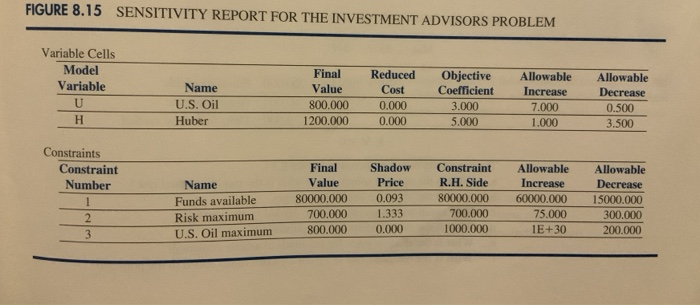

Question: FIGURE 8.15 SENSITIVITY REPORT FOR THE INVESTMENT ADVISORS PROBLEM Variable Cells Model Variable U H Name U.S. Oil Huber Final Value 800.000 1200.000 Reduced Cost

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock