Question: Consider a stock with a current price and possible prices in 1 year given by the binomial tree below, and a 1 - year call

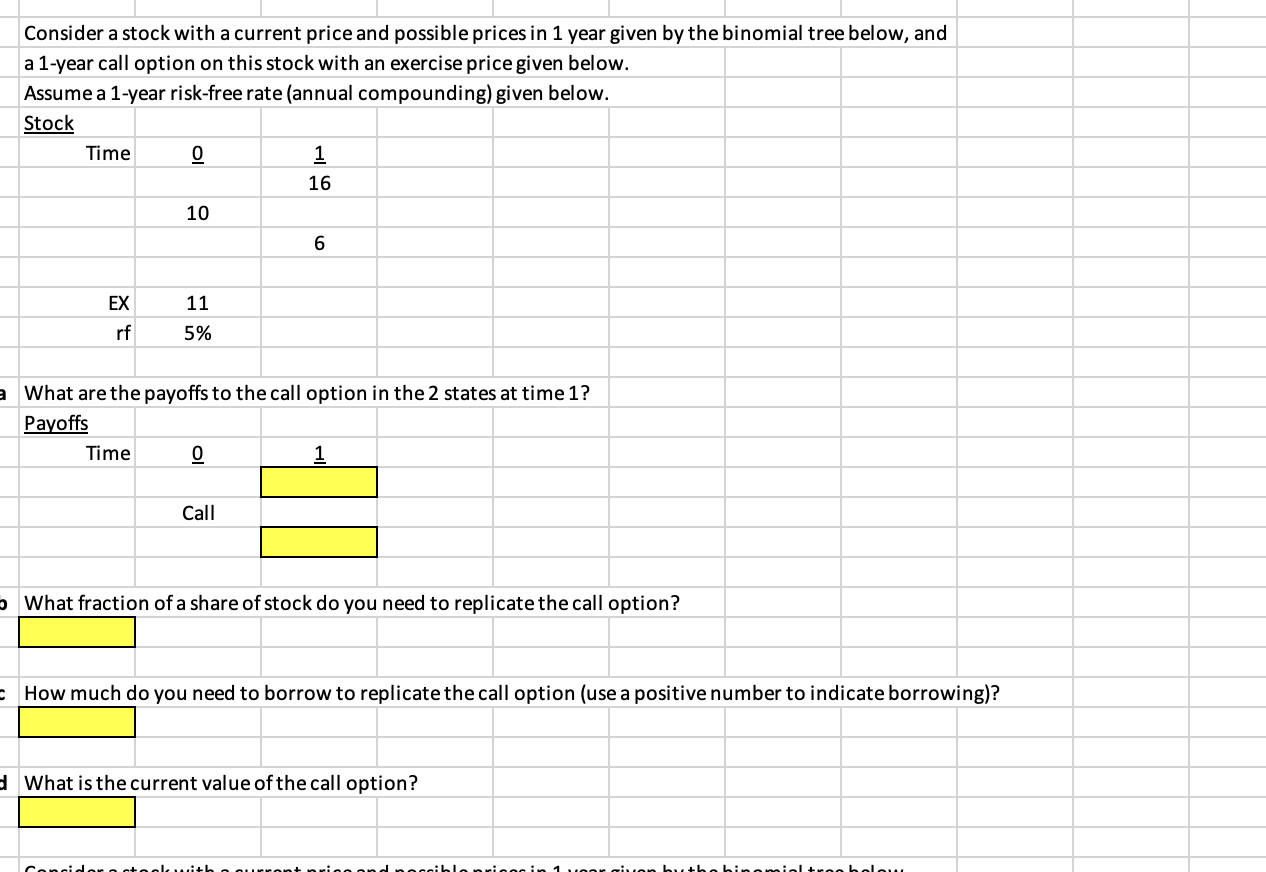

Consider a stock with a current price and possible prices in year given by the binomial tree below, and

a year call option on this stock with an exercise price given below.

Assume a year riskfree rate annual compounding given below.

What are the payoffs to the call option in the states at time

Payoffs

What fraction of a share of stock do you need to replicate the call option?

How much do you need to borrow to replicate the call option use a positive number to indicate borrowing

What is the current value of the call option?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock