Question: can someone explain how they got the expected return answer? Chapter 5, we identified the optimal (tangency) portfolio. How to hoose the weights between the

can someone explain how they got the expected return answer?

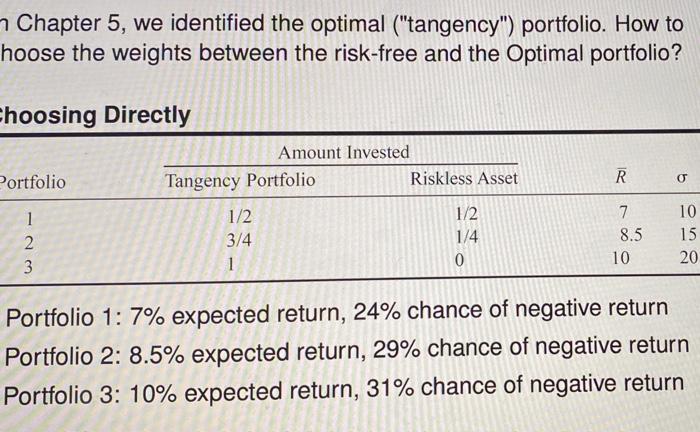

Chapter 5, we identified the optimal ("tangency") portfolio. How to hoose the weights between the risk-free and the Optimal portfolio? Choosing Directly Portfolio R Amount Invested Tangency Portfolio Riskless Asset 1/2 1/2 3/4 1/4 1 0 1 2 3 7 8.5 10 15 20 N 10 Portfolio 1: 7% expected return, 24% chance of negative return Portfolio 2: 8.5% expected return, 29% chance of negative return Portfolio 3: 10% expected return, 31% chance of negative return

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock