Question: Each investment return must also be compared to a comparable benchmark to assess if the investment has over- or underperformed during the last 12 months.

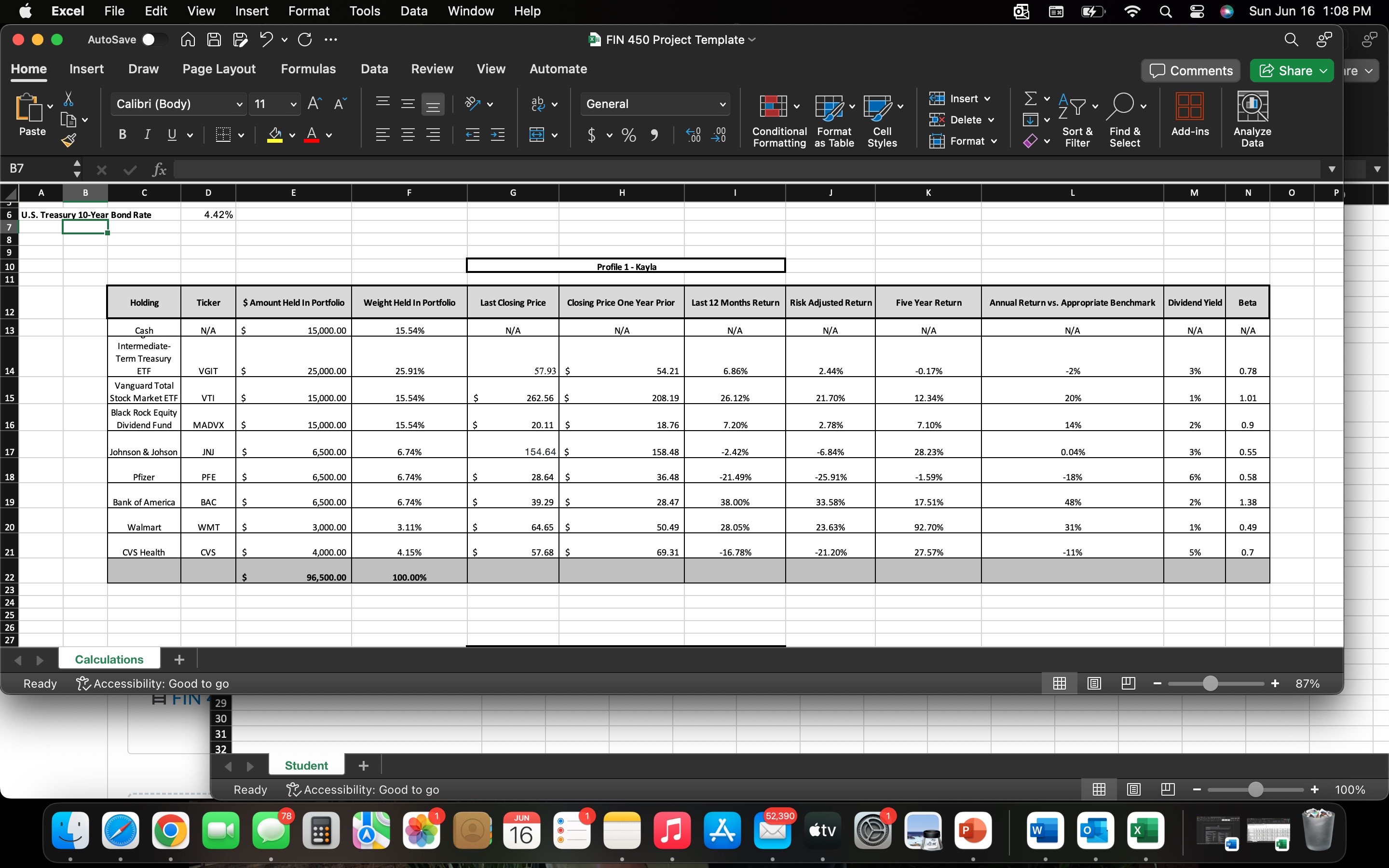

Each investment return must also be compared to a comparable benchmark to assess if the investment has over- or underperformed during the last 12 months. You can compare the last 12-month return of your investment to the last 12-month return of a bond index when the investment is a bond, a large stock market index when the investment is a stock, or individual stocks when the investment is a stock, and so on. Find a comparable benchmark and enter the difference between the portfolio investment's return and the benchmark in column L.

Specifically, you must address the following rubric criteria:

Analyze past portfolio performance. Include the following in your calculations:

Quantitative assessments from:

Annual return

Risk-adjusted return

Five-year return

Annual return versus appropriate benchmark

Compare portfolio investments to relevant benchmarks. Include the following in your calculations and summary:

Identify benchmarks for existing investments to be compared to, and identify the reason for benchmark selection.

Discuss return data on investments within the portfolio.

Identify over- and underperforming investments in relation to each benchmark.

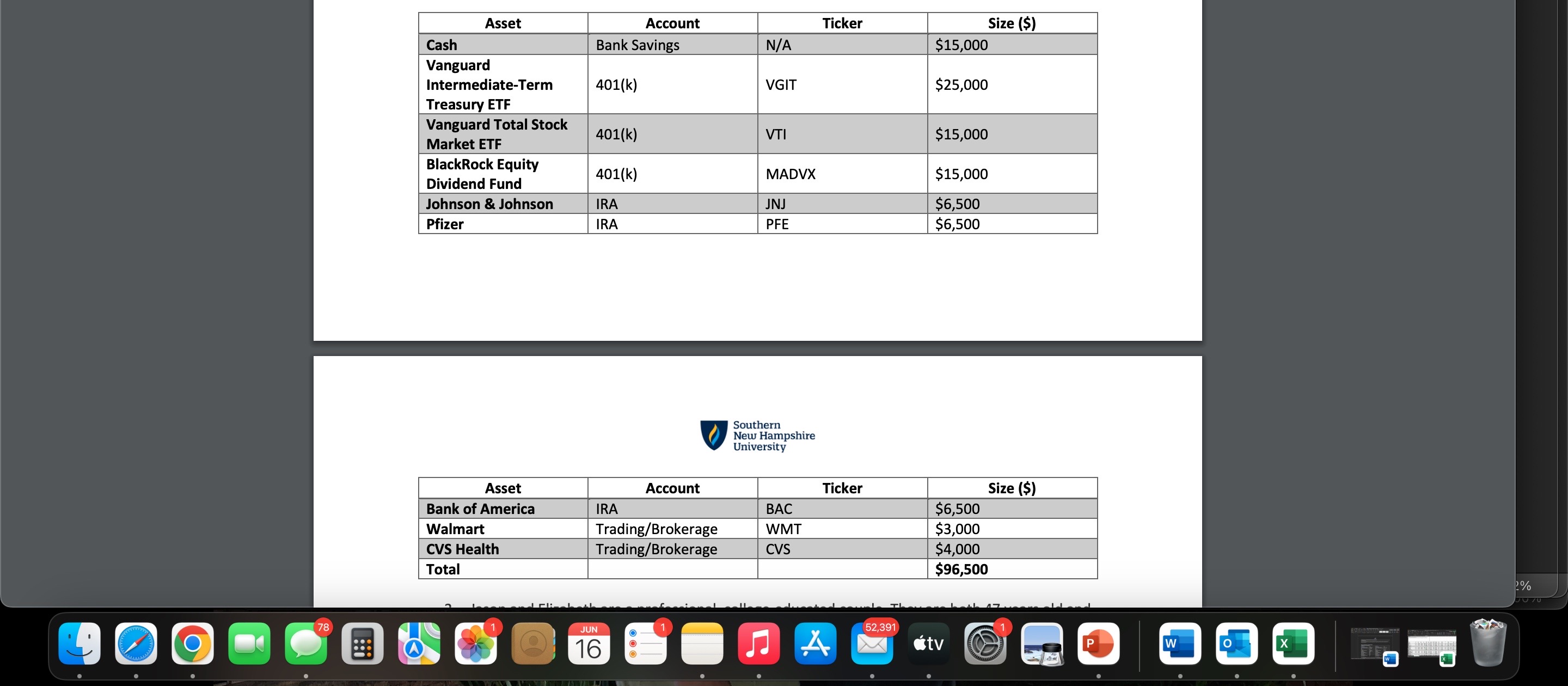

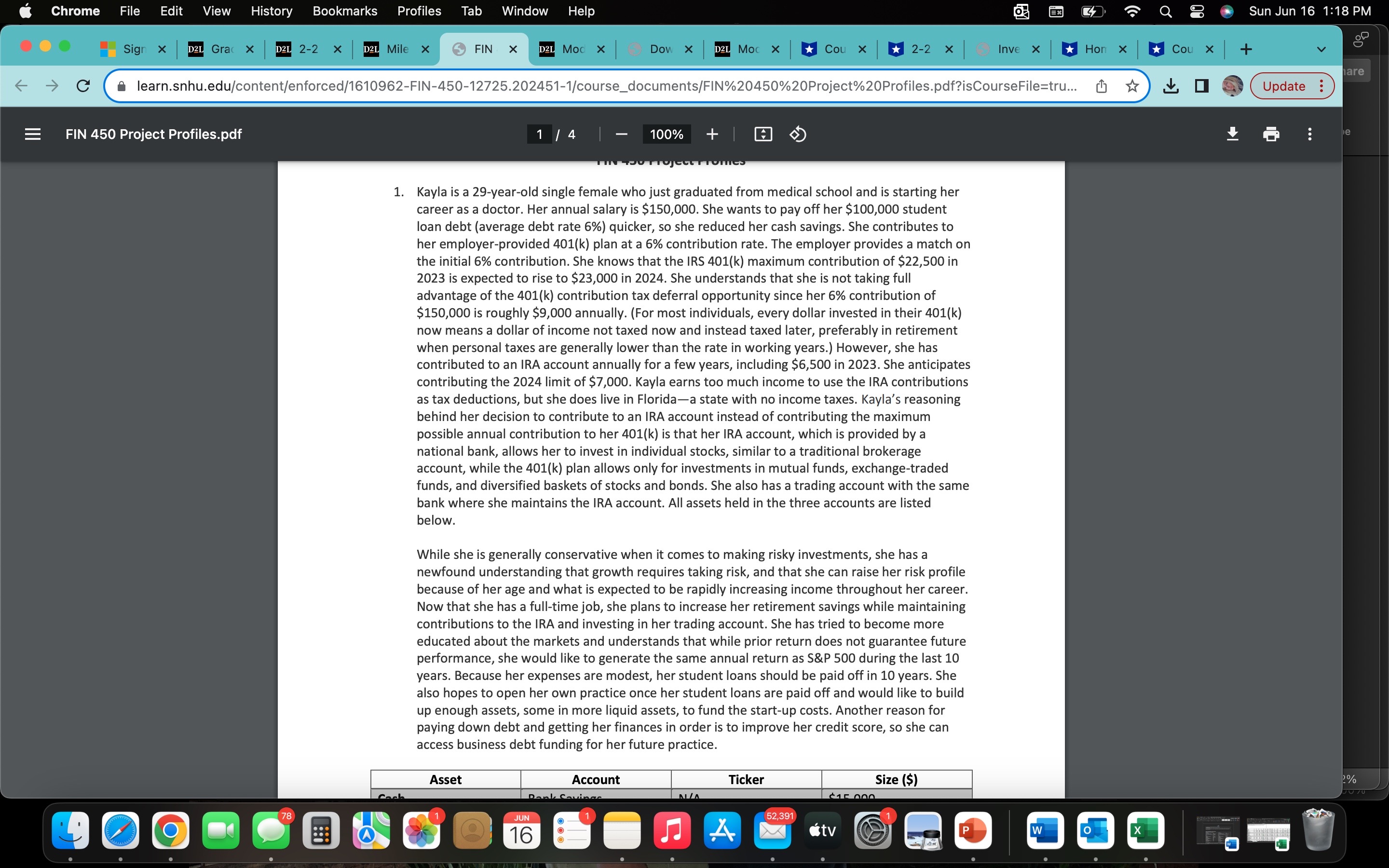

Excel File Edit View Insert Format Tools Data Window Help Q @ Sun Jun 16 1:08 PM AutoSave MAP ? C ... 3 FIN 450 Project Template Home Insert Draw Page Layout Formulas Data Review View Automate Comments Share re v Calibri (Body) 11 AA General Insert v Paste BIUV A Delete E V $ ~ % 9 Conditional Format Cell Sort & Find & Add-ins Styles Format v Analyze Formatting as Table Filter Select Data BZ X V fx D G H M U.S. Treasury 10-Year Bond Rate N 4.42% P Profile 1 - Kayla Holding Ticker 12 $ Amount Held In Portfolio Weight Held In Portfolio Last Closing Price Closing Price One Year Prior Last 12 Months Return Risk Adjusted Return Five Year Return Annual Return vs. Appropriate Benchmark Dividend Yield Beta 13 Cash N/A 15,000.00 15.54% N/A N/A N/A N/A Intermediate- N/A N/A N/A N/A Term Treasur 14 ETF VGIT 25,000.00 25.91% 57.93 $ 54.21 6.86% Vanguard Total 2.44% -0.17% -2% 39 0.78 Stock Market ETF VTI 15,000.00 15.54% Black Rock Equit S 262.56 $ 08.19 26.12% 21.70% 12.34% 20% 1% 1.01 16 Dividend Fund MADVX 15,000.00 15.54% $ 20.11 $ 18.76 7.20% 2.78% 7.10% 14% 2% 0.9 17 Johnson & Johson JN 6,500.00 6.74% 154.64 $ 58.48 -2.42% -6.84% 28.23% 0.04% 3% 0.55 18 Pfizer PEE 6,500.0 6.74% 28.64 $ 36.48 -21.49% -25.91% 1.59% -18% 6% 0.58 19 Bank of America BAC 6,500.00 6.74% 39.29 28.47 38.00% 33.58% 17.51% 48% 2% 1.38 20 Walmart WMT 3,000.00 3.11% 64.65 $ 50.49 28.05% 23.63% 92.70% 31% 1% 0.49 21 CVS Health CVS 4,000.00 4.15% 57.68 $ 69.31 -16.78% -21.20% 27.57% -11% 0.7 96,500.00 100.00% Calculations + Ready Accessibility: Good to go FIN 29 + 87% 30 31 32 Student + Ready Accessibility: Good to go + 100% 100 78 C JUN 52,390 16 4 tvAsset Account Ticker Size ($) Cash Bank Savings N/A $15,000 Vanguard Intermediate-Term 401(k) VGIT $25,000 Treasury ETF Vanguard Total Stock 401(k) VTI $15,000 Market ETF BlackRock Equity 401(k) MADVX $15,000 Dividend Fund Johnson & Johnson RA JNJ $6,500 Pfizer IRA PFE $6,500 Southern New Hampshire University Asset Account Ticker Size ($) Bank of America IRA BAC $6,500 Walmart Trading/Brokerage WMT $3,000 CVS Health Trading/Brokerage CVS $4,000 Total $96,500 JUN 52,391 16 A FFE@& Chrome File Edit View History Bookmarks Profiles Tab Window Help Mie X | @ FN X 1 B Moc x | Dow = Sun Jun 16 1:18 PM D Mo x | RIcov x | EI22 x| nve x [ R Hon x | RIcou x| + FIN 450 Project Profiles.pdf 1. L[ (=] Kayla is a 29-year-old single female who just graduated from medical school and is starting her career as a doctor. Her annual salary is $150,000. She wants to pay off her $100,000 student loan debt (average debt rate 6%) quicker, so she reduced her cash savings. She contributes to her employer-provided 401(k) plan at a 6% contribution rate. The employer provides a match on the initial 6% contribution. She knows that the IRS 401(k) maximum contribution of $22,500 in 2023 is expected to rise to $23,000 in 2024. She understands that she is not taking full advantage of the 401(k) contribution tax deferral opportunity since her 6% contribution of $150,000 is roughly $9,000 annually. (For most individuals, every dollar invested in their 401(k) now means a dollar of income not taxed now and instead taxed later, preferably in retirement when personal taxes are generally lower than the rate in working years.) However, she has contributed to an IRA account annually for a few years, including $6,500 in 2023. She anticipates contributing the 2024 limit of $7,000. Kayla earns too much income to use the IRA contributions as tax deductions, but she does live in Floridaa state with no income taxes. Kayla's reasoning behind her decision to contribute to an IRA account instead of contributing the maximum possible annual contribution to her 401(k) is that her IRA account, which is provided by a national bank, allows her to invest in individual stocks, similar to a traditional brokerage account, while the 401(k) plan allows only for investments in mutual funds, exchange-traded funds, and diversified baskets of stocks and bonds. She also has a trading account with the same bank where she maintains the IRA account. All assets held in the three accounts are listed below. While she is generally conservative when it comes to making risky investments, she has a newfound understanding that growth requires taking risk, and that she can raise her risk profile because of her age and what is expected to be rapidly increasing income throughout her career. Now that she has a full-time job, she plans to increase her retirement savings while maintaining contributions to the IRA and investing in her trading account. She has tried to become more educated about the markets and understands that while prior return does not guarantee future performance, she would like to generate the same annual return as S&P 500 during the last 10 years. Because her expenses are modest, her student loans should be paid off in 10 years. She also hopes to open her own practice once her student loans are paid off and would like to build up enough assets, some in more liquid assets, to fund the start-up costs. Another reason for paying down debt and getting her finances in order is to improve her credit score, so she can access business debt funding for her future practice

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!