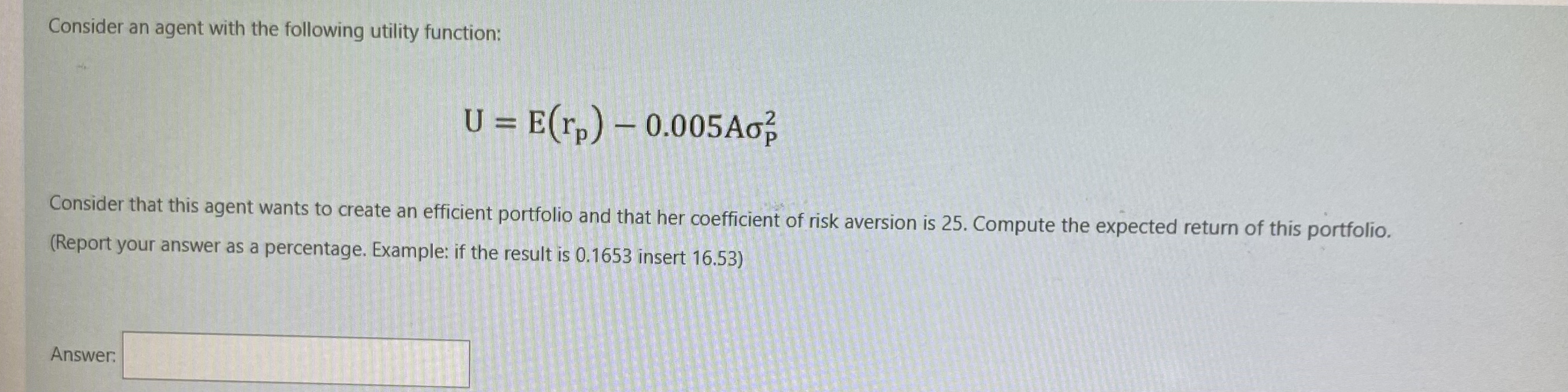

Question: Consider an agent with the following utility function: U = E(Ip) - 0.005Aop Consider that this agent wants to create an efficient portfolio and that

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock