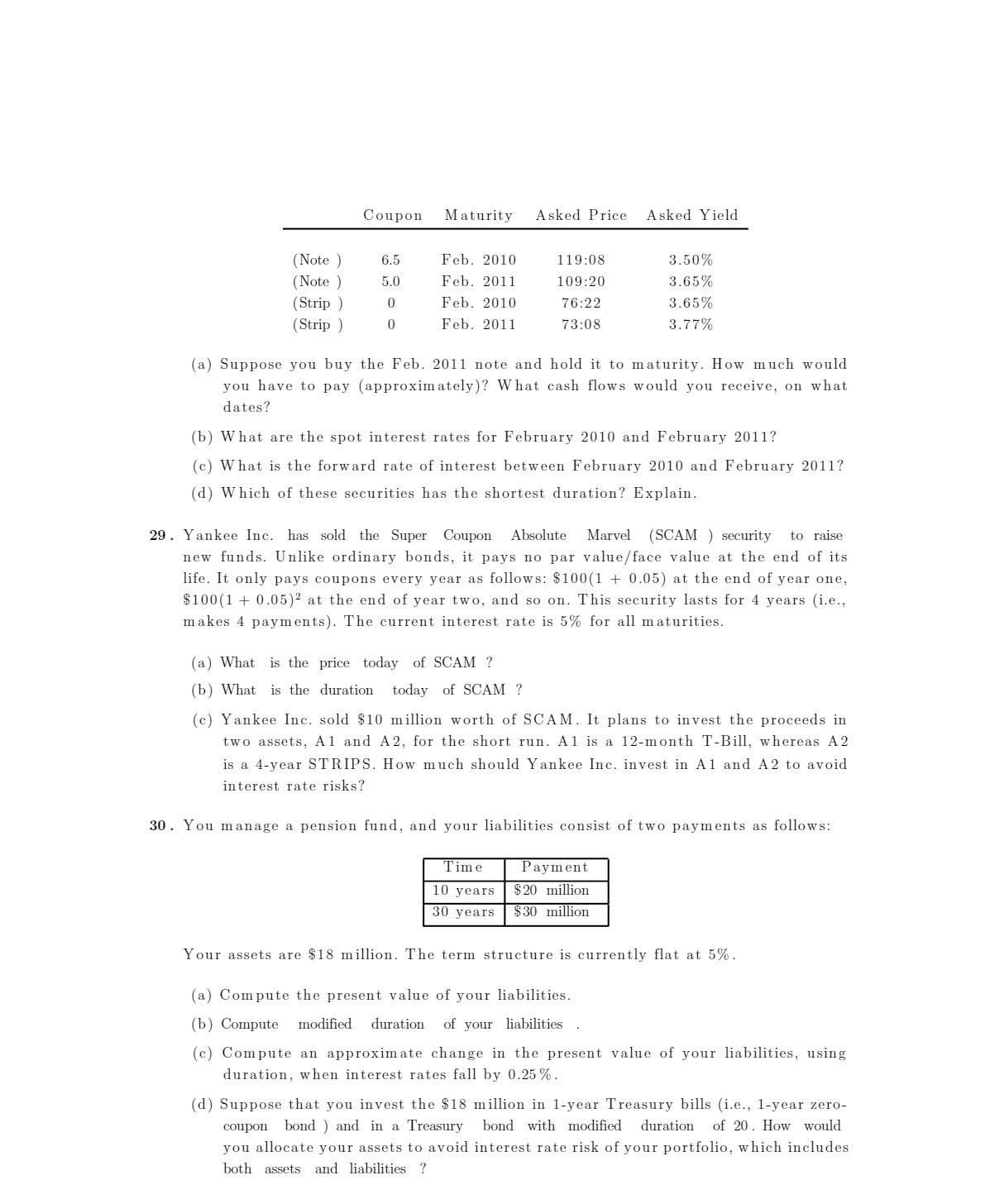

Question: Coupon Maturity Asked Price Asked Yield (Note ) 6.5 Feb. 2010 119:03 3.50% (Note ) 3.0 Feb. 2011 109:20 3.35% (Strip ) 0 Feb. 2010

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock