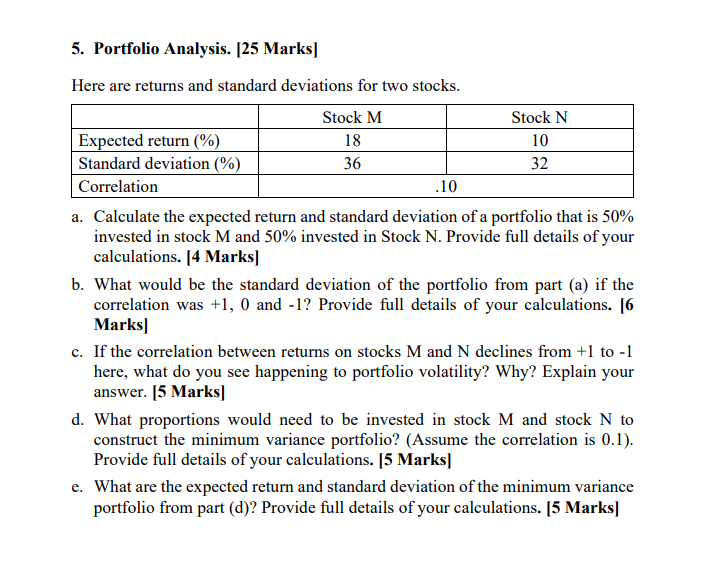

Question: could you please answer these with workings 5. Portfolio Analysis. [25 Marks] Here are retums and standard deviations for two stocks. Stock M Stock N

could you please answer these with workings

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock