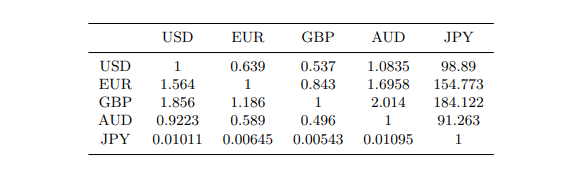

Question: Exercise 4 . 1 The Excel spreadsheet Exercise 4 . 1 FX model gives crosscurrency exchange rates among the currencies USD, EUR, GBP , AUD,

Exercise The Excel spreadsheet Exercise FX model gives crosscurrency exchange rates among the currencies USD, EUR, GBP AUD, and JPY

Use a linear programming model to detect if these exchange rates contain an

arbitrage opportunity. To do so use the following decision variables:

xij : amount of currency i converted to currency j

yk: net amount of currency k after all transactions.

Is there an arbitrage opportunity? If the answer is yes, then describe it for

example: Convert USD to EUR then to JPY then back to USD to net

USD without putting money in

tableUSD,EUR,GBPAUD,JPYUSDEURGBPAUDJPY

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock