Question: Case Study #1 Which Insurance is best? For each scenario below, pick the health insurance that would best meet their needs and provide your justification.

Case Study #1 Which Insurance is best?

For each scenario below, pick the health insurance that would best meet their needs and provide your justification. The insurance options you have to choose from is provided here in the 2020 Benefits Guide.

Scenario 1: Marc Jacob, who lives in South Florida just got a new job and he needs to enroll in health insurance. He has 90 days to make his selection. Marc is a 30-year-old male, with no underlying health conditions. He does travel for his job. He usually travels for about a week and then works at the office when he is not traveling. What health insurance plan should he enroll in that would provide him with the best coverage? Thoroughly provide your justification and keep in mind the items listed below.

- Think about the contracted service areas (i.e., state only or nationwide)

- Coverage for individual versus family

- Annual deductibles

- Copays

- Monthly premiums

Scenario 2: Arya Stark is married with 4-year-old twin boys and lives with her family in South Florida. She recently got a new job as a Director of Operations of a large healthcare organization. She has 90 days to make her healthcare insurance selection. She does travel on occasion for business, but she also takes family trips during the summer when her kids are out of school. Her husband is a diabetic and also a cancer survivor, but herself and her kids are healthy individuals with no underlying health conditions. The twins are active with sports and are involved with swimming, martial arts and gymnastics. What health insurance plan should she enroll in that would provide her and her family with the best coverage? Thoroughly provide your justification and keep in mind the items listed below.

- Think about the contracted service areas (i.e., state only or nationwide)

- Coverage for individual versus family

- Annual deductibles

- Copays

- Monthly premium

Have a list of references in correct format at the end of the paper

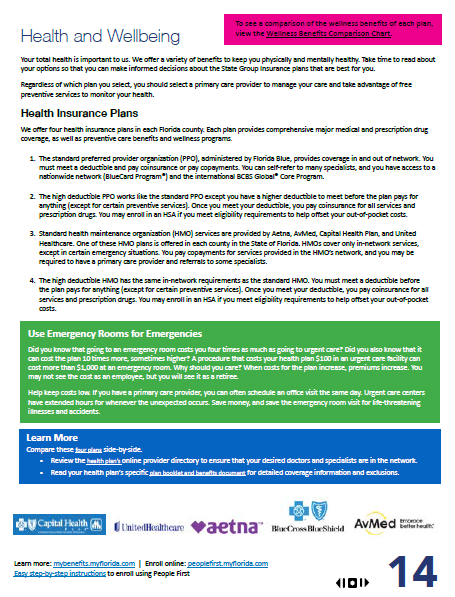

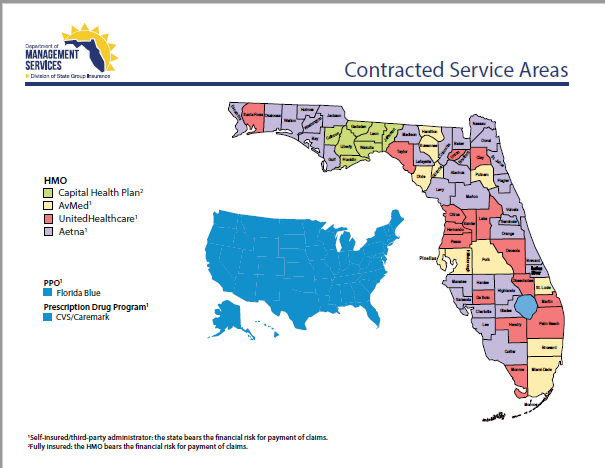

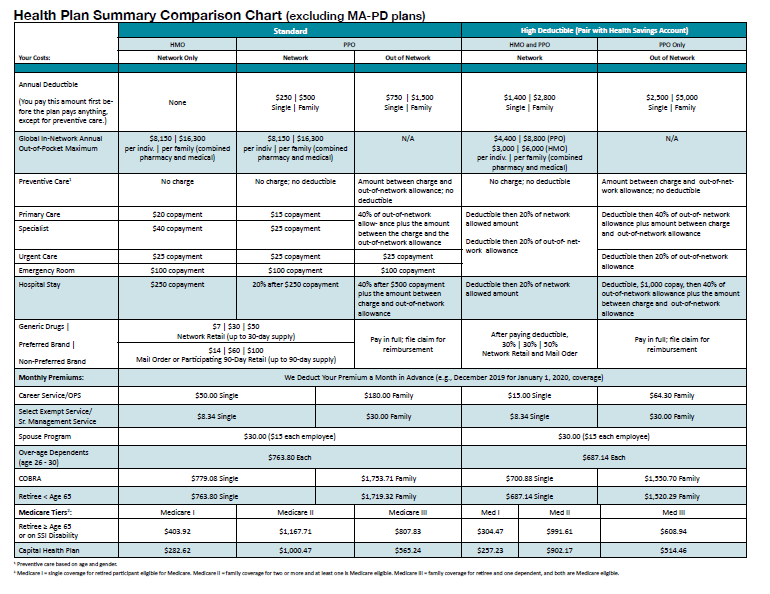

Health and Wellbeing To see a comparison of the wellness benefits of each plan, view the Wellness Benefits Comparison Chart. Your total health is important to us. We offer a variety of benefits to keep you physically and mentally healthy. Take time to read about your options so that you can make informed decisions about the State Group insurance plans that are best for you. Regardless of which plan you select, you should select a primary care provider to manage your care and take advantage of free preventive services to monitor your health. Health Insurance Plans We offer four health insurance plans in each Florida county. Each plan provides comprehensive mejor medical and prescription drug coverage, as well as preventive care benefits and wellness programs 1. The standard preferred provider organization (PPO), administered by Florida Blue, provides coverage in and out of network. You must meet a deductible and pay coinsurance or pay copayments. You can self-refer to many specialists, and you have access to a nationwide network (BlueCard Program) and the international BCBS Global Core Program. 2. The high deductible PFO works like the standard PPO except you have a higher deductible to meet before the plan pays for anything (except for certain preventive services). Once you meet your deductible, you pay coinsurance for all services and prescription drugs. You may enroll in an SA if you meet eligibility requirements to help offset your out-of-pocket costs. 3. Standard health maintenance organization (HMO) Services are provided by Aetna, Alied, Capital Health Fian, and United Healthcare. One of these HMO plans is offered in each county in the State of Florida. HMOs cover only in-network services, except in certain emergency situations. You pay copayments for services provided in the HMO's network, and you may be required to have a primary care provider and referrals to some specialists. 4. The high deductible HMO has the same in-network requirements as the standard HMO. You must meet a deductible before the plan peys for anything except for certain preventive services). Once you meet your deductible, you pay coinsurance for al Services and prescription drugs. You may enroll in an HSA if you meet eigbility requirements to help offset your out-of-pocket Use Emergency Rooms for Emergencies Did you know that going to an emergency room costs you four times as much as going to urgent care! Did you also know that it can cost the plan 10 times more, sometimes higher? A procedure that costs your health plan $1.00 in an urgent care facility can cost more than $1,000 at an emergency room. Why should you care? When costs for the plan increase, premium increase. You may not see the cost as an employee, but you will see it as a retiree Help keep costs low. If you have a primary care provider, you can often schedule an office visit the same day. Urgent care centers have extended hours for whenever the unexpected occurs. Save money, and save the emergency room vizit for ite-threatening illnesses and accidents Learn More Compare these are side-byside. - Review the health plek online provider directory to ensure that your desired doctors and specialists are in the network - Read your health plan's specific plan boodstard barn document for detailed coverage information and exclusions. Capital Health th Unitedhedhere aetna BacheShield Av Med ferme Learn more: mybenefits.myflorida.com Enroll online peoplefirst.myflorida.com Easy step-by-step instructions to enroll using People First 14 (101) Darmo MANAGEMENT SERVICES Die Grup Contracted Service Areas HMO Capital Health Plan AvMed United Healthcare Aetna wa PPO Florida Blue Prescription Drug Program! CVS/Caremark *Self-insured third-party administrator the state bears the financial risk for payment of claims. Fully insured the HMO bears the financial risk for payment of claims. Health Plan Summary Comparison Chart (excluding MA-PD plans) Standard PPO HMO Network Only High Deductible (Pair with Health Savings Account HMO and PPO PO Only Network Out of Network Your Costs: Network Out of Network Annual Deductible $750 $1,500 $250 $500 $1,400 $2,800 You pay this amount first be- $2,500 $5,000 None fore the plan pay anything Single Family Single Family Single Family Single Family except for preventive care. Global In-Network Annual $8,150 $15,300 $8,150 $16,300 N/A $4,400 $8,800 (PFO) N/A Out-of-Pocket Maximum per indiv. I per family combined per indivper family combined $3,000 $6,000 (HMO) pharmacy and medical pharmacy and medical per inciv. per family combined pharmacy and medical Preventive Carel Ne charge No charge no deductible Amount between charge and No charge: no deductible Amount between charge and out-of-net- out-of-network allowance: no work allowance no deductible deductible Primary Care $20 copement $15 copayment 40% of out-of-network Deductible then 20% of network Deductible then 40 of out-of-network allowance plus the amount allowed amount allowance plus amount between charge Specialist $40 copayment $23 copayment between the charge and the and out-of-network alowance out-of-network allowance Deductible then 20% of out-of-net- work allowance Urgent Care $25 copayment $29 copayment $25 copayment Deductible then 20% of out-of-network allowance Emergency Room $100 copayment $100 copayment $100 copayment Hospital Stay $250 copayment 20% after $250 copayment 40% after $500 copayment Deductible then 20% of network Deductible, $1,000 copay, then 40% of plus the amount between allowed amount out-of-network allowance plus the amount charge and out of network between charge and out-of-network allowance allowance Generic Drugs $7 $30 $50 Network Retail (up to 30-day supply) After paying deductible Pay in fuit; file cisim for Pay in full; nie claim for Preferred Brand 30% 30% 30% $14 $50 $100 reimbursement reimbursement Network Retail and Mail oder Non-Preferred Brand Mail Order or Participating 90-Day Retail (up to 90-day supply) Monthly Premiums: We Deduct Your Premium a Month in Advance les December 2019 for January 1, 2020, coverage Career Service/OPS $50.00 Single $180,00 Family $15.00 Single $64.30 Family Select Exempt Service $8.34 Single $30,00 Family $8.34 Single $30.00 Family St Management Service Spouse Program $30.00 ($15 esch employee $30.00 ($15 each employee Over-sge Dependents $763.80 Each $687.14 Esch (age 26 - 30 COBRA $779.08 Single $1,753.71 Family $700.38 Single $1,350.70 Family Retiree

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts