Question: Exercise 1(15 points) We consider a two-period binomial tree to model interest rates. The time step dt is 1 year, We know that yo =

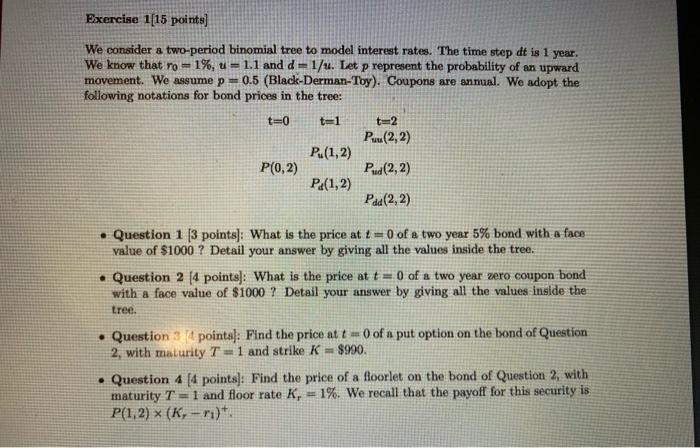

Exercise 1(15 points) We consider a two-period binomial tree to model interest rates. The time step dt is 1 year, We know that yo = 1%, u=1.1 and d = 1/4. Let p represent the probability of an upward movement. We assume p0.5 (Black-Derman-Toy). Coupons are anual. We adopt the following notations for bond prices in the tree: t=0 t=1 t=2 Pu(2, 2) P.(1,2) P(0,2) Pud(2, 2) PA(1,2) Pad(2, 2) Question 1 (3 points]: What is the price at t=0 of a two year 5% bond with a face value of $1000 ? Detail your answer by giving all the values inside the tree. Question 2 (4 points]: What is the price at t = 0 of a two year zero coupon bond with a face value of $1000 ? Detail your answer by giving all the values inside the tree. Question 3 points]: Find the price at t -0 of a put option on the bond of Question 2, with maturity T = 1 and strike K - $990. Question 4 [4 points]: Find the price of a floorlet on the bond of Question 2, with maturity T = 1 and floor rate K, -1%. We recall that the payoff for this security is P(1.2) x (K, -r)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts