Question: DO NOT ANSWER IN EXCEL PLEASE, THIS IS PAPER TEST Question 5. Answer all parts I. Consider the following information about the performance of two

DO NOT ANSWER IN EXCEL PLEASE, THIS IS PAPER TEST

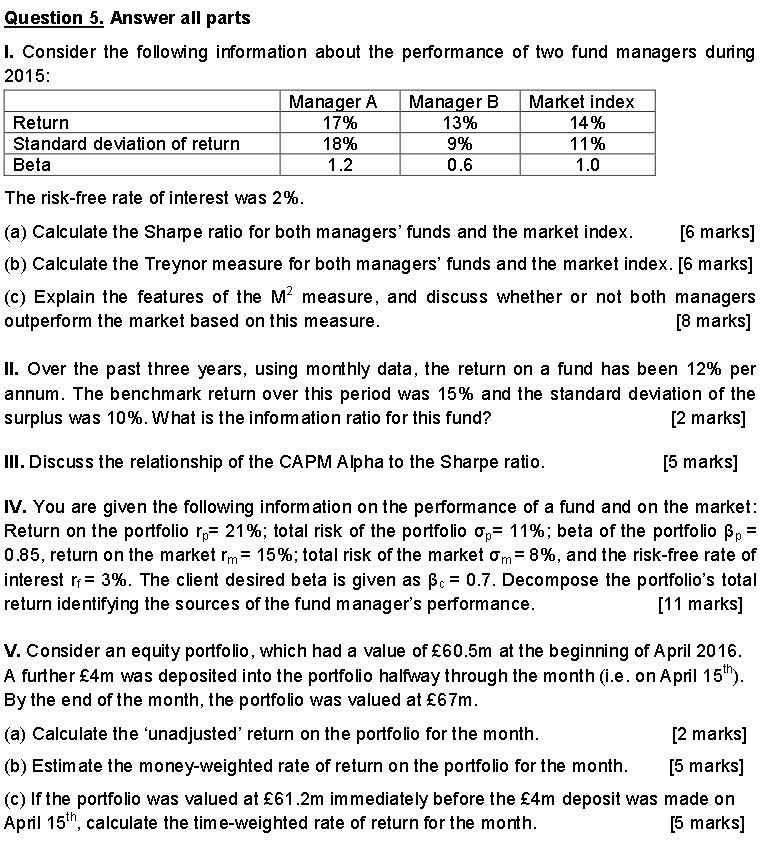

Question 5. Answer all parts I. Consider the following information about the performance of two fund managers during 2015 Manager A Manager B Market index 13% 9% 0.6 Return 17% 18% 14% 11% Standard devation of return Beta The risk-free rate of interest was 2% (a) Calculate the Sharpe ratio for both managers' funds and the market index. (b) Calculate the Treynor measure for both managers' funds and the market index. [6 marks] (c) Explain the features of the M2 measure, and discuss whether or not both managers outperform the market based on this measure [6 marks] [8 marks] ll. Over the past three years, using monthly data, the return on a fund has been 12% per annum. The benchmark return over this period was 15% and the standard deviation of the surplus was 10%. What is the information ratio for this fund? [2 marks] III. Discuss the relationship of the CAPM Alpha to the Sharpe ratio [5 marks] IV. You are given the following information on the performance of a fund and on the market Return on the portfolio r,-21%; total risk of the portfolio ,-11%; beta of the portfolio p_ 0.85, return on the market rm-15%; total risk of the market m_ 8%, and the risk-free rate of interest r,-3%. The client desired beta is given as .-0.7. Decompose the portfolio's total return identifying the sources of the fund manager's performance 11 marks] V. Consider an equity portfolio, which had a value of 60.5m at the beginning of April 2016 A further 4m was deposited into the portfolio halfway through the month (i.e. on April 15 By the end of the month, the portfolio was valued at 67m (a) Calculate the 'unadjusted' return on the portfolio for the month (b) Estim ate the money-weighted rate of return on the portfolio for the month.[5 marks] (c) If the portfolio was valued at 61.2m immediately before the 4m deposit was made on April 15th, calculate the time-weighted rate of return for the month [2 marks] [5 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts