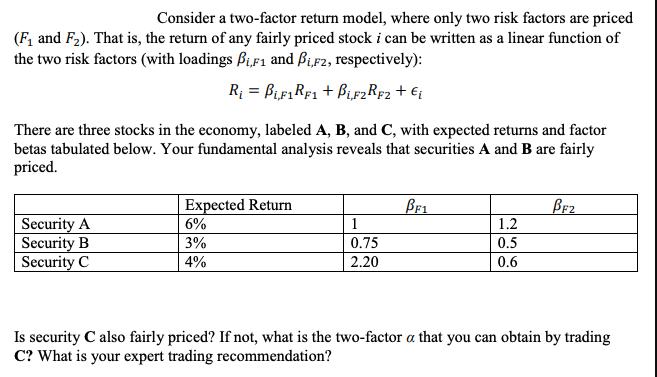

Question: Consider a two-factor return model, where only two risk factors are priced (F and F). That is, the return of any fairly priced stock

Consider a two-factor return model, where only two risk factors are priced (F and F). That is, the return of any fairly priced stock i can be written as a linear function of the two risk factors (with loadings Bi,F1 and i,F2, respectively): R = BiF1RF1+ Biz RF2 + i There are three stocks in the economy, labeled A, B, and C, with expected returns and factor betas tabulated below. Your fundamental analysis reveals that securities A and B are fairly priced. Expected Return BF1 BF2 Security A Security B 6% 1 1.2 3% 0.75 0.5 Security C 4% 2.20 0.6 Is security C also fairly priced? If not, what is the two-factor a that you can obtain by trading C? What is your expert trading recommendation?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts