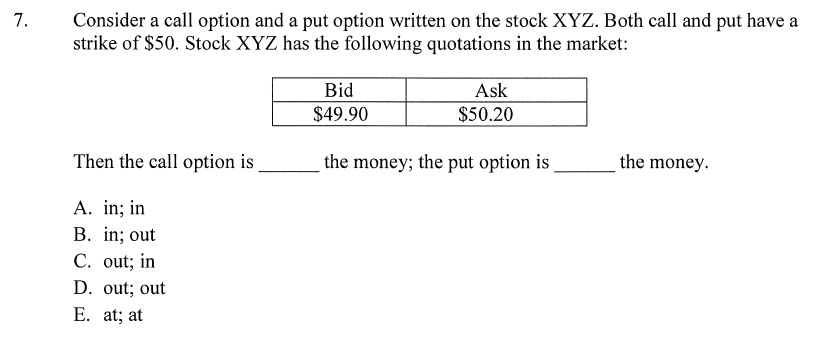

Question: Consider a call option and a put option written on the stock XYZ. Both call and put have a strike of $50. Stock XYZ has

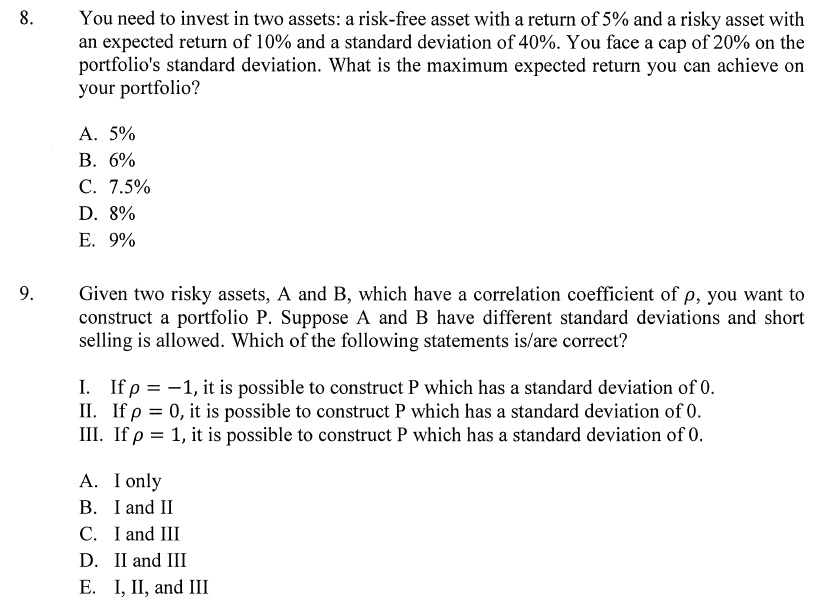

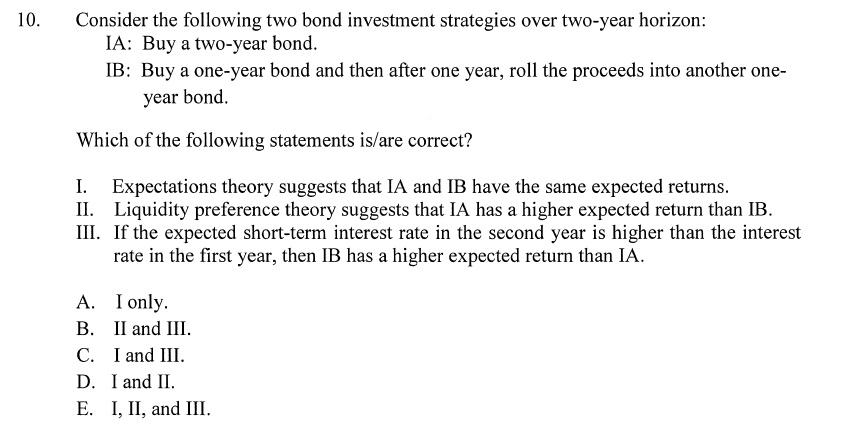

Consider a call option and a put option written on the stock XYZ. Both call and put have a strike of $50. Stock XYZ has the following quotations in the market: 7. Bid Ask $49.90 $50.20 the money Then the call option is the money; the put option is A. in; in B. in; out C. out; in D. out; out E. at; at 8 You need to invest in two assets: a risk-free asset with a return of 5% and a risky asset with an expected return of 10% and a standard deviation of 40%. You face a cap of 20% on the portfolio's standard deviation. What is the maximum expected return you can achieve on your portfolio? A. 5% . 6% C. 7.5% D. 8% . 9% 9. Given two risky assets, A and B, which have a correlation coefficient of p, you want to construct a portfolio P. Suppose A and B have different standard deviations and short selling is allowed. Which of the following statements is/are correct? I. If p -1, it is possible to construct P which has a standard deviation of 0 II. If p 0, it is possible to construct P which has a standard deviation of 0 III. If p 1, it is possible to construct P which has a standard deviation of 0. I only . I and II . C. I and III D. II and III E. I,II, and III Consider the following two bond investment strategies over two-year horizon IA: Buy a two-year bond IB: Buy a one-year bond and then after one year, roll the proceeds into another one- 10 year bond. Which of the following statements is/are correct? Expectations theory suggests that IA and IB have the same expected returns II. Liquidity preference theory suggests that IA has a higher expected return than IB III. If the expected short-term interest rate in the second year is higher than the interest rate in the first year, then IB has a higher expected return than IA I. A. I only B. II and III . I and III. D. I and II . I, I, and

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts