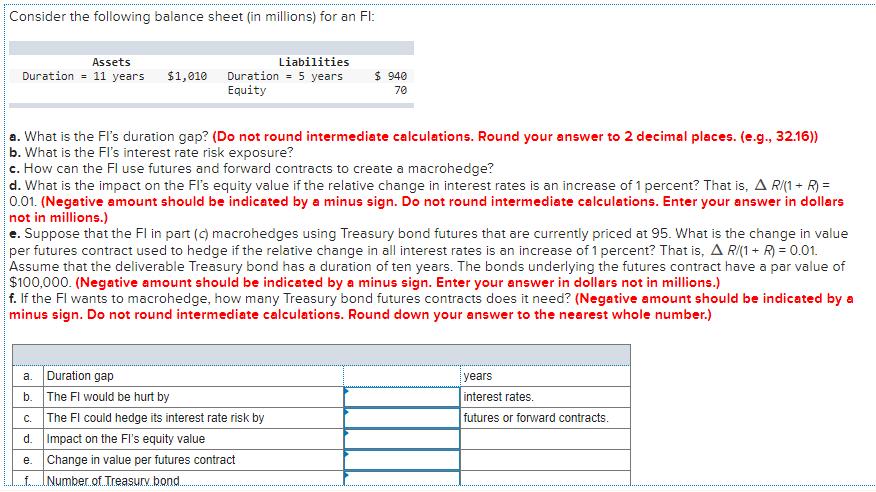

Consider the following balance sheet (in millions) for an Fl: Assets Liabilities Duration 11 years $1,010...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Financial Markets and Institutions

ISBN: 978-0077861667

6th edition

Authors: Anthony Saunders, Marcia Cornett

Posted Date: