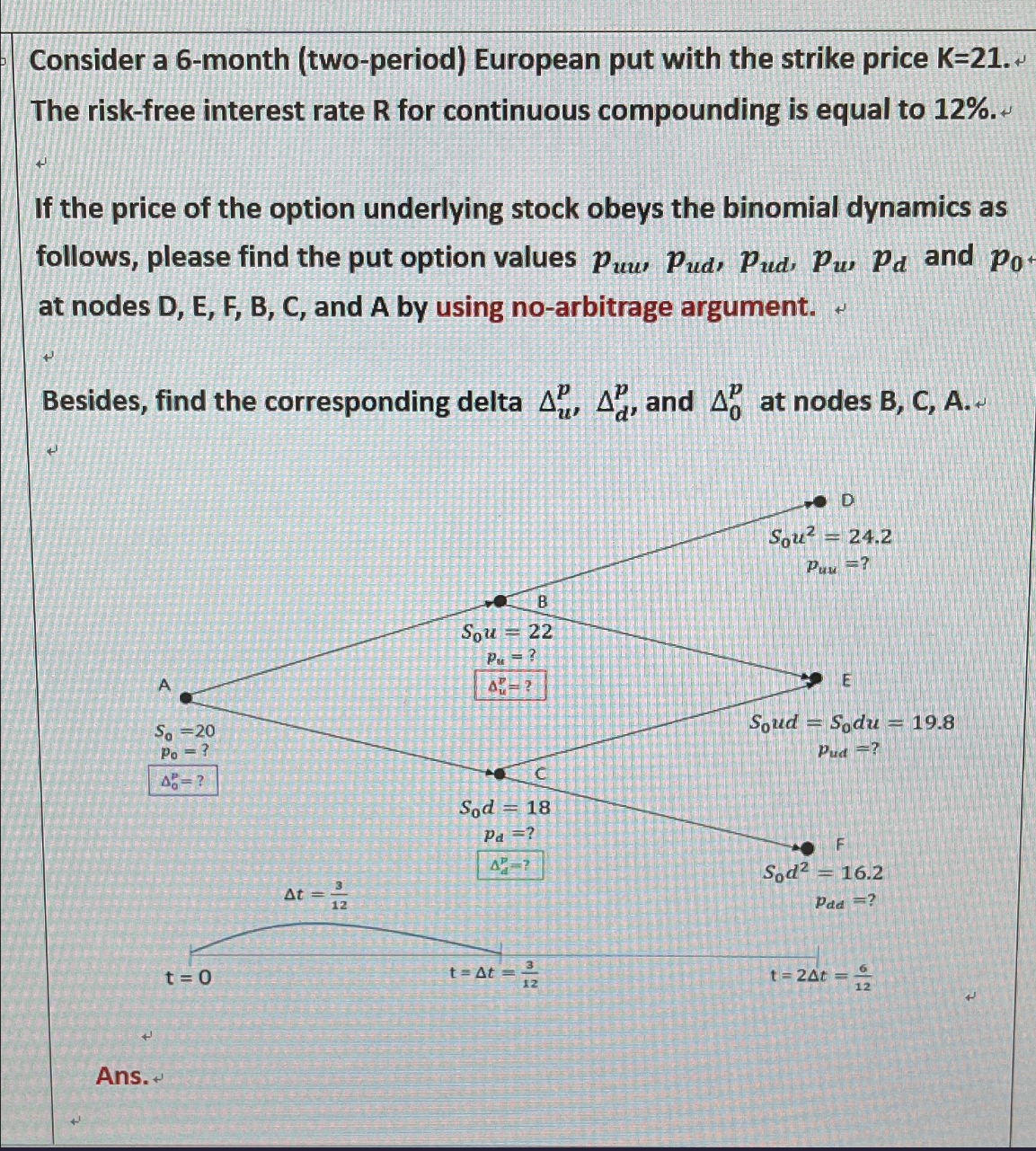

Question: Consider a 6 - month ( two - period ) European put with the strike price K = 2 1 . The risk - free

Consider a month twoperiod European put with the strike price K The riskfree interest rate for continuous compounding is equal to

If the price of the option underlying stock obeys the binomial dynamics as follows, please find the put option values and at nodes D E F B C and A by using noarbitrage argument.

Besides, find the corresponding delta and at nodes B C A

Ans.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock