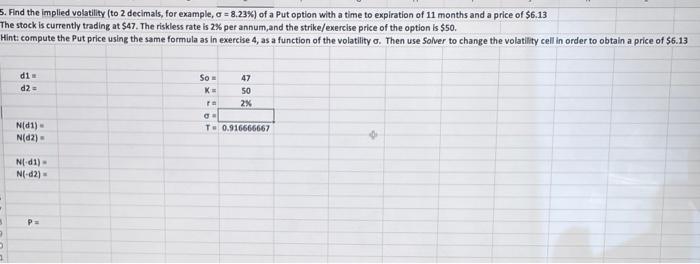

Question: Find the implied volatility (to 2 decimals, for example, =8.23% ) of a Put option with a time to expiration of 11 months and a

Find the implied volatility (to 2 decimals, for example, =8.23% ) of a Put option with a time to expiration of 11 months and a price of $6.13 he stock is currently trading at $47. The riskless rate is 2% per annum, and the strike/exercise price of the option is $50. inti compute the Put price using the same formula as in exercise 4 , as a function of the volatility . Then use Solver to change the volatility cell in order to obtain a price of 56.13 d1=d2=S0=K=4750

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock