Question: Could you help me to solve this question from Financial modelling course? 3. A writer is currently selling 100 identical European calls and wants to

Could you help me to solve this question from Financial modelling course?

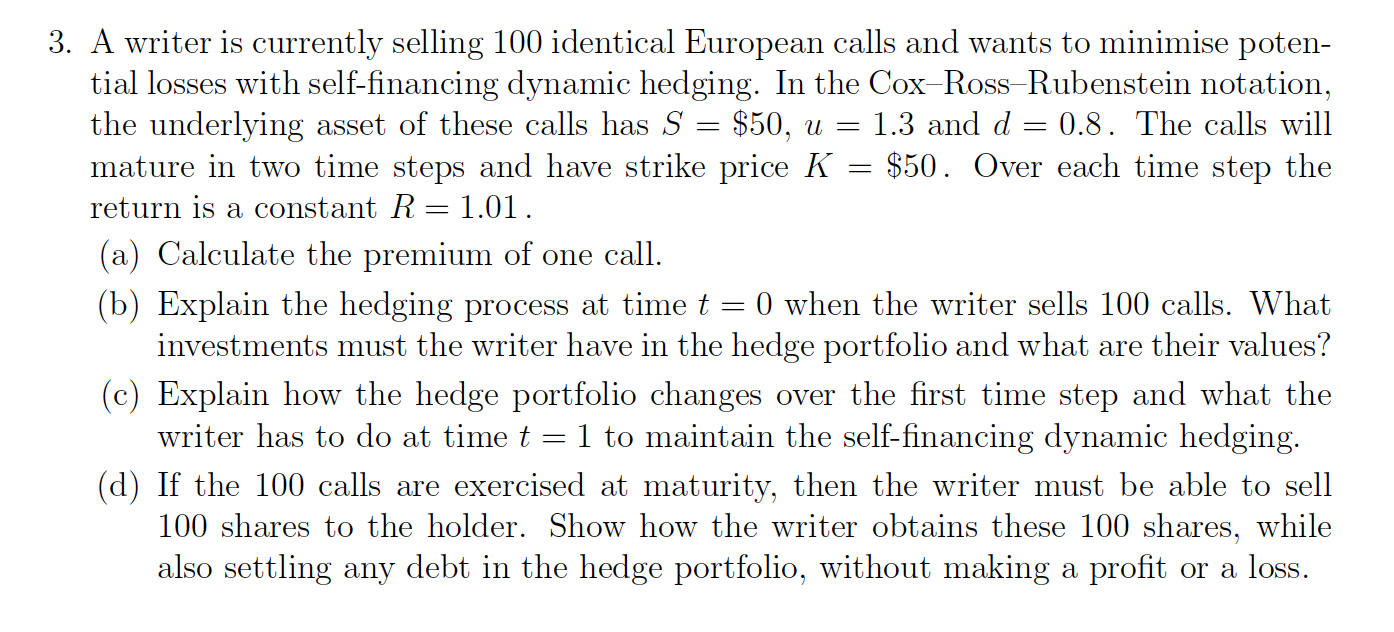

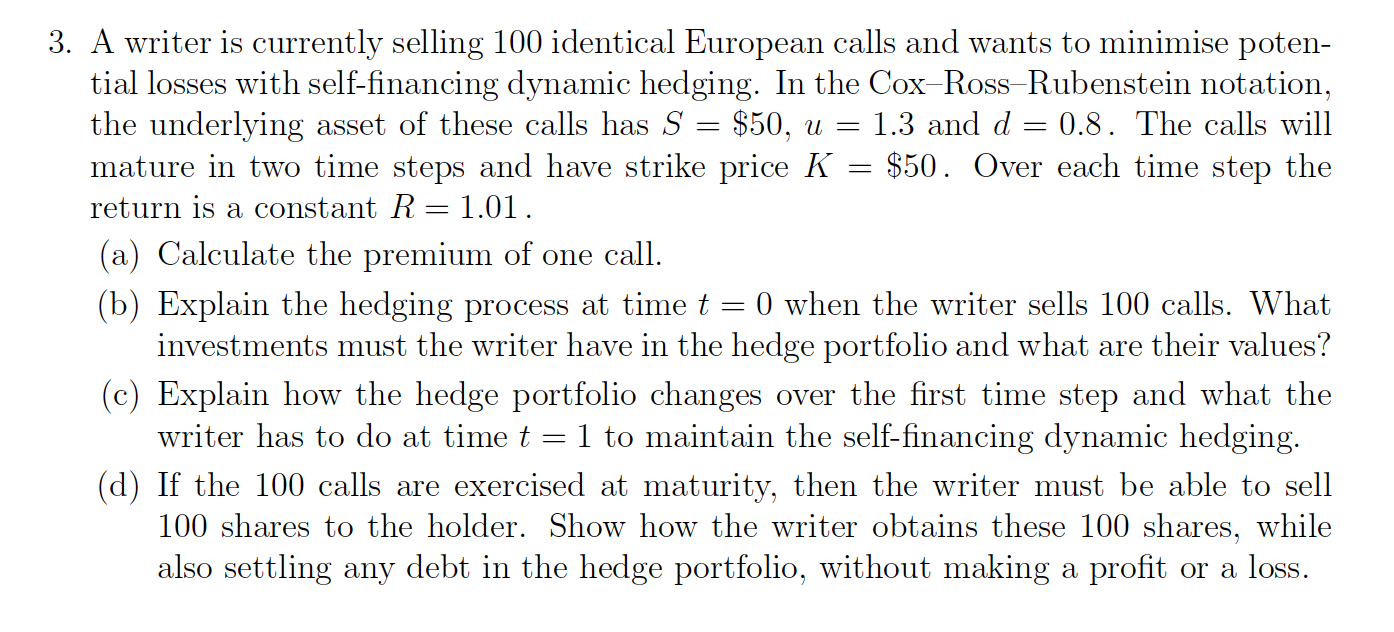

3. A writer is currently selling 100 identical European calls and wants to minimise poten- tial losses with self-nancing dynamic hedging. In the CoxRossRubenstein notation, the underlying asset of these calls has 8 = $50, u = 1.3 and d = 0.8. The calls will mature in two time steps and have strike price K = $50. Over each time step the return is a constant B = 1.01 . (a) Calculate the premium of one call. (b) Explain the hedging process at time t = 0 when the writer sells 100 calls. What investments must the writer have in the hedge portfolio and what are their values? (0) Explain how the hedge portfolio changes over the rst time step and what the writer has to do at time t = 1 to maintain the selfnancing dynamic hedging. (d) If the 100 calls are exercised at maturity, then the writer must be able to sell 100 shares to the holder. Show how the writer obtains these 100 shares, while also settling any debt in the hedge portfolio, without making a prot or a loss

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts