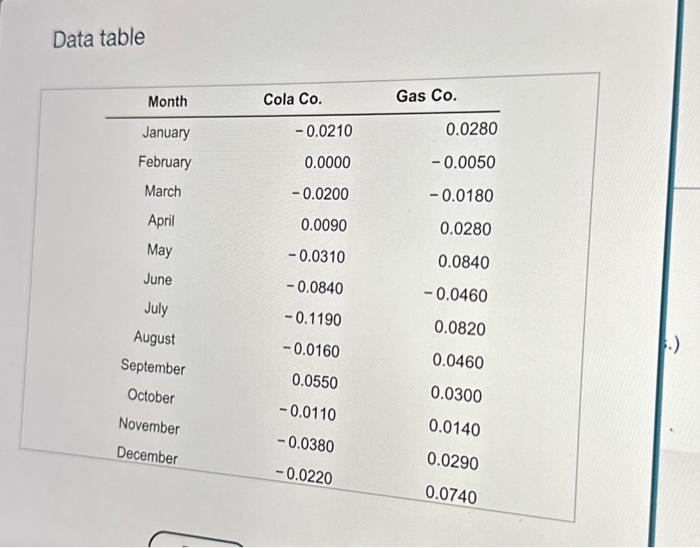

Question: Data table The following table contains monthly returns for Cola Co. and Gas Co. for 2013 (the returns are shown in decimal form, i.e., 0.035

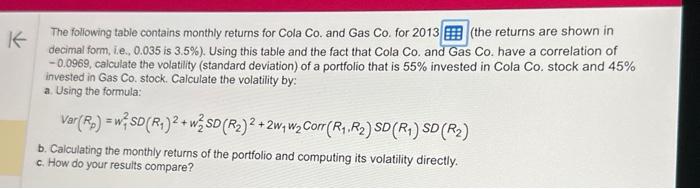

Data table The following table contains monthly returns for Cola Co. and Gas Co. for 2013 (the returns are shown in decimal form, i.e., 0.035 is 3.5% ). Using this table and the fact that Cola Co. and Gas Co. have a correlation of -0.0969 , calculate the volatility (standard deviation) of a portfolio that is 55% invested in Cola Co. stock and 45% invested in Gas Co. stock. Calculate the volatility by: a. Using the formula: Var(Rp)=w12SD(R1)2+w22SD(R2)2+2w1w2Corr(R1,R2)SD(R1)SD(R2) b. Calculating the monthly returns of the portfolio and computing its volatility directly. c. How do your results compare

Step by Step Solution

There are 3 Steps involved in it

We are asked to calculate portfolio volatility in two ways Lets proceed stepbystep Given Data From the image Month Cola Co Gas Co Jan 00210 00280 Feb 00000 00050 Mar 00200 00180 Apr 00090 00280 May 00... View full answer

Get step-by-step solutions from verified subject matter experts