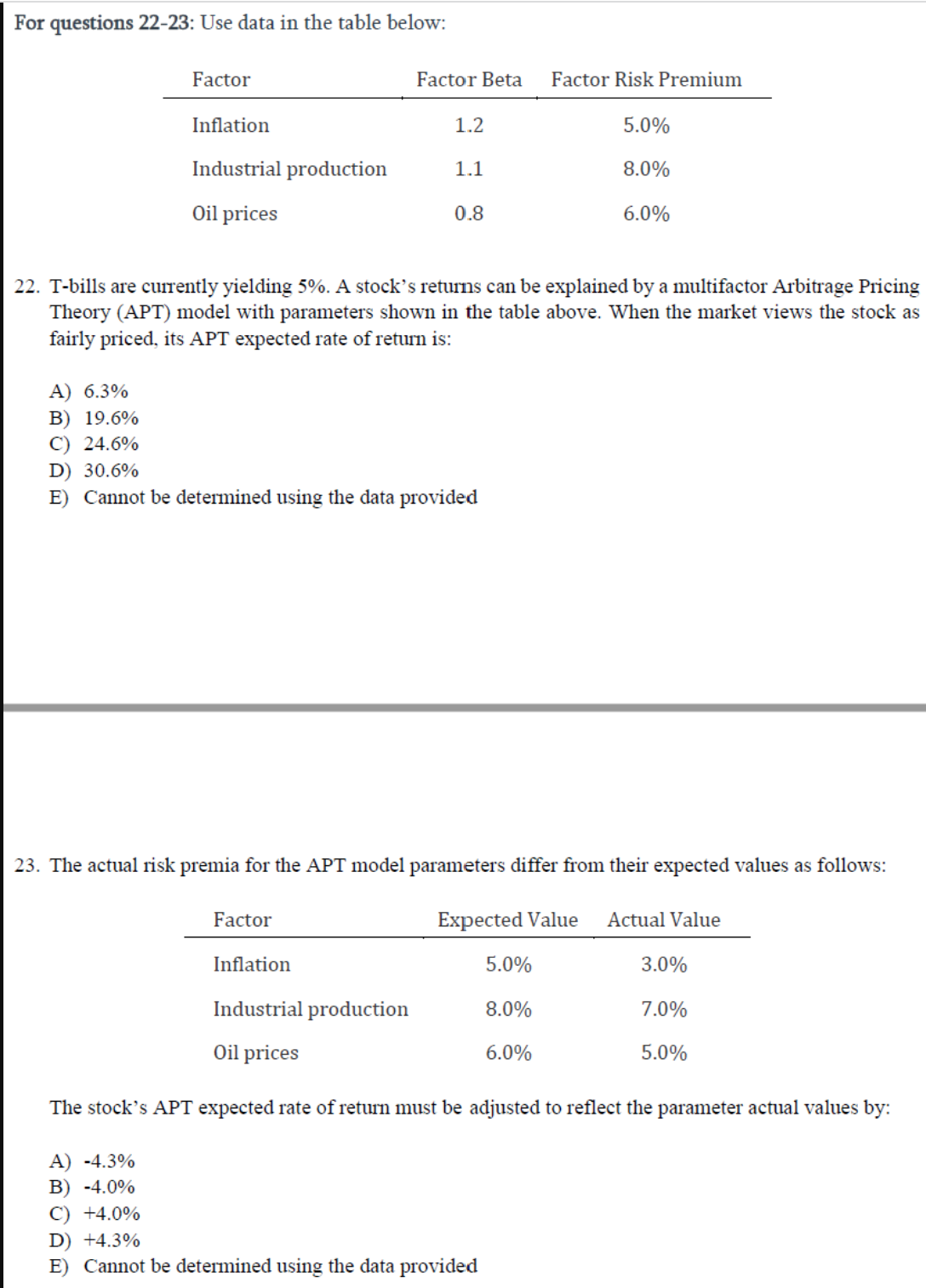

Question: For questions 22-23: Use data in the table below: Factor Factor Beta Factor Risk Premium Inflation 1.2 5.0% Industrial production 1.1 8.0% Oil prices 0.8

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts