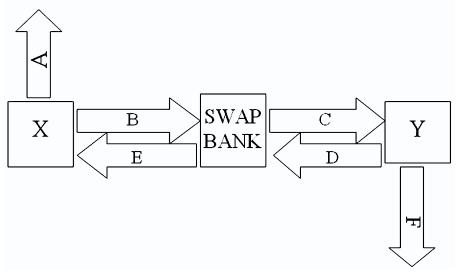

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed

Fantastic news! We've Found the answer you've been seeking!

Question:

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here:

| Fixed-Rate | Floating-Rate | |||

| Borrowing Cost | Borrowing Cost | |||

| Company X | 10% | LIBOR | ||

| Company Y | 12% | LIBOR + 1.5% | ||

A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05 percent−10.45 percent against LIBOR flat.

Assume both X and Y agree to the swap bank's terms. Fill in the values for A, B, C, D, E, & F on the diagram.

Expert Answer:

Company X wants to pay floating rates It borrow money from outside at fixed rate Company Y wants to ... View the full answer

Related Book For

Posted Date: