Question: Can you please answer the question showing full working out, thank you (b) Consider a European put option written on a stock that is now

Can you please answer the question showing full working out, thank you

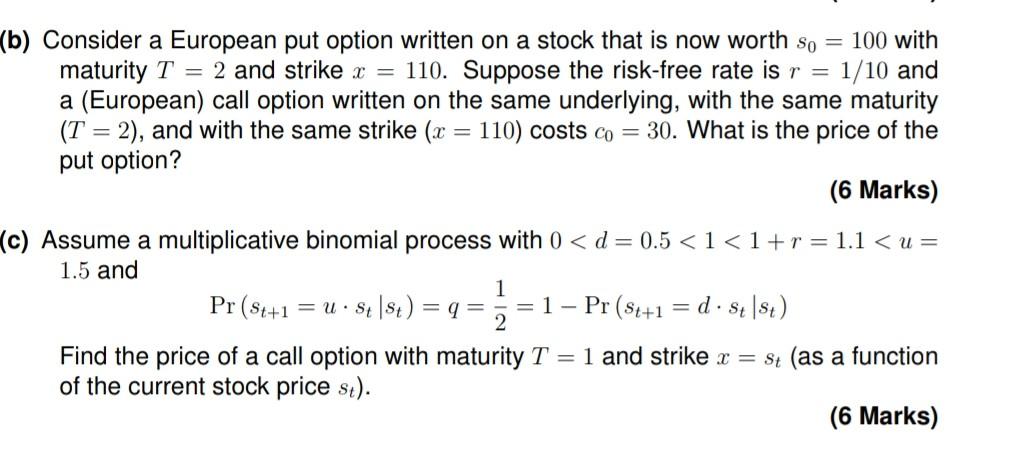

(b) Consider a European put option written on a stock that is now worth so = 100 with maturity T = 2 and strike x = 110. Suppose the risk-free rate is r = 1/10 and a (European) call option written on the same underlying, with the same maturity (T = 2), and with the same strike (x = 110) costs co = 30. What is the price of the put option? (6 Marks) (c) Assume a multiplicative binomial process with 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock