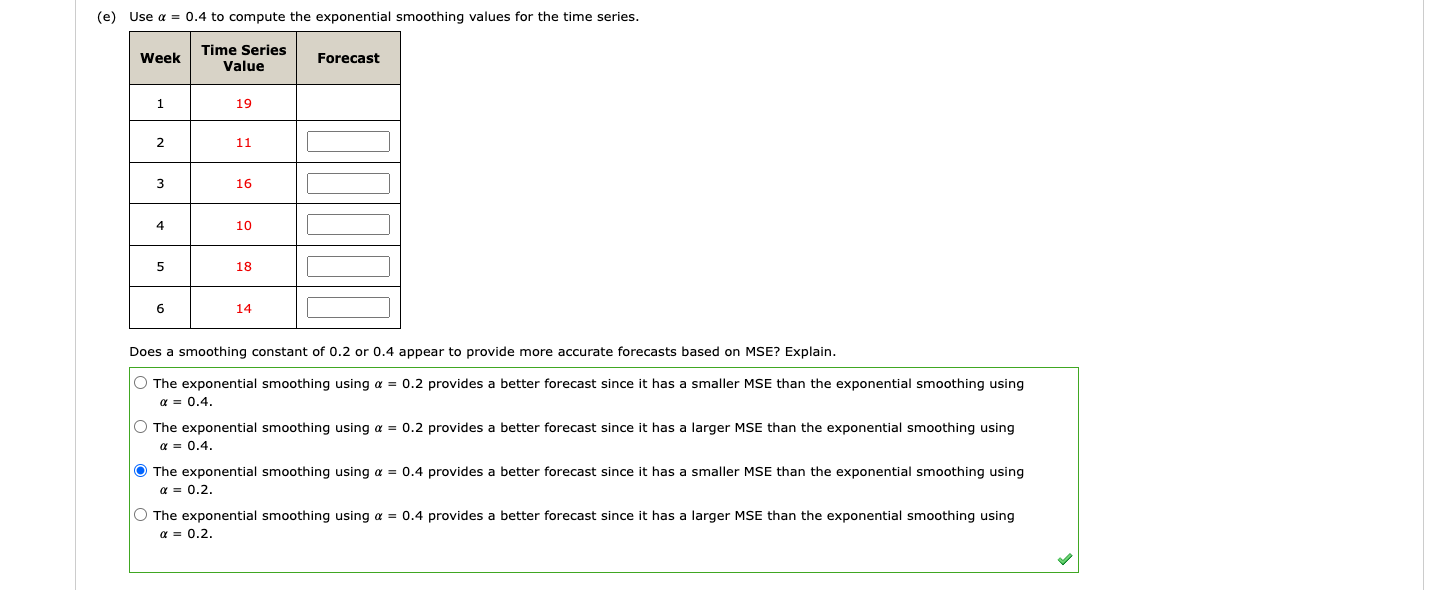

Question: (e) Use ( alpha=0.4 ) to compute the exponential smoothing values for the time series. Does a smoothing constant of 0.2 or 0.4 appear to

(e) Use \\( \\alpha=0.4 \\) to compute the exponential smoothing values for the time series. Does a smoothing constant of 0.2 or 0.4 appear to provide more accurate forecasts based on MSE? Explain. The exponential smoothing using \\( \\alpha=0.2 \\) provides a better forecast since it has a smaller MSE than the exponential smoothing using \\( \\alpha=0.4 \\). The exponential smoothing using \\( \\alpha=0.2 \\) provides a better forecast since it has a larger MSE than the exponential smoothing using \\( \\alpha=0.4 \\). The exponential smoothing using \\( \\alpha=0.4 \\) provides a better forecast since it has a smaller MSE than the exponential smoothing using \\( \\alpha=0.2 \\). The exponential smoothing using \\( \\alpha=0.4 \\) provides a better forecast since it has a larger MSE than the exponential smoothing using \\( \\alpha=0.2 \\)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts