Question: Case Study - The organization turned upside down Review the case study on page 328 What is the point of an upside down organizational structure?

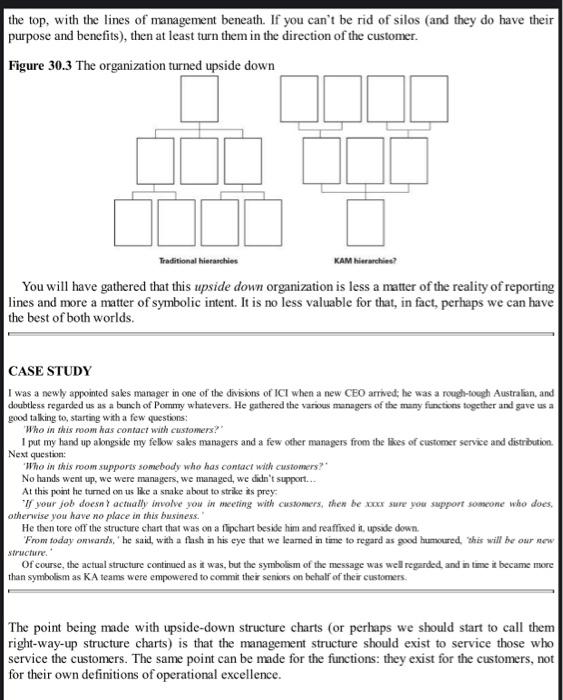

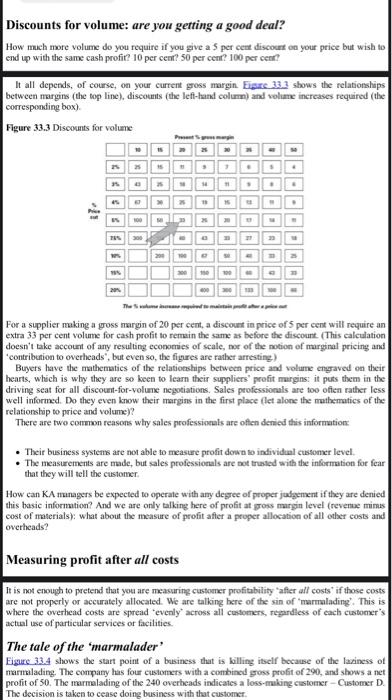

Case Study - The organization turned upside down Review the case study on page 328 What is the point of an upside down organizational structure? Case Study - Measuring customer profitability - Review the volume discount on page 372 For a supplier making a gross margin of 35% and agreeing to a price cut of 3%, what is the percentage of volume increase to maintain a cash profit of the same amount prior to the price cut? the top, with the lines of management beneath. If you can't be rid of silos (and they do have their purpose and benefits), then at least turn them in the direction of the customer. Figure 30.3 The organization turned upside down Traditional hierarchies KAM hierarchies? You will have gathered that this upside down organization is less a matter of the reality of reporting lines and more a matter of symbolic intent. It is no less valuable for that, in fact, perhaps we can have the best of both worlds CASE STUDY I was a newly appointed sales manager in one of the divisions of ICI when a new CEO arrived, he was a rough-tough Australian, and doubtless regarded us as a bunch of Pommy whatevers. He gathered the varius managers of the many functives together and gave us a good talking to starting with a few questions Who in this room has contact with customers? I put my hand up alongside my fellow sales managers and a few other managers from the likes of customer service and distribution Next question: 'Who in this room supports somebody who has contact with customers No hands went up, we were managers, we managed, we didn't support... At this point he turned on us like a snake about to strike its prey "If your job doesny actually involve you in meeting with customers, then be xxxx sure your support someone who does. otherwise you have no place in this business. He then tore off the structure chart that was on a flipchart beside him and reaffixed it, upside down. From today onwards," he said, with a flash in his eye that we learned in time to regard as good humoured this will be our new Of course, the actual structure continued as it was, but the symbolism of the message was wel regarded and in time it became more than symbolism as KA teams were empowered to commit their seniors on behalf of their customers. structure The point being made with upside-down structure charts (or perhaps we should start to call them right-way-up structure charts) is that the management structure should exist to service those who service the customers. The same point can be made for the functions: they exist for the customers, not for their own definitions of operational excellence. Discounts for volume: are you getting a good deal? How much more volume do you require if you give a 5 per cent discount on your price but wish to end up with the same cash profit? 10 per cent? 50 per cent? 100 percent? It all depends, of course, on your current gross margin Figure 3.3 shows the relationships between margins (the top line), discouts (the left-hand column) and volume increases required (the corresponding box) Figure 33.3 Discounts for volume 1 For a supplier making a gross margin of 20 per cent, a discount in price of 5 per cent will require an extra 33 per cent volume for cash profit to remain the same as before the discount. (This calculation doesn't take account of any resulting economies of scale, nor of the notion of marginal pricing and contribution to overheads, but even so, the figures are rather arresting) Buyers have the mathematics of the relationships between price and volume engraved on their hearts, which is why they are so keen to learn their suppliers' profit margins: it puts them in the driving seat for all discount-for-volume negotiations Sales professionals are too ofien rather less well informed. Do they even know their margins in the first place let alone the mathematics of the relationship to price and volume)? There are two common reasons why sales professionals are often denied this information: Their business systems are not able to measure profit down to individual customer level. The measurements are made, but sales professionals are not trusted with the information for fear that they will tell the customer How can KA managers be expected to operate with any degree of proper judgement if they are denied this basic information? And we are only talking here of profit at gross margin level (revenue minus cost of materials): what about the measure of profit after a proper allocation of all other costs and overheads? Measuring profit after all costs It is not enough to pretend that you are measuring customer profitability after all costs' if those costs are not properly or accurately allocated. We are talking here of the sin of "marmalading. This is where the overhead costs are spread evenly across all customers, regardless of each customer's actual use of particular services or facilities. The tale of the "marmalader Figure 33.4 shows the start point of a business that is killing itself because of the laziness of marmalading. The company has four customers with a combined gross profit of 290, and shows a net profit of 50. The marmalading of the 240 overbeads indicates a loss-making customer-Customer D. The decision is taken to cease doing business with that customer