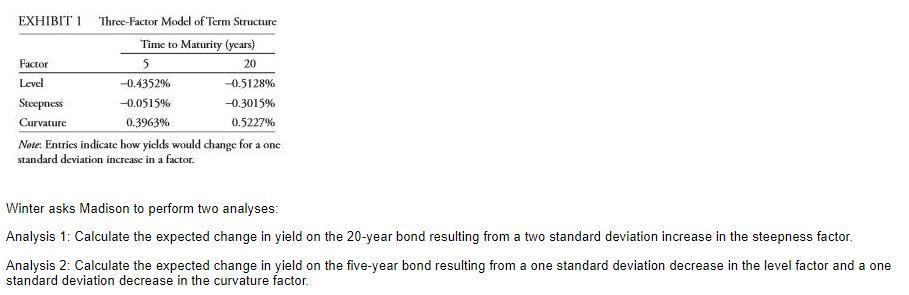

Question: EXHIBIT 1 Three-Factor Model of Term Structure Note: Entries indicate how yiclds would change for a one standard deviation increase in a factor. Winter asks

EXHIBIT 1 Three-Factor Model of Term Structure Note: Entries indicate how yiclds would change for a one standard deviation increase in a factor. Winter asks Madison to perform two analyses: Analysis 1: Calculate the expected change in yield on the 20-year bond resulting from a two standard deviation increase in the steepness factor. Analysis 2: Calculate the expected change in yield on the five-year bond resulting from a one standard deviation decrease in the level factor and a one standard deviation decrease in the curvature factor. EXHIBIT 1 Three-Factor Model of Term Structure Note: Entries indicate how yiclds would change for a one standard deviation increase in a factor. Winter asks Madison to perform two analyses: Analysis 1: Calculate the expected change in yield on the 20-year bond resulting from a two standard deviation increase in the steepness factor. Analysis 2: Calculate the expected change in yield on the five-year bond resulting from a one standard deviation decrease in the level factor and a one standard deviation decrease in the curvature factor

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts