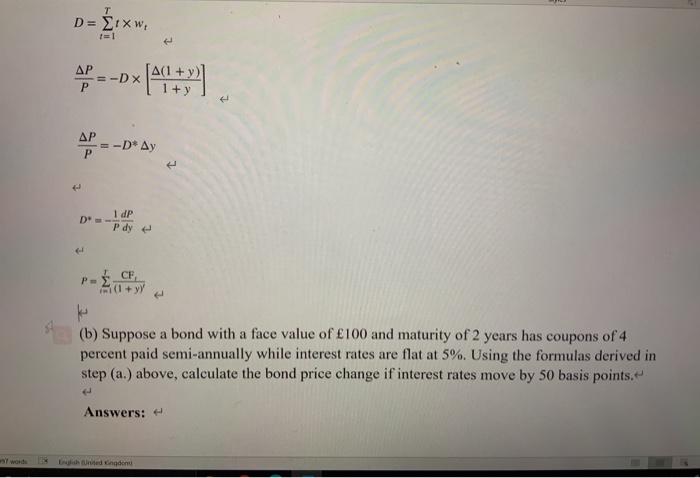

Question: D = w, . -=-DX P -Dx (40+ AP = -D* Ay P D- 1 dp P dy 4 CE P (b) Suppose a bond

D = w, . -=-DX P -Dx (40+ AP = -D* Ay P D- 1 dp P dy 4 CE P (b) Suppose a bond with a face value of 100 and maturity of 2 years has coupons of 4 percent paid semi-annually while interest rates are flat at 5%. Using the formulas derived in step (a.) above, calculate the bond price change if interest rates move by 50 basis points. Answers: 1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock