Question: Consider the stochastic differential equation (SDE): dS = dSt St(udt + odWt), So = S, where and are constant drift and volatility, respectively, and

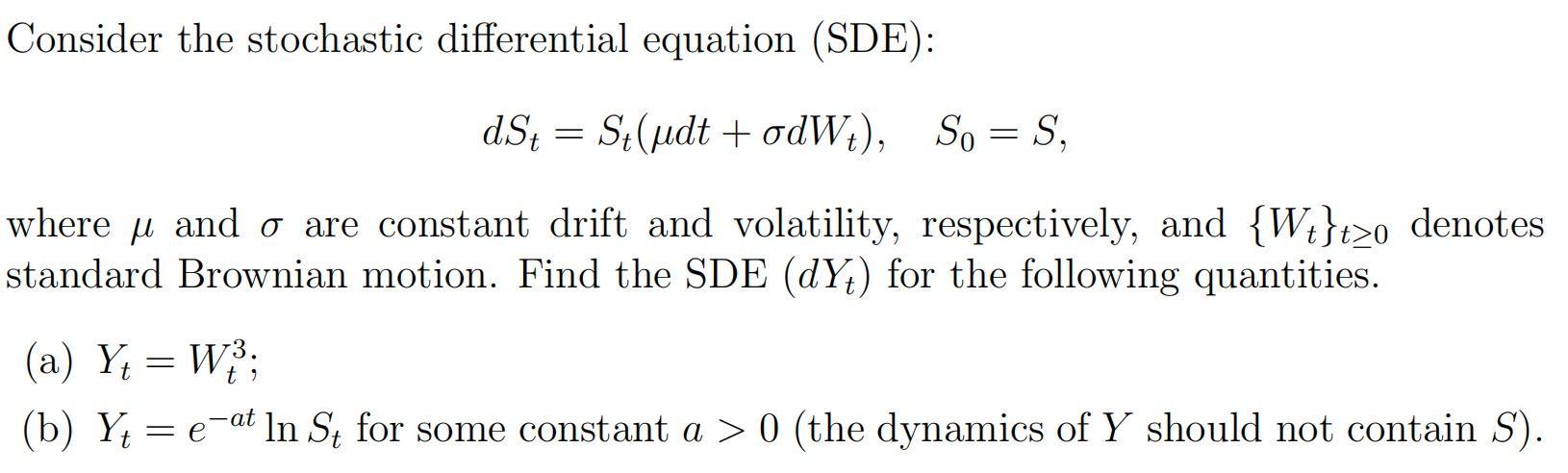

Consider the stochastic differential equation (SDE): dS = dSt St(udt + odWt), So = S, where and are constant drift and volatility, respectively, and {W}tzo denotes standard Brownian motion. Find the SDE (dY) for the following quantities. (a) Y = W; (b) Y = eat In St for some constant a > 0 (the dynamics of Y should not contain S).

Step by Step Solution

★★★★★

3.50 Rating (150 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock