Question: F. Fill in the above table for 52 weeks. ( t= 2501 for daily time change, use this information to compute t for week) Problem

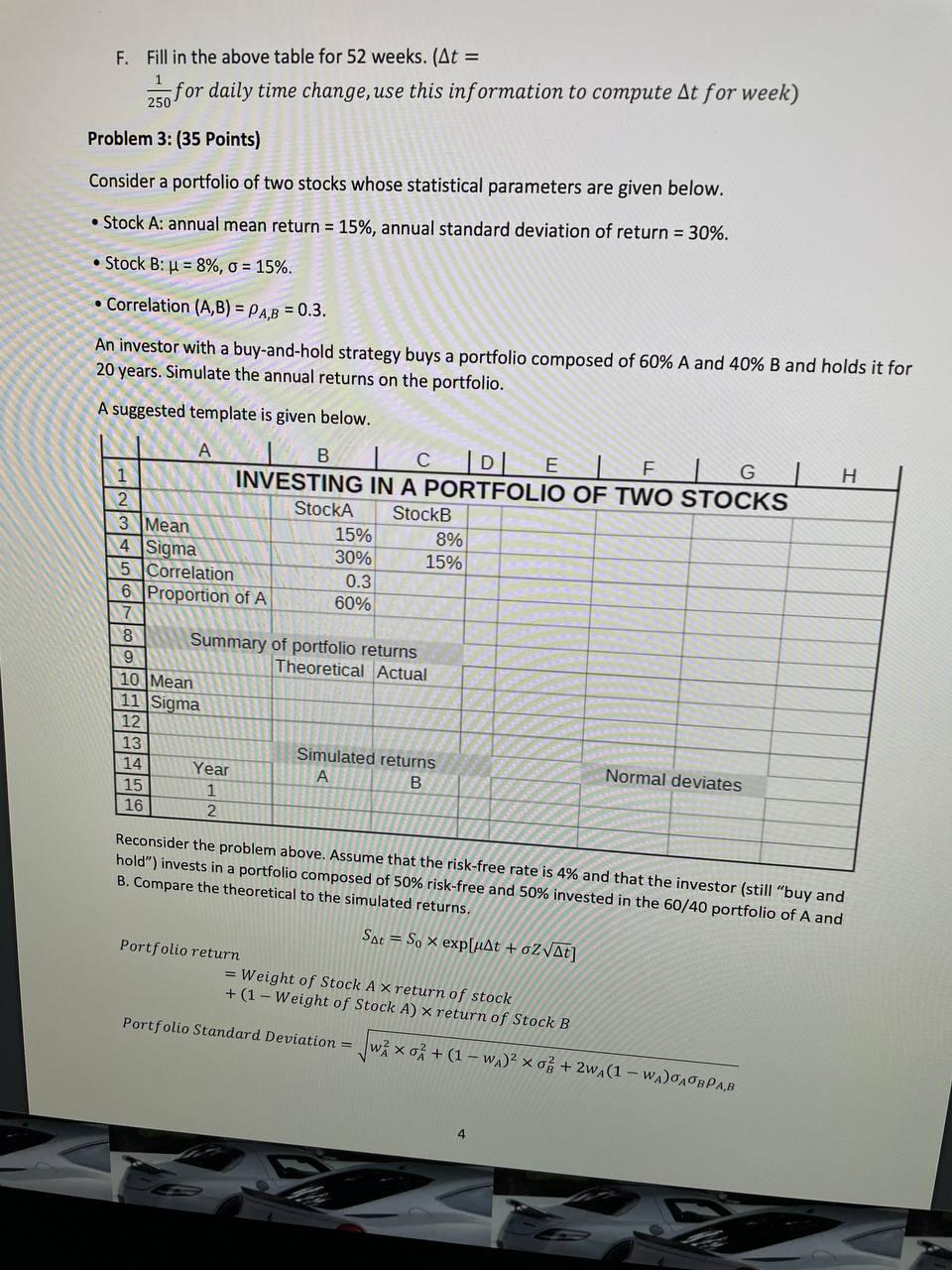

F. Fill in the above table for 52 weeks. ( t= 2501 for daily time change, use this information to compute t for week) Problem 3: (35 Points) Consider a portfolio of two stocks whose statistical parameters are given below. - Stock A: annual mean return =15%, annual standard deviation of return =30%. - Stock B: =8%,=15%. - Correlation (A,B)=A,B=0.3. An investor with a buy-and-hold strategy buys a portfolio composed of 60%A and 40% B and holds it for 20 years. Simulate the annual returns on the portfolio. A suggested template is given below. B. Compare the a portfolio composed of 50% risk-free and 50% is 4% and that the investor (still "buy and B. Compare the theoretical to the simulated returns. Portfolio return St=S0exp[t+Zt] = Weight of Stock A return of stock +(1 Weight of Stock A) return of Stock B Deviation =wA2A2+(1wA)2B2+2wA(1wA)ABA,B F. Fill in the above table for 52 weeks. ( t= 2501 for daily time change, use this information to compute t for week) Problem 3: (35 Points) Consider a portfolio of two stocks whose statistical parameters are given below. - Stock A: annual mean return =15%, annual standard deviation of return =30%. - Stock B: =8%,=15%. - Correlation (A,B)=A,B=0.3. An investor with a buy-and-hold strategy buys a portfolio composed of 60%A and 40% B and holds it for 20 years. Simulate the annual returns on the portfolio. A suggested template is given below. B. Compare the a portfolio composed of 50% risk-free and 50% is 4% and that the investor (still "buy and B. Compare the theoretical to the simulated returns. Portfolio return St=S0exp[t+Zt] = Weight of Stock A return of stock +(1 Weight of Stock A) return of Stock B Deviation =wA2A2+(1wA)2B2+2wA(1wA)ABA,B

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts