Question: Consider a four-factor APT model with self-financing factors. The table below provides the expected return for each of the factors as well as the beta

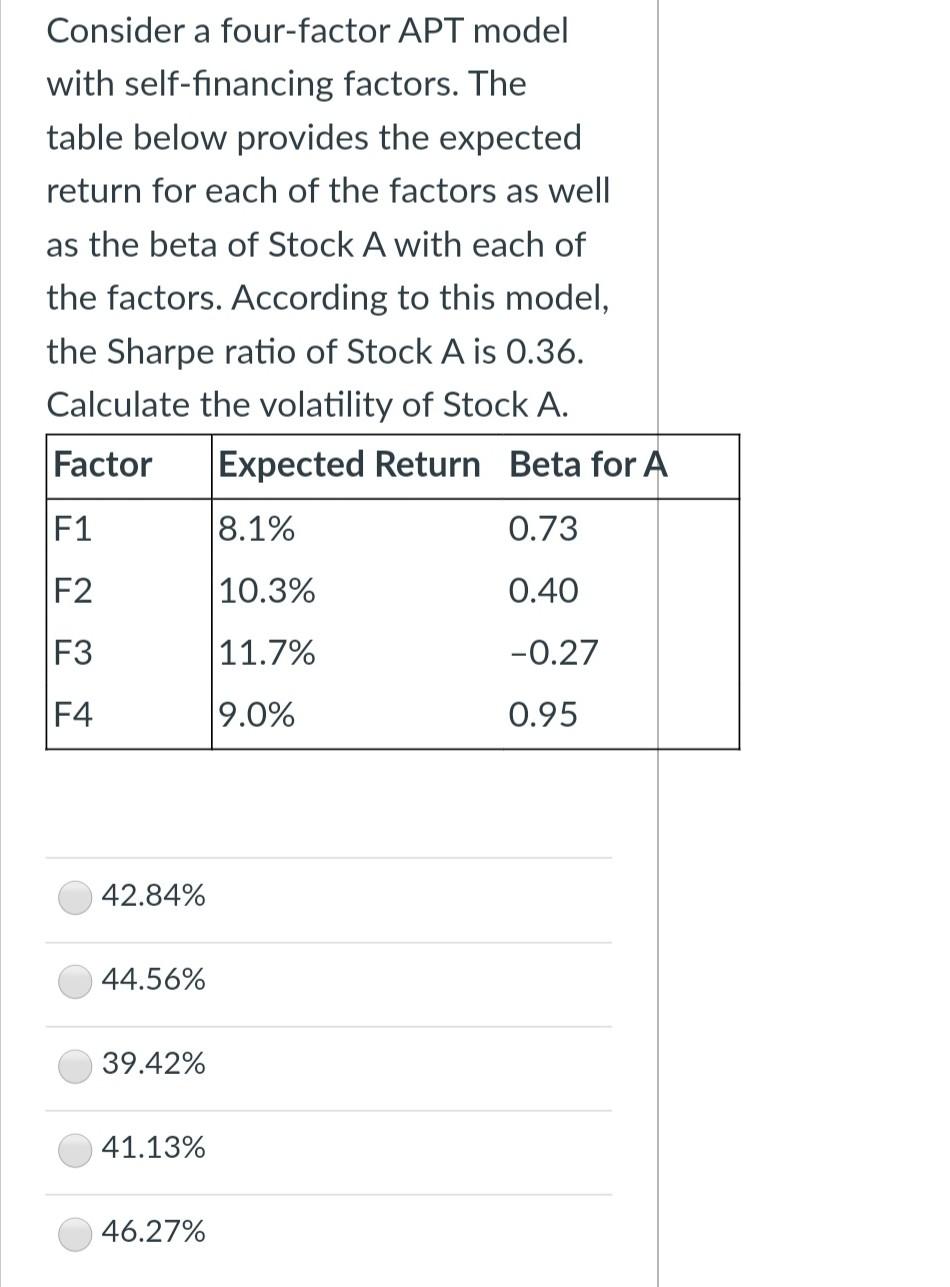

Consider a four-factor APT model with self-financing factors. The table below provides the expected return for each of the factors as well as the beta of Stock A with each of the factors. According to this model, the Sharpe ratio of Stock A is 0.36. Calculate the volatility of Stock A. Factor Expected Return Beta for A F1 8.1% 0.73 F2 10.3% 0.40 F3 11.7% -0.27 F4 9.0% 0.95 42.84% 44.56% 39.42% 41.13% 46.27%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock