Question: Cash Flows from Operating Activities-indirect Method The income statement disclosed the following items for the year: Depreciation expense $34,200 Gain on disposal of equipment 19,930

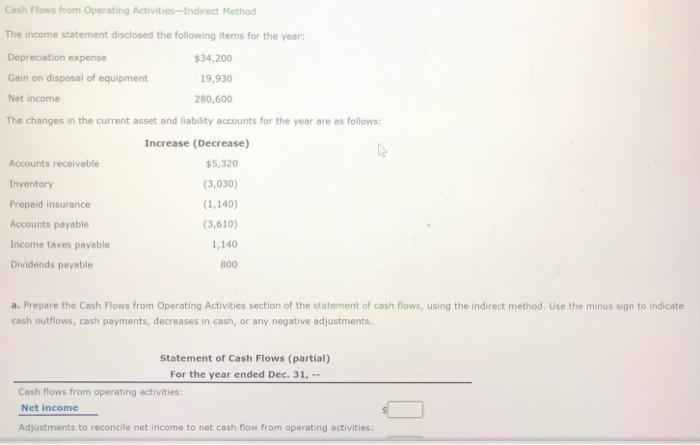

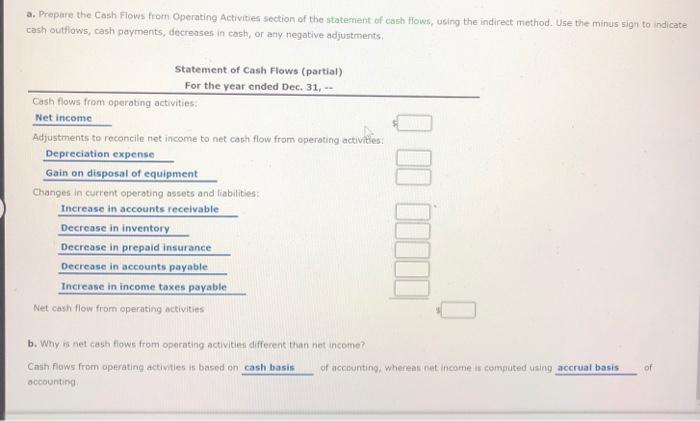

Cash Flows from Operating Activities-indirect Method The income statement disclosed the following items for the year: Depreciation expense $34,200 Gain on disposal of equipment 19,930 Net income 280,600 The changes in the current asset and liability accounts for the year are as follows: Increase (Decrease) Accounts receivable $5,320 Inventory (3,030) Prepaid insurance (1,140) Accounts payable (3,610) Income taxes payable 1,140 Dividends payable 800 a. Prepare the Cash Flows from Operating Activities section of the statement of cash flows, using the Indirect method. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments. Statement of Cash Flows (partial) For the year ended Dec. 31, -- Cash flows from operating activities Net income Adjustments to reconcile not income to net cash flow from operating activities: a. Prepare the Cash Flows from Operating Activities section of the statement of cash flows, using the indirect method. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments, Statement of Cash Flows (partial) For the year ended Dec. 31, -- Cash flows from operating activities: Net income Adjustments to reconcile net income to net cash flow from operating activities: Depreciation expense Gain on disposal of equipment Changes in current operating assets and liabilities: Increase in accounts receivable Decrease in inventory Decrease in prepaid insurance Decrease in accounts payable Increase in income taxes payable Net cash flow from operating activities b. Why is net cash flows from operating activities different than net income? Cash Flows from operating activities is based on cash basis of accounting, whereas net income is computed using accrual basis accounting of

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts