Question: Directions: Match Column A with Column B. Write your answels on a separate sheet of paper. A B 1. It is the most basic journal.

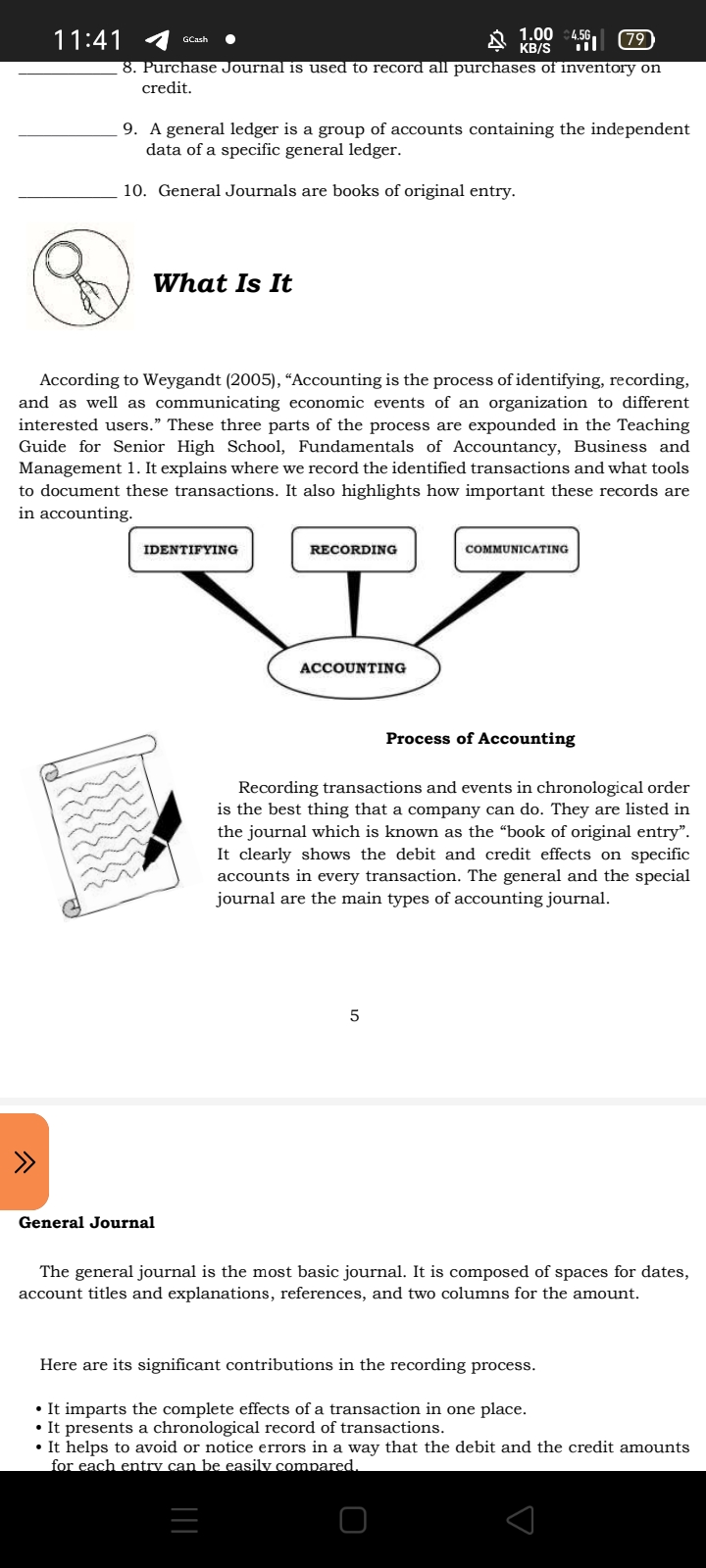

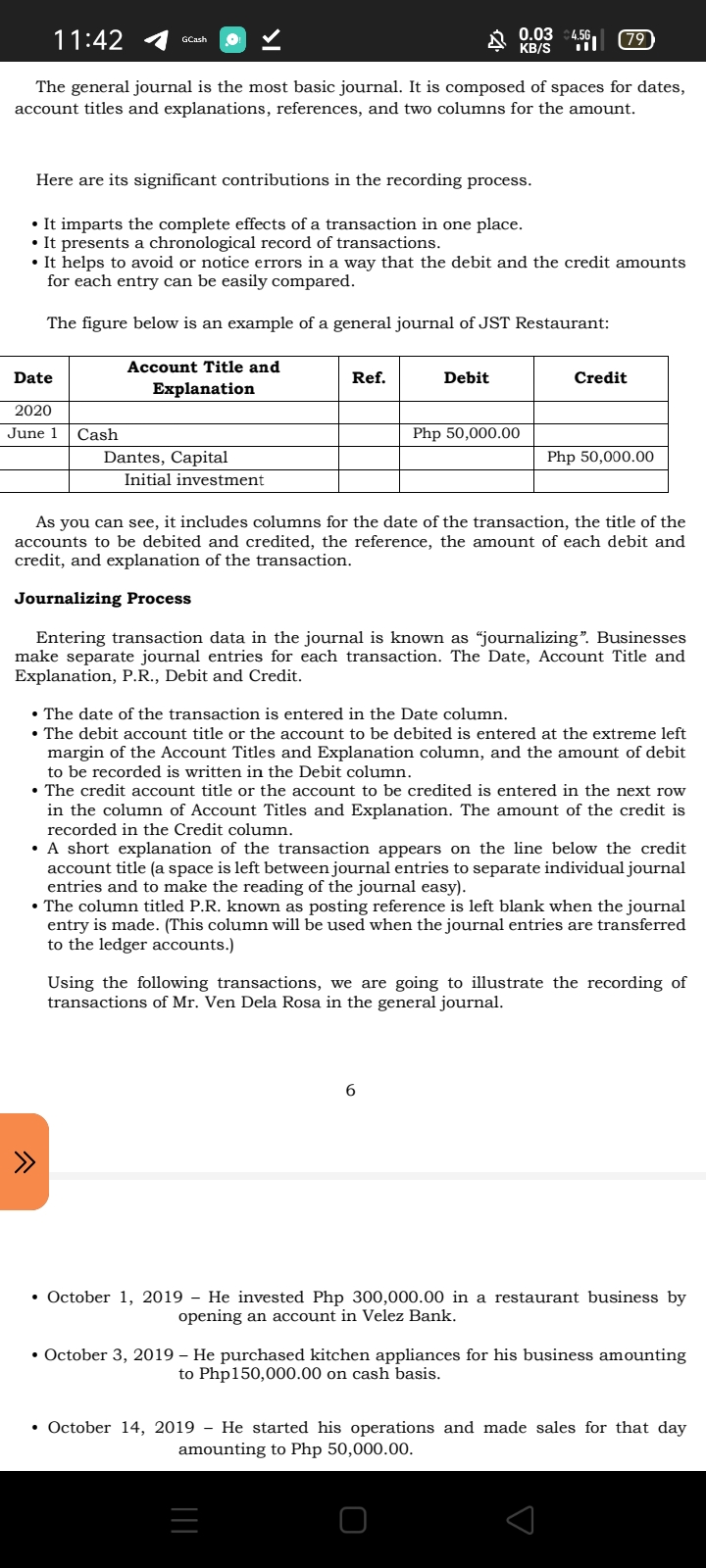

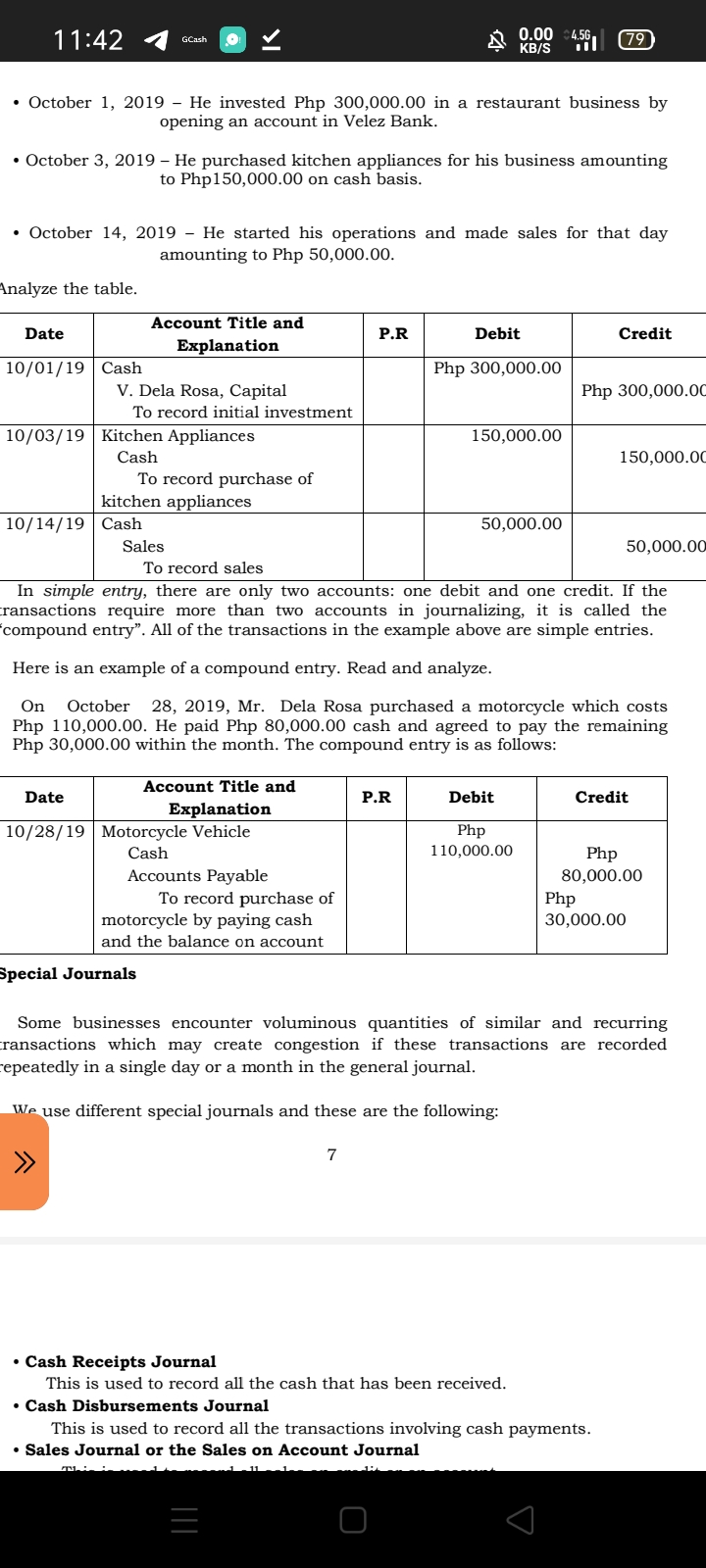

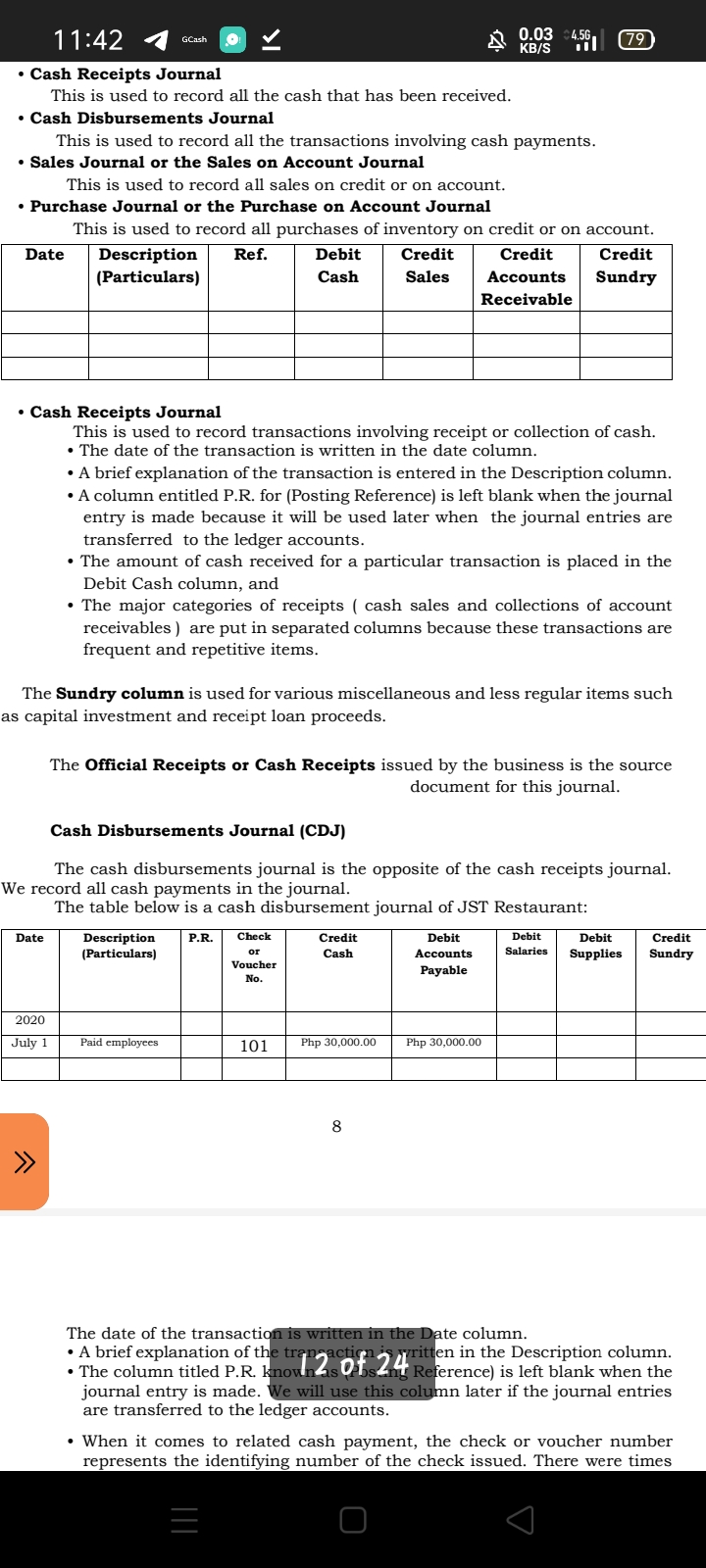

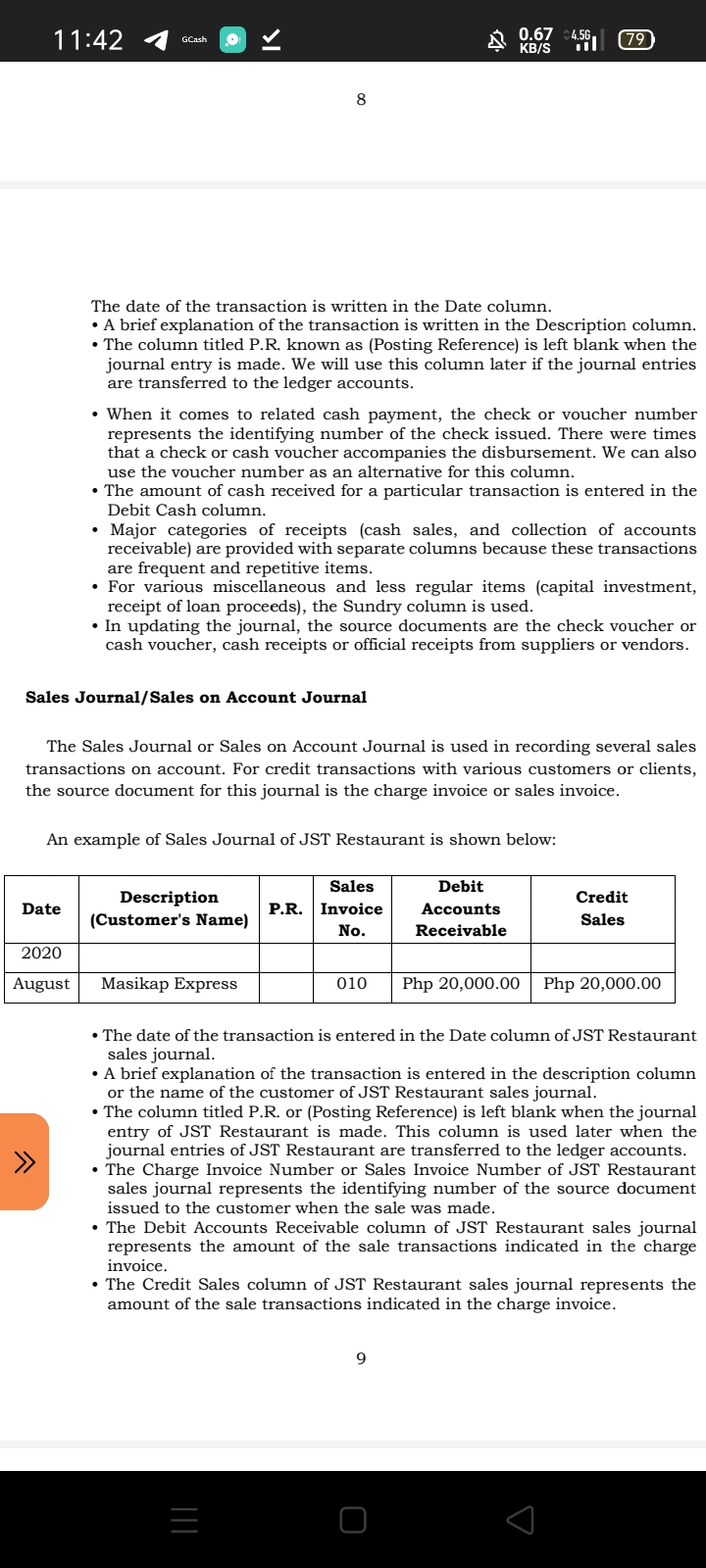

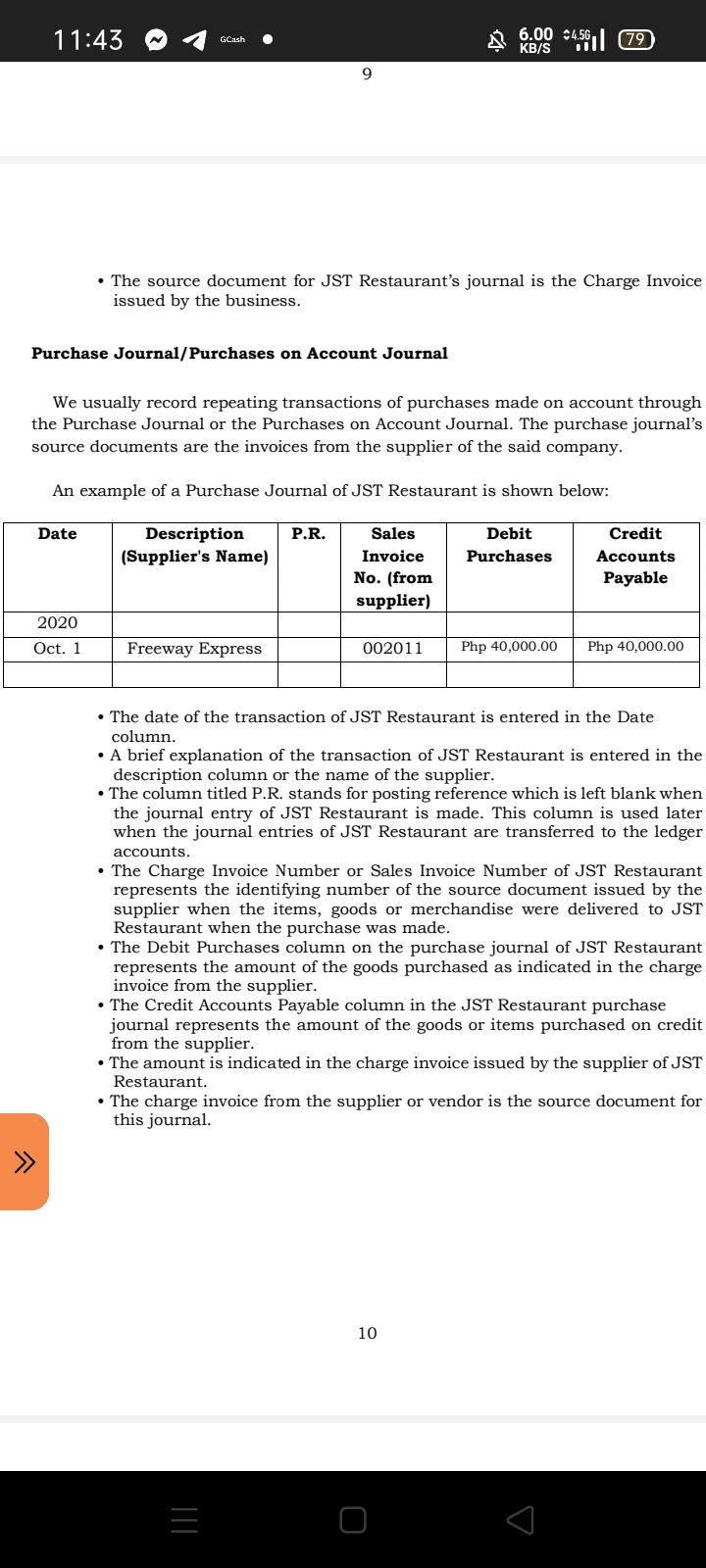

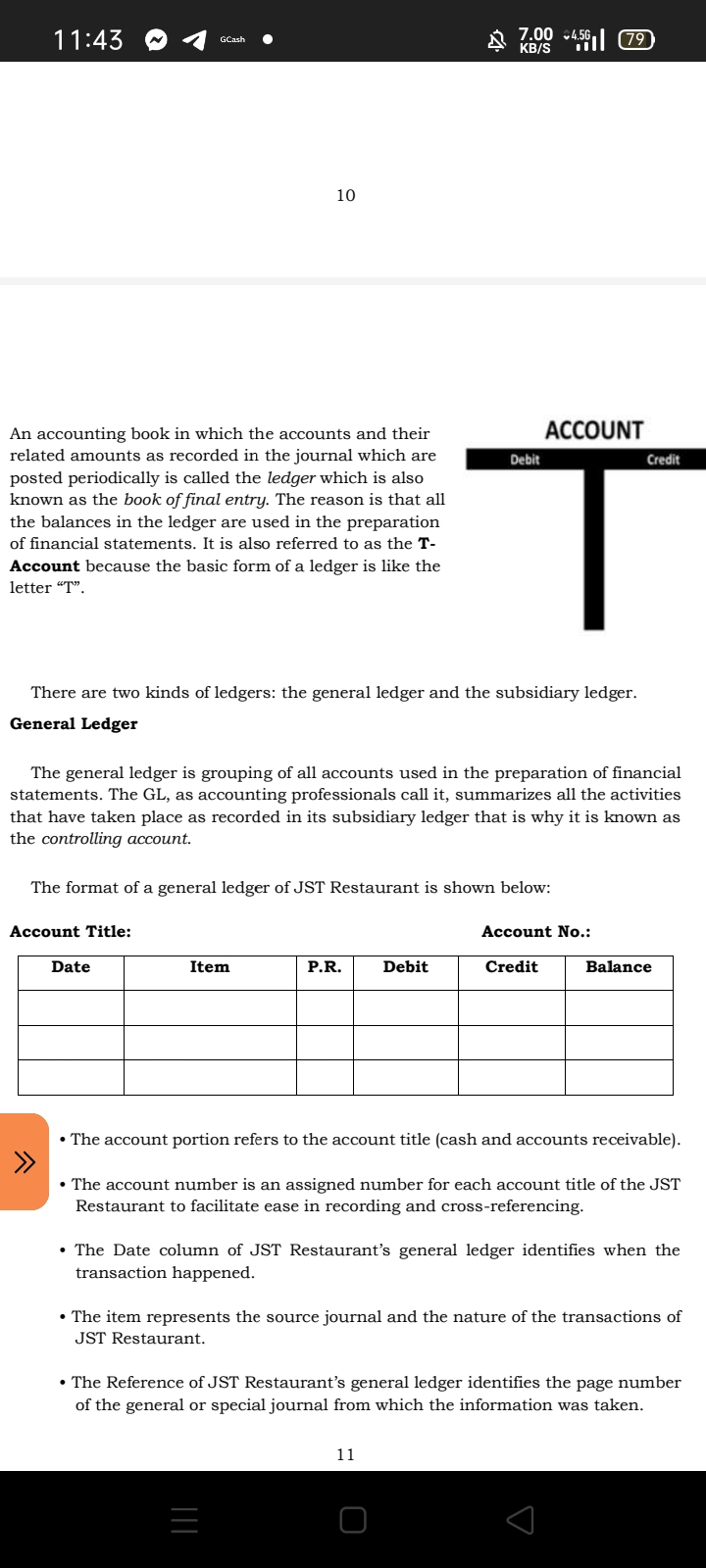

Directions: Match Column A with Column B. Write your answels on a separate sheet of paper. A B 1. It is the most basic journal. A. Purchase Journal 2. It is used to record all purchases. B. General Journal 3. It is used for various miscellaneous. C. Sundry Column 4. It is the opposite of cash receipt journal. D. Journalizing Process 5. It is the process entering transacan data E. Cash Disbursement in the journal. Journal Books are essential to all of us. They are a common source of information and an integral tool for learning. In every eld of study, There is a specialized book to be used. Books can also be used for documenting or recording important data, such as in the eld of business, particularly in accounting. Accountants use general journal and ledger and other special journals for different business transactions. These are like books where you can nd mostly nancial information and records of transactions which can be used as reference in decision-making for the success of one's business management. The general journal is the \"book of original entry\" where you can nd the initial record of the transactions of a rm while the ledger contains the total or balance of each account. @ What's In Directions: Identify what is described in each number. Choose your answer from the box. Write your answers on a separate paper. Chart of Accounts Notes Payable Liabilities Non-Current Asset Owner's Equity Notes Receivable Assets Prepaid Expenses Capital Cash 1. These are the debt of the company payable in money, goods, or services. 2. It is the list of all the accounts of the company that is being used by the rm to their- nancial records. 3. These are the resources owned by the owner. 4. It is the claim of the owner on the business. Directions: Identify what is described in each number. Choose your answer from the box. Write your answers on a separate paper. Chart of Accounts Notes Payable Liabilities Non-Current Asset Owner's Equity Notes Receivable Assets Prepaid Expenses Capital Cash 1. These are the debt of the company payable in money, goods, or services. 2. It is the list of all the accounts of the company that is being used by the rm to their nancial records. 3. These are the resources owned by the owner. 4. It is the claim of the owner on the business. 5. It is the most liquid asset. 6. It is a written note from the customer to pay his account on a given time and date. 7. Land and building are examples of these assets. 8. These are debts that are supported with awritten note or promise. 9. These are the resources or assets that have been invested in the business. 10. These are the bills paid in advance. Notes to the Teacher This module prepares students to differentiate a journal from a ledger and identify their types. @ What's New Directions: Read each statement below carefully. Write T if you think the statement is true and P if the statement is false. Write your answers on a separate sheet of paper. Notes to the Teacher This module prepares students to differentiate a journal from a ledger and identify their types. @ What's New Directions: Read each statement below carefully. Write T if you think the statement is true and F if the statement is false. Write your answers on a separate sheet of paper. 1. The general ledger is the most basic journal. 2. In recording, you are entering data transaction in the journal. 3. All entries involve only two accounts: one debit and one credit. 4. Accounting is the process of identifying, recording, and communicating economic events. 5. Cash Disbursement Journal is used to record all cash that have been received. 6. Cash Receipts Journal is used to record all transactions involving cash payments. 7. Sales Journal is used to record all sales on credit. 8. Purchase Journal is used to record all purchases of inventory on credit. 9. A general ledger is a group of accounts containing the independent data of a specific general ledger. 10. General Journals are books of original entry. What Is It According to Weygandt (2005], \"Accounting is the process of identifying, recording, and as well as communicating economic events of an organization to different interested users.\" These three parts of the process are expounded in the Teaching Guide for Senior High School, Fundamentals of Accountancy, Business and Management 1. It explains where we record the identified transactions and what tools to document these transactions. It also highlights how important these records are in accounting. 9. A general ledger is a group of accounts containing the independent data of a specific general ledger. 10. General Journals are books of original entry. What Is It According to Weygandt (2005], \"Accounting is the process of identifying, recording, and as well as communicating economic events of an organization to different interested users.\" These three parts of the process are expounded in the Teaching Guide for Senior High School, Fundamentals of Accountancy, Business and Management 1. It explains where we record the identied transactions and what tools to document these transactions. it also highlights how important these records are in accounting. Process of Accounting Recording transactions and events in chronological order is the best thing that a company can do. They are listed in the journal which is known as the \"book of original entry\". It clearly shows the debit and credit effects on specic accounts in every transaction. The general and the special journal are the main types of accounting journal. General Jamal The general journal is the most basic journal. [t is composed of spaces for dates, account titles and explanations, references, and two columns for the amount. Here are its signicant contributions in the recording process. - It imparts the complete effects of a transaction in one place. . It presents a chronological record of transactions. - It helps to avoid or notice errors in a way that the debit and the credit amounts The general journal is the most basic journal. It is composed of spaces for dates, account titles and explanations, references, and two columns for the amount. Here are its signicant contributions in the recording process. - [t imparts the complete effects of a transaction in one place. . It presents a chronological record of transactions. . It helps to avoid or notice errors in a way that the debit and the credit amounts for each entry can be easily compared. The gure below is an example of a general journal of JST Restaurant: Date nmngd Ref. Debit Credit 2020 June 1 Cash Php 50,000.00 Dantes, Capital Php 50,000.00 Initial investment As you can see, it includes columns for the date of the transaction, the title of the accounts to be debited and credited, the reference, the amount of each debit and credit, and explanation of the transaction. Journalizing Process Entering transaction data in the journal is known as \"journalizing\". Businesses make separate journal entries for each transaction. The Date, Account Title and Explanation, P.R., Debit and Credit. . The date of the transaction is entered in the Date column. . The debit account title or the account to be debited is entered at the extreme left margin of the Account Titles and Explanation column, and the amount of debit to be recorded is written in the Debit column. . The credit account title or the account to be credited is entered in the next row in the column of Account Titles and Explanation. The amount of the credit is recorded in the Credit column. . A short explanation of the transaction appears on the line below the credit account title (a space is left between journal entries to separate individual journal entries and to make the reading of the journal easy]. . The column titled RR. known as posting reference is left blank when the journal entry is made. [This columnwiil be used when the journal entries are transferred to the ledger accounts.) Using the following transactions, we are going to illustrate the recording of transactions of Mr. Ven Dela Rosa in the general journal. 0 October 1, 2019 He invested Php 300,000.00 in a restaurant business by opening an account in Velez Bank. 0 October 3, 2019 He purchased kitchen appliances for his business amounting to Php150,000.00 on cash basis. 0 October 14, 2019 He started his operations and made sales for that day amounting to Php 50,000.00. - October 1, 2019 He invested Php 300,000.00 in a restaurant business by opening an account in Velez Bank. 0 October 3, 2019 He purchased kitchen appliances for his business amounting to Php150,000.00 on cash basis. - October 14, 2019 He started his operations and made sales for that day amounting to Php 50,000.00. analyze the table. Account Title and Date Explanation RR Debit Credit 10301,! 19 Cash Php 300,000.00 V. Dela Rosa, Capital Php 300,000.0 To record initial investment 10;'03,rt 19 Kitchen Appliances 150,000.00 Cash 150,000.0C To record purchase of kitchen appliances 10/14/19 Cash 50,000.00 Sales 50,000.00 To record sales In simple entry, there are only two accounts: one debit and one credit. If the ransactions require more than two accounts in journalizing, it is called the 'compound entry\". All of the transactions in the example above are simple entries. Here is an example of a compound entry. Read and analyze. On October 28, 2019, Mr. Dela Rosa purchased a motorcycle which costs Php 110,000.00. He paid Php 80,000.00 cash and agreed to pay the remaining Php 30,000.00 within the month. The compound entry is as follows: Account Title and Date Explanation PR Debit Credit 10/28} 19 Motorcycle Vehicle Php Accounts Payable 80,000.00 To record purchase of Php motorcycle by paying cash 30,000.00 and the balance on account Special Journals Some businesses encounter voluminous quanties of similar and recurring ransactions which may create congestion if these transactions are recorded repeatedly in a single day or a month in the general journal. use different special journals and these are the following: 7 - Cash Receipts Journal This is used to record all the cash that has been received. - Cash Disbursements Journal This is used to record all the transactions involving cash payments. - Sales Journal or the Sales on Account Journal - Cash Receipts Journal This is used to record all the cash that has been received. - Cash Disbursements Journal This is used to record all the transactions involving cash payments. - Sales Journal or the Sales on Account Journal This is used to record all sales on credit or on account. - Purchase Journal or the Purchase on Account Journal This is used to record all purchases of inventory on credit or on account. Date Description Ref. Debit Credit Credit Credit [Particulars] Cash Sales Accounts Sundry Receivable Cash Receipts Journal This is used to record transactions involving receipt or collection of cash. - The date of the transaction is written in the date column. - A brief explanation of the transaction is entered in the Description column. - A column entitled P.R. for [Posting Reference) is left blank when the journal entry is made because it will be used later when the journal entries are transferred to the ledger accounts. - The amount of cash received for a particular transaction is placed in the Debit Cash column, and - The major categories of receipts I: cash sales and collections of account receivables ) are put in separated columns because these transactions are frequent and repetitive items. The Sundry column is used for various miscellaneous and less regular items such as capital investment and receipt loan proceeds. The Ofcial Receipts or Cash Receipts issued by the business is the source document for this journal. Cash Disbursements Journal (CDJj The cash disbursements journal is the opposite of the cash receipts journal. We record all cash payments in the journal. The table below is a cash disbursement journal of J ST Restaurant: M: Denmiptkm an. M Credit Debit Mt Debit Credit [Particulars] W Cash mu m Supplies Sundry Foam p I] 2020 July 1 Paid employees 101 Flip 30,000.00 Php 30,000.00 8 The date of the transacti te column. - A brief explanation of n in the Description column. - The column titled P.R. erence} is left blank when the journal entry is made. later if the journal entries are transferred to the ledger accounts. - When it comes to related cash payment, the check or voucher number represents the identifying number of the check issued. There were times The date of the transaction is written in the Date column. I A brief explanation of the transaction is written in the Description column. I The column titled PR. known as [Posting Reference} is left blank when the journal entry is made. We will use this column later if the journal entries are transferred to the ledger accounts. I When it comes to related cash payment, the check or voucher number represents the identifying number of the check issued. There were times that a check or cash voucher accompanies the disbursement. We can also use the voucher number as an alternative for this column. I The amount of cash received for a particular transaction is entered in the Debit Cash column. I Major categories of receipts {cash sales, and collection of accounts receivable} are provided with separate columns because these transactions are frequent and repetitive items. I For various miscellaneous and less regular items (capital investment, receipt of loan proceeds], the Sundry column is used. I In updating the journal, the source documents are the check voucher or cash voucher, cash receipts or ofcial receipts from suppliers or vendors. Sales JournallSale-s on Account Journal The Sales Journal or Sales on Account Journal is used in recording several sales transactions on account. For credit transactions with various customers or clients, the source document for this journal is the charge invoice or sales invoice. An example of Sales Journal of JST Restaurant is shown below: Description Sales Debit c t Date [Customer's Name) P'R- Invoice Accounts \"\"1: Na. Receivable sale 2020 August Masikap Express 010 Php 20,000.00 Php 2030030 I The date of the transaction is entered in the Date column of JST Restaurant sales journal. I A brief explanation of the transaction is entered in the description column or the name of the customer of JST Restaurant sales journal. I The column titled ER. or (Posting Reference) is left blank when the journal entry of JST Restaurant is made. This column is used later when the journal entries of JST Restaurant are transferred to the ledger accounts. I The Charge Invoice Number or Sales Invoice Number of JST Restaurant sales journal represents the identifying number of the source document issued to the customer when the sale was made. I The Debit Accounts Receivable column of JST Restaurant sales journal represents the amount of the sale transactions indicated in the charge mvorce. I The Credit Sales column of JST Restaurant sales journal represents the amount of the sale transactions indicated in the charge invoice. 11:45 9 4 . - The source document for J ST Restaurant's journal is the Charge Invoice issued by the business. Purchase Journalll'urehases on Account Journal We usually record repeating transactions of purchases made on account through the Purchase Journal or the Purchases on Account Journal. The purchase journal's source documents are the invoices from the supplier of the said company. An example of a Purchase Journal of J ST Restaurant is shown below: Date Description ER. Sales Debit Credit (Supplier's Name] Invoice Purchases Accounts No. [from Payable supplier] 2020 Oct. 1 Freeway Express 00201 1 1\"1'11: 40900-00 Php 40.00030 - The date of the transaction of JST Restaurant is entered in the Date column. - A brief exploitation of the transaction of JST Restaurant is entered in the description column or the name of the supplier. - The column titled RR. stands for posting reference which is left blank when the journal entry of JST Restaurant is made. This column is used later when the journal entries of JST Restaurant are transferred to the ledger accounts. - The Charge Invoice Number or Sales Invoice Number of J ST Restaurant represents the identifying number of the source document issued by the supplier when the items, goods or merchandise were delivered to JST Restaurant when the purchase was made. - The Debit Purchases column on the purchase journal of JST Restaurant represents the amount of the goods purchased as indicated in the charge invoice from the supplier. - The Credit Accounts Payable column in the J ST Restaurant purchase journal represents the amount of the goods or items purchased on credit from the supplier. - The amount is indicated in the charge invoice issued by the supplier of J ST Restaurant. - The charge invoice from the supplier or vendor is the source document for this journal. 10 11:45 a 4 . 10 An accounting book in which the accounts and their ACCOUNT related amounts as recorded in the journal which are posted periodically is called the ledger which is also known as the book ofnal entry. The reason is that all the balances in the ledger are used in the preparation of nancial statements. It is also referred to as the 1'- Account because the basic form of a ledger is like the letter \"T\". There are two kinds of ledgers: the general ledger and the subsidiary ledger. General Ledger The general ledger is grouping of all accounts used in the preparation of nancial statements. The GL, as accounting professionals call it, summarizes all the activities that have taken place as recorded in its subsidiary ledger that is why it is known as the controlling account. The format of a general ledger of J ST Restaurant is shown below: Account Title: Account No.: Date Item ER. Debit Credit Balance . The account portion refers to the account title [cash and accounts receivable}. - The account number is an assigned number for each account title of the JST Restaurant to facilitate ease in recording and cross-referencing. - The Date DDhlIIll'l of JST Restaurant's general ledger identies when the transaction happened. - The item represents the source journal and the nature of the transactions of J ST Restaurant. . The Reference of JST Restaurant's general ledger identies the page number of the general or special journal from which the information was taken. 11 11:45 64 . The item represents the source journal and the nature of the transactions of transaction appen - . . J ST Restaurant. - The Reference of JST Restaurant's general ledger identifies the page number of the general or special journal from which the information was taken. - The Debit and Credit columns are used in recording the number of 11 transactions from the general journal or special journal. - The Balance Column of JST Restaurant's general ledger represents the running balance of the Account after considering the debit and credit amounts. If the running balance amount is positive, the account has a debit balance whereas if it has a negative running balance, the accounts have a credit balance. Subsidiary Ledger A subsidiary ledger is a group of similar accounts that consists of an independent data of a specic general ledger. It is ofcially created or maintained ii individualized data is needed for a specic general ledger account. Individual record of various payables to suppliers is the best example of a subsidiary ledger. When we total the amount of all subsidiary ledgers it should equal the balance in the Accounts Payable of the general ledger. A format of subsidiary ledgers of JST Restaurant is shown below: Accounts Payable Subsidiary Ledger Vendor! Supplier: Vendor No.: Address: Date Item ER. Debit Credit Balance - The upper portion indicates the name and address of the vendor or supplier of J ST Restaurant. - The vendor number of JST Restaurant's subsidiary ledger is an assigned number for each vendor as a reference in keeping the records of a supplier. - The Date column of JST Restaurant's subsidiary ledger identifies when the transaction happened. - The description column of JST Restaurant's subsidiary ledger describes the nature of the transaction. - The Reference of JST Restaurant's subsidiary ledger identies the page number of the general or special journal from which the information was taken. 11:43 ~ GCash 0.04 KB/S Will 79 . The description column of JST Restaurant's subsidiary ledger describes the nature of the transaction. . The Reference of JST Restaurant's subsidiary ledger identifies the page number of the general or special journal from which the information was taken. 12 . The Debit and Credit columns of JST Restaurant's subsidiary ledger reflect the various effects of every transaction to the record of the supplier or vendor. . The Balance column of JST Restaurant's subsidiary ledger provides the running balance of every supplier. Take note that the total running balance for all subsidiary ledgers of JST Restaurant should be equal to the accounts payable in the general ledger. What's More Directions: Identify the appropriate journal to be used in each item below. Choose from the book of accounts listed in the box. Write your answers on a separate sheet of paper. General Journal Sales Journal Purchase Journal Cash Receipt Journal Cash Disbursement Journal 1. Mr. Ong invested an equipment on his own business worth of Php 200,000.00. 2. Aling Lita sold merchandise on account worth of Php 3,000.00. 3. Mr. Valdez purchased a vehicle worth of Php 150,000.00 on account. 4. Rhea received Php 20,000.00 for the services that she rendered. 5. Janice paid the salaries of her employees on her accounting firm with the amount of Php 30,000.00. > > 6. Khariz bought office supplies on cash basis amounting to Php 2,000.00. 7. Trishi received cash of Php 5,000.00 on the sales she made. 8. Mr. Melbourne purchased supplies amounting to Php 1,500.00 with the terms of 2/2, n/30. 9. Julie sold merchandise amounting to Php 20,000.00 with the terms of 2/5, n/30. 10. Mr. Ong withdrew cash worth of Php 3,000.00 for his personal use. E O11:44 49 What I Have Learned Directions: Fill in the blanks with the correct accounting term;t s. Choose the answers from the box below and write them on a separate sheet of paper. Chronological General ledger Compound Entry Subsidiary ledger Cash Receipts Journal Purchase Journal Cash Disbursement Journal ledger Special Journal Journalizing Special Journal Date Simple entry Communicating Description Column {ANDI 9. . Entering transaction data in the journal is known as . An entry that requires three or more accounts is called . An entry that only involves one debit and one credit is known as . Recording transactions involving receipt or collection of cash is called . The journal where all cash payments are recorded is known as . The accounting book in which the accounts and their related amounts are recorded' in the journal' is referred to as _ The grouping of all accounts used' In the preparation of nancial statements is called . The group of accounts containing the independent data of a specic general ledger 1s referred to as Recurring transactions of purchases on account are recorded in 10. Cash Receipts Journal, Cash Disbursement Journal, Sales Journal are examples of 11. Accounting re the pI'OCESS of identifying, recording and . 12. Companies initially record transactions and events in order. 13.There are two types of journals: the general journal and 14.A brief explanation of the transaction is entered in the 15.The date of transaction is entered in the column. 14 [901'24 11:44 O 4 . 14 What I Can Do Directions: Answer the following questions in 3-5 sentences. Write your answers on a separate sheet of paper. 1. How are you going to differentiate General Ledger from a Subsidiary Ledger? 2. How are you going to differentiate General Journal from a General Ledger? 3. What are the different types of special journals? 4. Why do companies use special journals? 5. What are the advantages of using a special journal? 15 11:44 a 4 . Assessment Directions: Identify what is described in each number. Write the letter of your answer on a separate sheet of paper. 1. This is the book of original entry. A. ledger C. subsidiary ledger B. special journal D. general journal 2. This is the book of nal entry. A. general journal C. subsidiary ledger B. general ledger D. special journals 3. This is used to record purchases on account. A. sales journal C. general journal B. purchase journal D. cash receipts journal 4. This is used to record sales on credit. A. cash disbursement journal C. sales journal B. purchase journal D. ledger 5. This is used to record cash receipts. A. ledger C. cash disbursement journal B. cash receipts journal D. journal 6. This is used to record cash payments. A. cash disbursement journal C. purchase journal B. cash receipts journal D. sales journal 7. This contains the details supporting the balance in the general ledger account. A. general ledger C. ledger B. subsidiary ledger D. none of the above 8. This is also known as the controlling account. A. cash receipts journal C. accounts receivable B. notes payable D. general ledger 9. This type of entry involves only two accounts: one debit and one credit. A. compound entry C. simple entry B. dual entry D. jumbled entry 10.1t is an entry that requires three or more accounts. A. compound entry C. simple entry B. dual entry D. jumbled entry 1 1.This type of special journal makes use of ofcial receipts issued by companies. A. cash disbursement C. purchase journal B. cash receipts D. sales journal 16 12.This is the type of special journal makes use of sales invoices issued by companie A. purchase journal C. cash receipt journal B. sales journal D. cash disbursement journal 13.This is the type of special journal Where sales invoice from a supplier may be four A. sales journal C. cash receipt journal B. purchase journal D. cash disbursement journal 11:44 94 11_Th.is type of special journal makes use of ofcial receipts issued by companies. A. cash disbursement C. purchase journal B. cash receipts D. sales journal 16 12.Th.is is the type of special journal makes use of sales invoices issued by companies. A. purchase journal C. cash receipt journal B. sales journal D. cash disbursement journal 13.This is the type of special journal where sales invoice from a supplier may be found A. sales journal C. cash receipt journal B. purchase journal D. cash disbursement journal l4.This is the type of special journal where oicial receipts from suppliers as proof of payment may be found. A. cash disbursement journal C. purchase journal B. cash receipt journal D. sales journal 15.A cash disbursement journal or cash payments journal is not used to record this transaction. A. purchase of merchandise for cash C. all cash received B. purchase of merchandise on D. payment to creditors and account suppliers Additional Activities Directions: The following are transactions from Marvin Hernandez's book of account. Decide which journal to use in each of the given transactions. Write the letters of your answer on the separate sheet of paper. A. Cash Receipts Journal B. Cash Disbursement Journal C. General Journal D. Sales Journal E. Purchase Journal . . Collected Php10,000.00 from a customer in payment of his account . Bought 100 pieces of mugs to be sold in the store amounting to Php1,500.00 on credit . Sold ve pieces of mugs to Mr. X, Php 320.00 cash . Sold two pieces of mugs to Mr. Y, Php 112.00 cash . Purchased ofce supplies for cash, Php 500.00 . Paid Php 20,000.00 monthly rental . Paid salary of staff, Php15,000.00. . Sold 100 pieces of mugs to Cuppy, Inc., Php 5,600.00 on account . Sold 500 pieces of mugs to Muggy Corp. for Php 15,300.00 payable one month after delivery 10. Purchased on account 1,000 pieces of mugs for Php12,400.00 [Q condom-ow 17

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!