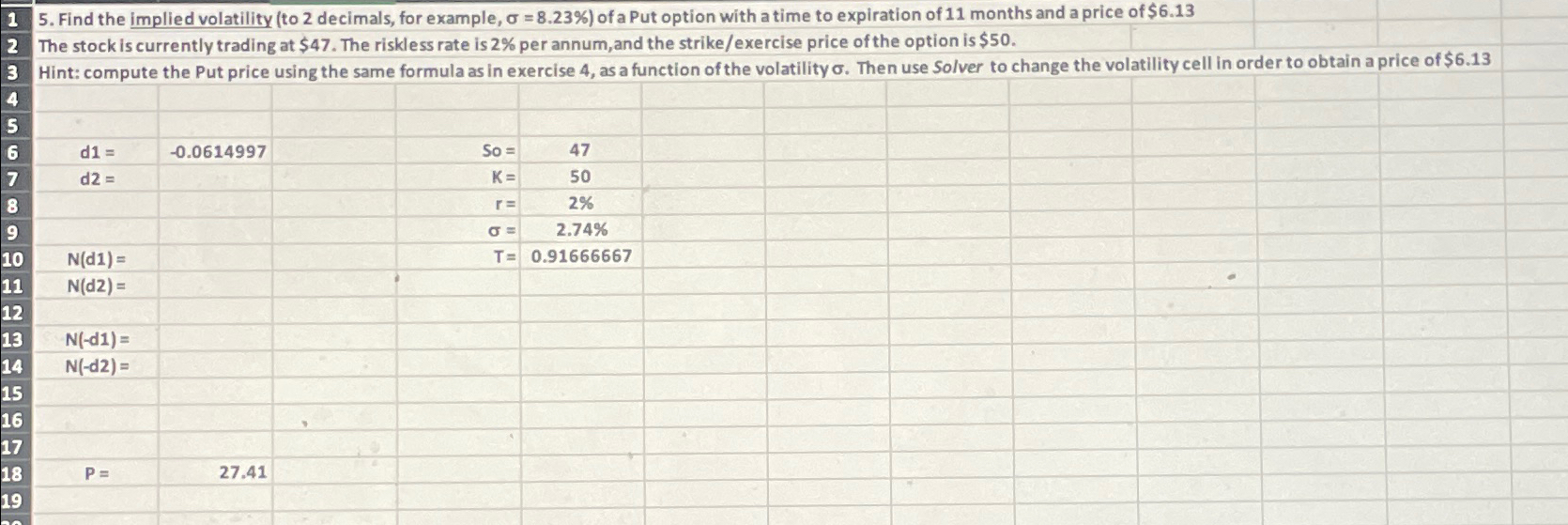

Question: 15. Find the implied volatility (to 2 decimals, for example, = 8.23%) of a Put option with a time to expiration of 11 months

15. Find the implied volatility (to 2 decimals, for example, = 8.23%) of a Put option with a time to expiration of 11 months and a price of $6.13 2 The stock is currently trading at $47. The riskless rate is 2% per annum, and the strike/exercise price of the option is $50. 3 Hint: compute the Put price using the same formula as in exercise 4, as a function of the volatility . Then use Solver to change the volatility cell in order to obtain a price of $6.13 4 5 6 d1 = -0.0614997 7 d2 = 8 9 10 N(d1)= 11 N(d2)= 12 13 N(-d1)= 14 N(-d2)= 15 16 17 18 P = 27.41 19 So= 47 K= 50 r = 2% = 2.74% T= 0.91666667

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts