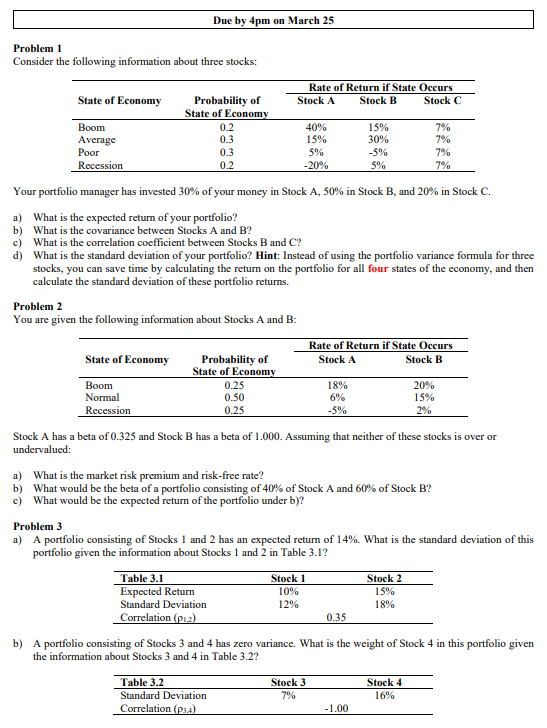

Question: Due by 4pm on March 25 Problem 1 Consider the following information about three stocks: Rate of Return if State Occurs State of Economy Probability

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts