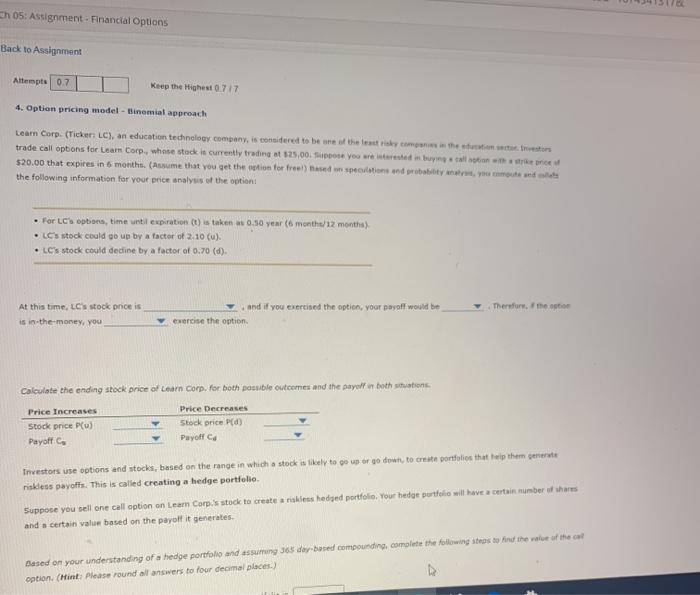

Question: Ch 05: Assignment - Financial Options Back to Assignment Attempts 0.7 Keep the Highest 0717 4. Option pricing model - Binomial approach Learn Corp. (Ticker

Ch 05: Assignment - Financial Options Back to Assignment Attempts 0.7 Keep the Highest 0717 4. Option pricing model - Binomial approach Learn Corp. (Ticker LC), an education technology company is considered to be one of the risky cam the contratos trade call options for Learn Corp., whose stack is currently trading at $25,00. You wrested in buying all time $20.00 that expires in 6 months. (Assume that you get the option for free) tased on perlotions and probably wound the following information for your price analysis of the option For LC's options, time until expiration (t) is taken *030 year (o months/12 months) LCS stock could go up by a factor of 2.10 (). LC's stock could decline by a factor of 0.70 (d). Therefore, the At this time, LC's stock price is is in the money, you and if you evertised the option, your payoff would be exercise the option Calculate the ending stock price of Learn Corp. for both possible outcomes and the payoff both wions Price Increases Stock price PC) Payoff Price Decreases Stock price P(d) Payoff Co Investors use options and stocks, based on the range in which a stock is likely to go or go down to create portfolios that help them generate riskless payoffs. This is called creating a hedge portfolio Suppose you sell one call option on Learn Corp's stock to create a rakous hedged portfolio. Your bedge portfolio will have a certain number of whares and a certain value based on the payoff it generates. Based on your understanding of a hedge portfolio and assuming 365 day-based compounding complete the following stros do find the value of the option. (Hint: Please round all answers to four decimal places) Ch 05: Assignment - Financial Options Back to Assignment Attempts 0.7 Keep the Highest 0717 4. Option pricing model - Binomial approach Learn Corp. (Ticker LC), an education technology company is considered to be one of the risky cam the contratos trade call options for Learn Corp., whose stack is currently trading at $25,00. You wrested in buying all time $20.00 that expires in 6 months. (Assume that you get the option for free) tased on perlotions and probably wound the following information for your price analysis of the option For LC's options, time until expiration (t) is taken *030 year (o months/12 months) LCS stock could go up by a factor of 2.10 (). LC's stock could decline by a factor of 0.70 (d). Therefore, the At this time, LC's stock price is is in the money, you and if you evertised the option, your payoff would be exercise the option Calculate the ending stock price of Learn Corp. for both possible outcomes and the payoff both wions Price Increases Stock price PC) Payoff Price Decreases Stock price P(d) Payoff Co Investors use options and stocks, based on the range in which a stock is likely to go or go down to create portfolios that help them generate riskless payoffs. This is called creating a hedge portfolio Suppose you sell one call option on Learn Corp's stock to create a rakous hedged portfolio. Your bedge portfolio will have a certain number of whares and a certain value based on the payoff it generates. Based on your understanding of a hedge portfolio and assuming 365 day-based compounding complete the following stros do find the value of the option. (Hint: Please round all answers to four decimal places)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts