Question: EXCEL Note 1: Please use appropriate Cell referencing in Excel so that your numerical values update when you chan This will be helpful when you

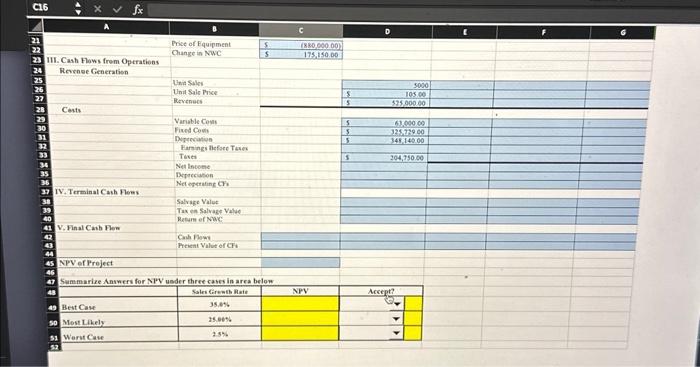

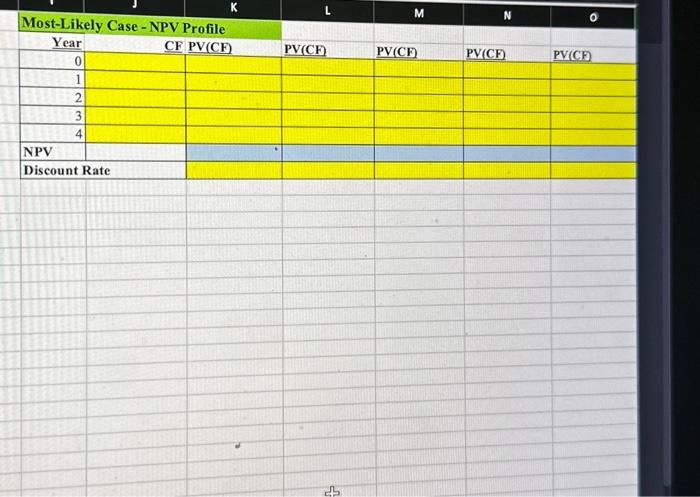

Note 1: Please use appropriate Cell referencing in Excel so that your numerical values update when you chan This will be helpful when you analyze the Best and Worst Case growth rate scenarios. Numerical Inputs expected from you are highlighted in yellow and Formula/Function Inputs are highlig Step 1: Read the Full Case. On the "CapitalBudget" Worksheet: Step 2: Calculate the weights of Equity and Weights of Debt for the firm. Use the stock and bond data provided in Step 3: Calculate the Cost of Equity for the firm. Use the CAPM and the Market data provided on on the Workshe Step 4: Calculate the Cost of Debt for the firm. Use the information provided about the firms bonds to calculate th Step 5: Calculate the after-tax cost of debt. Use the given tax rate for the firm. Step 6: Use the results from steps 2-5 to calculate the WACC (Weighted Average Cost of Capital) for the firm. Step 7: Input the appropriate Initial Cash Outlays IMPORTANT: All cash inflows need to be POSITIVE and all cash outflows need to be NEGATIVE. Step 8: Input the appropriate Cash flows from Operations Step 9: Input the appropriate Terminal Cash flows. Step 10: Compute the Net Cash flows for Years 04. Step 11: Compute the PV of Net Cash flows for Years 0 - 4. (You can either use the EXCEL formula for PVO or use Step 12: Compute the NPV of the Net cash flows - This can be done as the sum of the PV's in Step 11 or using Exce Note 2: Excel's NPV formula needs to be adjusted by a factor of (I+I)-Refer to the module 14 notes on CANV Step 13: Indicate the Accept/Reject decision for the most likely scenario. Note 3: Copy and paste the NPV values in cells C48 - C50 as you will need to input the NPV's for the 3 scenario Step 14: Compute the NPV for the Best Case scenario by changing to the Best Case growth rate in cell B11 and ind See Note I above - This is where it will be helpful. Step 15: Compute the NPV for the Worst Case scenario by changing to the Worst Case growth rate in cell B11 and On the "NPVProfile" Worksheet: Step 16: Complete the table to generate a NPV profile for the Most-Likely Scenario. The graph will be automaticall Note 4: A sample calculation for generating a NPV profile is shown on the NPVProfile worksheet Step 17: Optional - Complete the Worksheet "Answer Sheet" as needed. (see instructions on the sheet) Hint: Explain/Clarify any assumptions or methods used. Note: Use this sheet to convey any comments to the instructor. Step 18: Double check your work Step 19: Save with Solutions for Most Likely Case and Upload your final Excel project by the due date. EXTREMELY IMPORTANT: DO NOT add any rows or columns to the existing worksheets. You can ADD work that you may wish to conduct. Finallv. the inout Cells are configured to displax in a certain formah alease pavatteution to what is disulowedh The new Designer Eyewear was expected to sell for $105 per unit and had projected sales of 5000 units in the first year, with a projected (Most-Likely scenario) 25.0% growth rate per year for subsequent years. A total investment of $ 880,000 for new equipment was required. The equipment had fixed maintenance contracts of $325,729 per year with a salvage value of 176,860 and variable costs were 12% of revenues. Balky also needed to consider both the BestCase and Worst-Case scenarios in the analysis with growth rates of 35.00% and 2.50% respectively. The new equipment would be depreciated to zero using straight line depreciation. The new project required an increase in working capital of $175,150 and $22,770 of this increase would be offset with accounts payable. PSUWC currently has 917000 shares of stock outstanding at a current price of $78.00. Even though the company has outstanding stock, it is not publicly traded and therefore there is no publicly available financial information. However, after analysis management believes that its equity beta is 1.41 . The company also has 95000 bonds outstanding, with a current price of $900.00. The bonds pay interest semiannually at a coupon rate of 6.90%. The bonds have a par value of $1,000 and will mature in 12 years. The average corporate tax rate was 39%. Management believes the S\&P 500 is a reasonable proxy for the market portfolio. Therefore, the cost of equity is calculated using the company's equity beta and the market risk premium based on the S\&P 500 annual expected rate of retum - Balky would calculate the monthly expected market retum using 5 years of past monthly price data available in the worksheet Marketdata. This would then be multiplied by 12 to estimate the annual expected rate. Balky remembered that if the expected rate of retum for the market was too low, too high, or negative, a forward looking rate of an historical average of about 9.5% would have to be used, as the calculated value for the current 5 -year period may not be representative of the future. Balky would consider a E(Rm) between 812% acceptable. Balky would calculate the market risk premium: E(Rm) - R from the revious calculations using the risk-free rate data available in the worksheet Marketdata. Balky noted that the risk-free rate was on an annual basis. Balky needed to calculate the rate at which the project would have to be discounted to calculate the Net Present Value (NPV) of the proposed project based on the decision of raising capital and the current capital market environment. This discount rate, the WACC, would obviously influence the NPV and could affect the decision of whether to accept or reject the project. Thankfully, all the information needed to calculate this was available. Balky needed to clearly show all the calculations and sources for all parameter estimates used in the calculation of the WACC (and ultimately the NPV). 12x7 A B C D S\&P 500 Closing Data Company = 1.41 Date Adjusted Close Returns Risk Free Rate (Rf)= 4/1/2023 6275.870.56773% 3/1/2023 2/1/2023 12/1/2022 101/2022 \begin{tabular}{|l|l} \hline 6328.04 & 1.53966% \\ \hline 6230.61 & 0.30463% \\ \hline 6211.63 & 0.26627% \\ \hline 6228.17 & 0.38069% \\ \hline \end{tabular} 9/1/2022 8/1/2022 \begin{tabular}{ll} 6204.46 & 0.82054% \\ \hline 6153.55 & 3.45037% \end{tabular} 7/1/2022 \begin{tabular}{|l|l} 5941.23 & 2.28572% \\ \hline 5805.43 & 3.36685% \\ \hline 5609.97 & 0.36364% \end{tabular} 3/1/2022 2/1/2022 1/1/2022 12/1/2021 \begin{tabular}{|l|l|l} 11/1/2021 & 5222.79 & 1.45286% \\ \hline 10/1/2021 & 5146.91 & 1.73949% \\ \hline 911/2021 & 5057.38 & 0.78697% \end{tabular} \begin{tabular}{|l|l|l|} \hline 9/1/2021 & 5057.38 & 0.78697% \\ \hline 8/1/2021 & & 0.899 \\ \hline \end{tabular} 8/1/2021 \begin{tabular}{|l|l|l} \hline 711/2021 & 5061.93 & 0.27539% \\ \hline 6/1/2021 & 5075.87 & 1.43975% \\ \hline 5/12021 & 5002.79 & 0.90050% \\ \hline \end{tabular} \begin{tabular}{|l|l|l|} \hline 5/1/2021 & 5002.79 & 0.90050% \\ \hline 4/1/2021 & 4957.74 & 2.55177% \\ \hline 3/1/2021 & 4831.23 & 1.59959% \\ \hline 2/1/2021 & 4753.95 & 1.62349% \\ \hline 1/1/2021 & 4676.77 & 0.56813% \\ \hline 12//2020 & 4650.20 & 3.64414% \\ \hline 11/1/2020 & 4480.74 & 1.53457% \\ \hline 101/2020 & 4411.98 & 0.71782% \\ \hline/1/2020 & 4380.31 & 1.84371% \\ \hline 8/1/2020 & 4299.55 & 1.55993% \\ \hline 7/12020 & 4232.48 & 1.81170% \\ \hline 6/12020 & 4155.80 & 2.34467% \\ \hline 5/1/2020 & 4058.36 & 2.08015% \\ \hline \end{tabular} 1 0.Case Instructions A FullCase MarketData Q Grading Rubric Answer Sheet Ready Rx Accessibility: Investigate (Numerical Inputs Expected from you are highlighted in yellow and Formula/Function Inputs are highlighted in blue) Parameters Spreadoheet for determinisg Cath Vlows Cells G3s-G4e ceasain the terwisial cesh Gewh. 19 Timeline! 20 11. Net Investment Outlay = Isinial CF. \begin{tabular}{|l|l|ll|} \hline 21 & Fice of llawipment & 5 & (340,000(9) \\ \hline 22 & Change in NWC & 3 & 175,15060 \\ \hline \end{tabular} 111. Cash Flows frem Operations Revenue Gieneratien Una Sales: Unit Sale Price Revenues Costs Variable Cout Fard Cone Deprecietion Farningi Before Tants Depreciulion Net eperating CF: Note 1: Please use appropriate Cell referencing in Excel so that your numerical values update when you chan This will be helpful when you analyze the Best and Worst Case growth rate scenarios. Numerical Inputs expected from you are highlighted in yellow and Formula/Function Inputs are highlig Step 1: Read the Full Case. On the "CapitalBudget" Worksheet: Step 2: Calculate the weights of Equity and Weights of Debt for the firm. Use the stock and bond data provided in Step 3: Calculate the Cost of Equity for the firm. Use the CAPM and the Market data provided on on the Workshe Step 4: Calculate the Cost of Debt for the firm. Use the information provided about the firms bonds to calculate th Step 5: Calculate the after-tax cost of debt. Use the given tax rate for the firm. Step 6: Use the results from steps 2-5 to calculate the WACC (Weighted Average Cost of Capital) for the firm. Step 7: Input the appropriate Initial Cash Outlays IMPORTANT: All cash inflows need to be POSITIVE and all cash outflows need to be NEGATIVE. Step 8: Input the appropriate Cash flows from Operations Step 9: Input the appropriate Terminal Cash flows. Step 10: Compute the Net Cash flows for Years 04. Step 11: Compute the PV of Net Cash flows for Years 0 - 4. (You can either use the EXCEL formula for PVO or use Step 12: Compute the NPV of the Net cash flows - This can be done as the sum of the PV's in Step 11 or using Exce Note 2: Excel's NPV formula needs to be adjusted by a factor of (I+I)-Refer to the module 14 notes on CANV Step 13: Indicate the Accept/Reject decision for the most likely scenario. Note 3: Copy and paste the NPV values in cells C48 - C50 as you will need to input the NPV's for the 3 scenario Step 14: Compute the NPV for the Best Case scenario by changing to the Best Case growth rate in cell B11 and ind See Note I above - This is where it will be helpful. Step 15: Compute the NPV for the Worst Case scenario by changing to the Worst Case growth rate in cell B11 and On the "NPVProfile" Worksheet: Step 16: Complete the table to generate a NPV profile for the Most-Likely Scenario. The graph will be automaticall Note 4: A sample calculation for generating a NPV profile is shown on the NPVProfile worksheet Step 17: Optional - Complete the Worksheet "Answer Sheet" as needed. (see instructions on the sheet) Hint: Explain/Clarify any assumptions or methods used. Note: Use this sheet to convey any comments to the instructor. Step 18: Double check your work Step 19: Save with Solutions for Most Likely Case and Upload your final Excel project by the due date. EXTREMELY IMPORTANT: DO NOT add any rows or columns to the existing worksheets. You can ADD work that you may wish to conduct. Finallv. the inout Cells are configured to displax in a certain formah alease pavatteution to what is disulowedh The new Designer Eyewear was expected to sell for $105 per unit and had projected sales of 5000 units in the first year, with a projected (Most-Likely scenario) 25.0% growth rate per year for subsequent years. A total investment of $ 880,000 for new equipment was required. The equipment had fixed maintenance contracts of $325,729 per year with a salvage value of 176,860 and variable costs were 12% of revenues. Balky also needed to consider both the BestCase and Worst-Case scenarios in the analysis with growth rates of 35.00% and 2.50% respectively. The new equipment would be depreciated to zero using straight line depreciation. The new project required an increase in working capital of $175,150 and $22,770 of this increase would be offset with accounts payable. PSUWC currently has 917000 shares of stock outstanding at a current price of $78.00. Even though the company has outstanding stock, it is not publicly traded and therefore there is no publicly available financial information. However, after analysis management believes that its equity beta is 1.41 . The company also has 95000 bonds outstanding, with a current price of $900.00. The bonds pay interest semiannually at a coupon rate of 6.90%. The bonds have a par value of $1,000 and will mature in 12 years. The average corporate tax rate was 39%. Management believes the S\&P 500 is a reasonable proxy for the market portfolio. Therefore, the cost of equity is calculated using the company's equity beta and the market risk premium based on the S\&P 500 annual expected rate of retum - Balky would calculate the monthly expected market retum using 5 years of past monthly price data available in the worksheet Marketdata. This would then be multiplied by 12 to estimate the annual expected rate. Balky remembered that if the expected rate of retum for the market was too low, too high, or negative, a forward looking rate of an historical average of about 9.5% would have to be used, as the calculated value for the current 5 -year period may not be representative of the future. Balky would consider a E(Rm) between 812% acceptable. Balky would calculate the market risk premium: E(Rm) - R from the revious calculations using the risk-free rate data available in the worksheet Marketdata. Balky noted that the risk-free rate was on an annual basis. Balky needed to calculate the rate at which the project would have to be discounted to calculate the Net Present Value (NPV) of the proposed project based on the decision of raising capital and the current capital market environment. This discount rate, the WACC, would obviously influence the NPV and could affect the decision of whether to accept or reject the project. Thankfully, all the information needed to calculate this was available. Balky needed to clearly show all the calculations and sources for all parameter estimates used in the calculation of the WACC (and ultimately the NPV). 12x7 A B C D S\&P 500 Closing Data Company = 1.41 Date Adjusted Close Returns Risk Free Rate (Rf)= 4/1/2023 6275.870.56773% 3/1/2023 2/1/2023 12/1/2022 101/2022 \begin{tabular}{|l|l} \hline 6328.04 & 1.53966% \\ \hline 6230.61 & 0.30463% \\ \hline 6211.63 & 0.26627% \\ \hline 6228.17 & 0.38069% \\ \hline \end{tabular} 9/1/2022 8/1/2022 \begin{tabular}{ll} 6204.46 & 0.82054% \\ \hline 6153.55 & 3.45037% \end{tabular} 7/1/2022 \begin{tabular}{|l|l} 5941.23 & 2.28572% \\ \hline 5805.43 & 3.36685% \\ \hline 5609.97 & 0.36364% \end{tabular} 3/1/2022 2/1/2022 1/1/2022 12/1/2021 \begin{tabular}{|l|l|l} 11/1/2021 & 5222.79 & 1.45286% \\ \hline 10/1/2021 & 5146.91 & 1.73949% \\ \hline 911/2021 & 5057.38 & 0.78697% \end{tabular} \begin{tabular}{|l|l|l|} \hline 9/1/2021 & 5057.38 & 0.78697% \\ \hline 8/1/2021 & & 0.899 \\ \hline \end{tabular} 8/1/2021 \begin{tabular}{|l|l|l} \hline 711/2021 & 5061.93 & 0.27539% \\ \hline 6/1/2021 & 5075.87 & 1.43975% \\ \hline 5/12021 & 5002.79 & 0.90050% \\ \hline \end{tabular} \begin{tabular}{|l|l|l|} \hline 5/1/2021 & 5002.79 & 0.90050% \\ \hline 4/1/2021 & 4957.74 & 2.55177% \\ \hline 3/1/2021 & 4831.23 & 1.59959% \\ \hline 2/1/2021 & 4753.95 & 1.62349% \\ \hline 1/1/2021 & 4676.77 & 0.56813% \\ \hline 12//2020 & 4650.20 & 3.64414% \\ \hline 11/1/2020 & 4480.74 & 1.53457% \\ \hline 101/2020 & 4411.98 & 0.71782% \\ \hline/1/2020 & 4380.31 & 1.84371% \\ \hline 8/1/2020 & 4299.55 & 1.55993% \\ \hline 7/12020 & 4232.48 & 1.81170% \\ \hline 6/12020 & 4155.80 & 2.34467% \\ \hline 5/1/2020 & 4058.36 & 2.08015% \\ \hline \end{tabular} 1 0.Case Instructions A FullCase MarketData Q Grading Rubric Answer Sheet Ready Rx Accessibility: Investigate (Numerical Inputs Expected from you are highlighted in yellow and Formula/Function Inputs are highlighted in blue) Parameters Spreadoheet for determinisg Cath Vlows Cells G3s-G4e ceasain the terwisial cesh Gewh. 19 Timeline! 20 11. Net Investment Outlay = Isinial CF. \begin{tabular}{|l|l|ll|} \hline 21 & Fice of llawipment & 5 & (340,000(9) \\ \hline 22 & Change in NWC & 3 & 175,15060 \\ \hline \end{tabular} 111. Cash Flows frem Operations Revenue Gieneratien Una Sales: Unit Sale Price Revenues Costs Variable Cout Fard Cone Deprecietion Farningi Before Tants Depreciulion Net eperating CF

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts