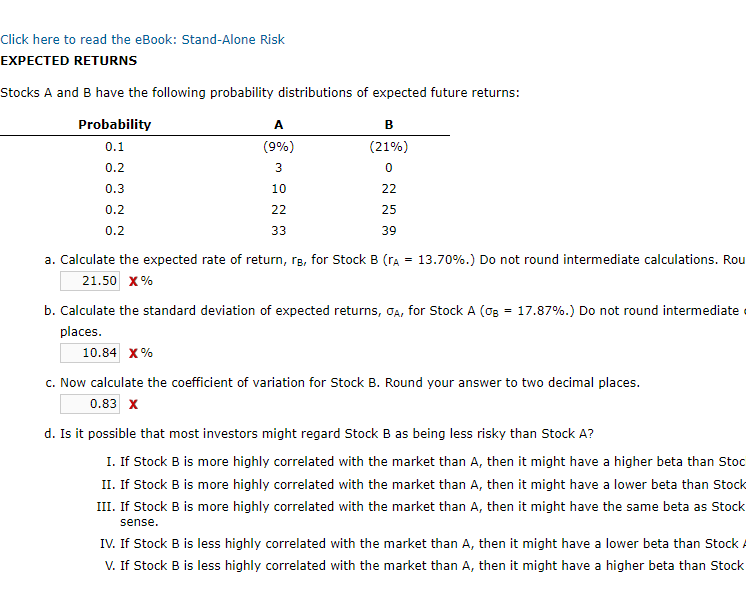

Question: Click here to read the eBook: Stand-Alone Risk EXPECTED RETURNS Stocks A and B have the following probability distributions of expected future returns: Probability A

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts