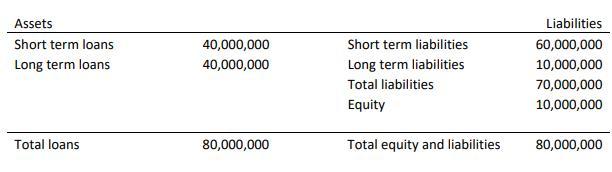

Consider the following simplified example of a commercial bank, which is borrowing and lending funds of two

Question:

Consider the following simplified example of a commercial bank, which is borrowing and lending funds of two maturities: short-term (1 year) and long-term (2 years), all zero-coupon. Loans consist of $40 million short term and $40 million long term, while liabilities are $60 million short term and $10 million long term. All numbers are in market value terms as of October 30, 2012. Hence, the bank’s balance sheet is the yield curve as of October 30, 2012, is a flat solid line; Annual yields on assets and liabilities of all maturities are 10%. Now suppose that on October 31, 2012, the yield curve shifts parallel such that all yields rise to 12%.

A) What is the new balance sheet of the bank?

B) What is the impact of a parallel shift in the yield curve to the economic value of the bank?

Expert Answer:

A The balance will still be the same since all numbers are in market value as of October 30 ... View the full answer

Principles of Corporate Finance

ISBN: 978-0072869460

7th edition

Authors: Richard A. Brealey, Stewart C. Myers