Question: Centered random walk. A random sequence (So, S1, .. . ) is defined recursively by So = x0 and St = St-1 + Xt for

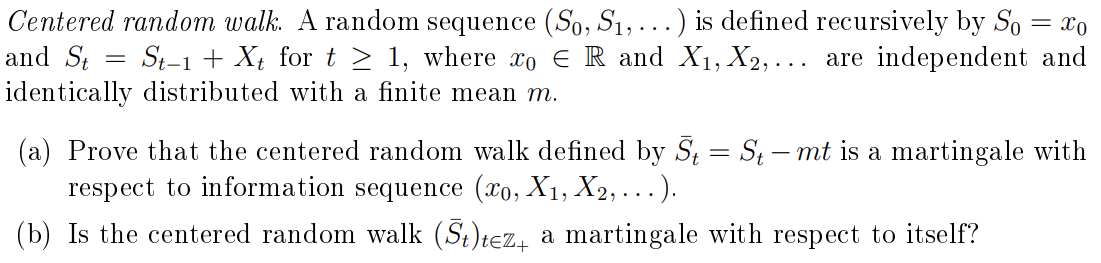

Centered random walk. A random sequence (So, S1, .. . ) is defined recursively by So = x0 and St = St-1 + Xt for t > 1, where No E R and X1, X2, ... are independent and identically distributed with a finite mean m. (a) Prove that the centered random walk defined by St = St -mt is a martingale with respect to information sequence (xo, X1, X2, . . .). (b) Is the centered random walk (St)tez, a martingale with respect to itself

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock