Question: Formulate and solve the Markowitz portfolio optimization model to minimize portfolio variance subject to a required expected return of 10 percent that was defined

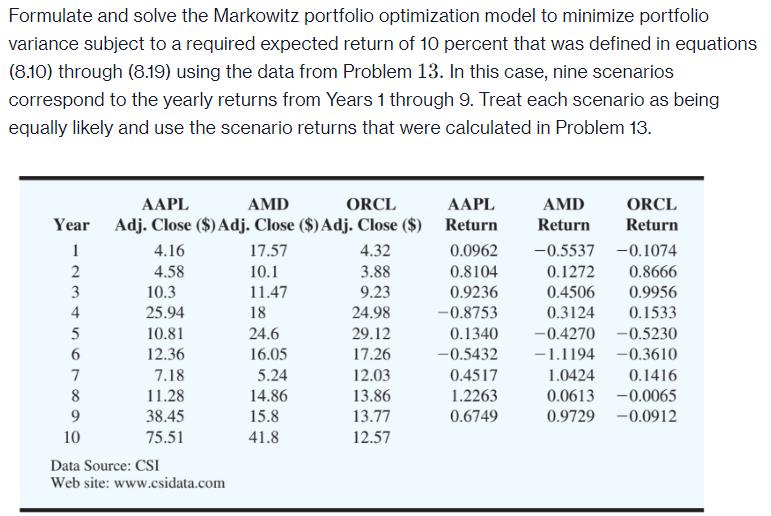

Formulate and solve the Markowitz portfolio optimization model to minimize portfolio variance subject to a required expected return of 10 percent that was defined in equations (8.10) through (8.19) using the data from Problem 13. In this case, nine scenarios correspond to the yearly returns from Years 1 through 9. Treat each scenario as being equally likely and use the scenario returns that were calculated in Problem 13. AAPL AMD ORCL Year Adj. Close ($) Adj. Close ($) Adj. Close ($) AAPL Return AMD ORCL Return Return 10 1234567899 4.16 17.57 4.32 0.0962 -0.5537 -0.1074 4.58 10.1 3.88 0.8104 0.1272 0.8666 10.3 11.47 9.23 0.9236 0.4506 0.9956 25.94 18 24.98 -0.8753 0.3124 0.1533 10.81 24.6 29.12 0.1340 -0.4270 -0.5230 12.36 16.05 17.26 -0.5432 -1.1194 -0.3610 7.18 5.24 12.03 0.4517 1.0424 0.1416 11.28 14.86 13.86 1.2263 0.0613 -0.0065 38.45 15.8 13.77 0.6749 0.9729 -0.0912 75.51 41.8 12.57 Data Source: CSI Web site: www.csidata.com

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts