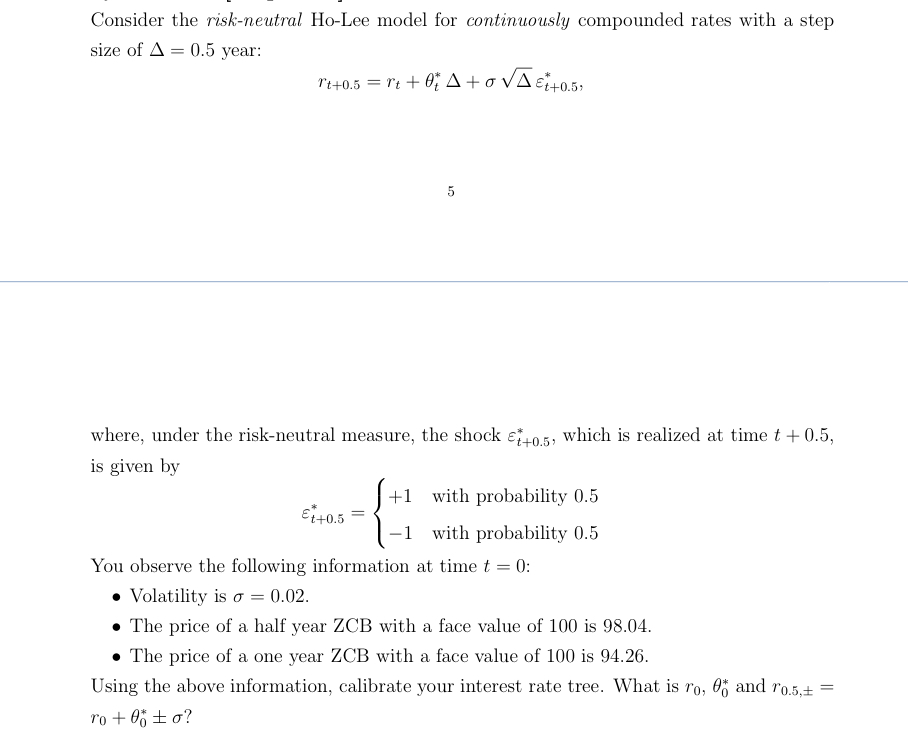

Question: Consider the risk - neutral Ho - Lee model for continuously compounded rates with a step size of = 0 . 5 year: r t

Consider the riskneutral HoLee model for continuously compounded rates with a step size of year:

where, under the riskneutral measure, the shock which is realized at time is given by

You observe the following information at time :

Volatility is

The price of a half year ZCB with a face value of is

The price of a one year ZCB with a face value of is

Using the above information, calibrate your interest rate tree. What is and

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock