Question: econometrics question Asset 1 has expected return , with variance of (or standard deviation 61). Asset 2 has expected return , with variance oz .

econometrics question

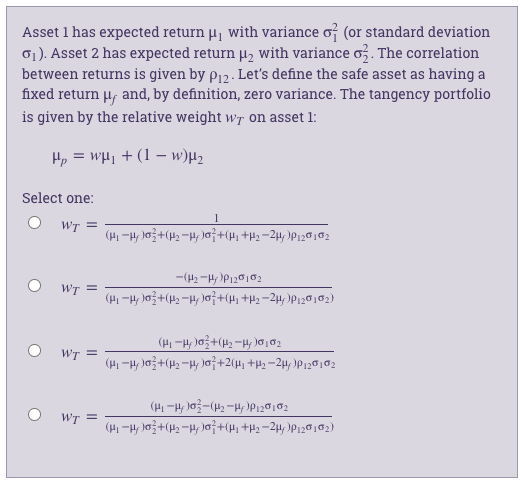

Asset 1 has expected return , with variance of (or standard deviation 61). Asset 2 has expected return , with variance oz . The correlation between returns is given by p12 . Let's define the safe asset as having a fixed return u and, by definition, zero variance. The tangency portfolio is given by the relative weight wy on asset 1: Hp = WHI+(1 -W)/2 Select one: WT = (HI - 1/ 103 + (12 - 1/10 7+(H] +12 -214/JP120102 O WT = -(H2 -Hy )P120102 (HI -1 103+(12 -1/ 107+(H, +12-24)P120102) O WT = (HI - H/ 103+ (H2 - H, )0102 O WT = (HI - 1 103-(12 -H/JP 120102

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock