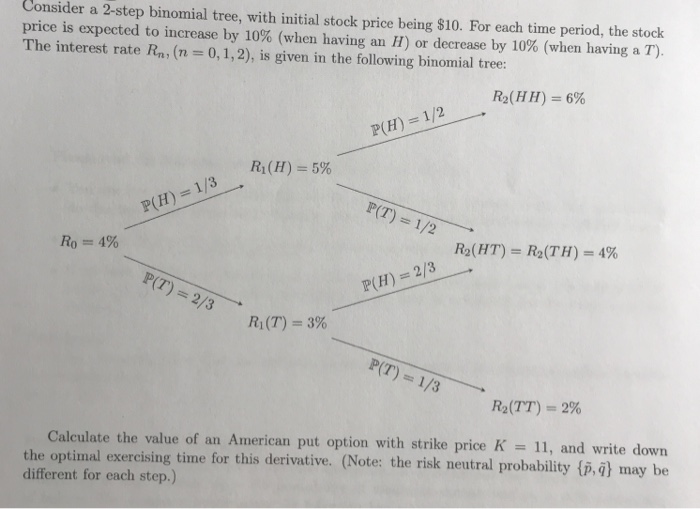

Question: Consider a 2-step binomial tree, with initial stock price being $10. For each time period, the stock price is expected to increase by 10% (when

Consider a 2-step binomial tree, with initial stock price being $10. For each time period, the stock price is expected to increase by 10% (when having an 11) or decrease by 10% (when having a T). The interest rate Rn, (n-0,1,2), is given in the following binomial tree: R2(H H) = 6% 2 R1(H) 5% 1/3 Ro 1% R2(HT)-R2(TH) 4% R, (T) = 3% Ra(TT) 2% Calculate the value of an American put option with strike price K 11, and write down the optimal exercising time for this derivative. (Note: the risk neutral probability (p.i) may be different for each step.) Springer Finance Textbook Steven E.Shreve Stochastic Calculus for Finance l The Binomial Asset Pricing Model S(HH) 16 Sa S (T)-2 Springer

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts