Question: Problem 8-14 Formulate and solve the Markowitz portfolio optimization model to minimize portfolio variance subject to a required expected return of 10 percent that was

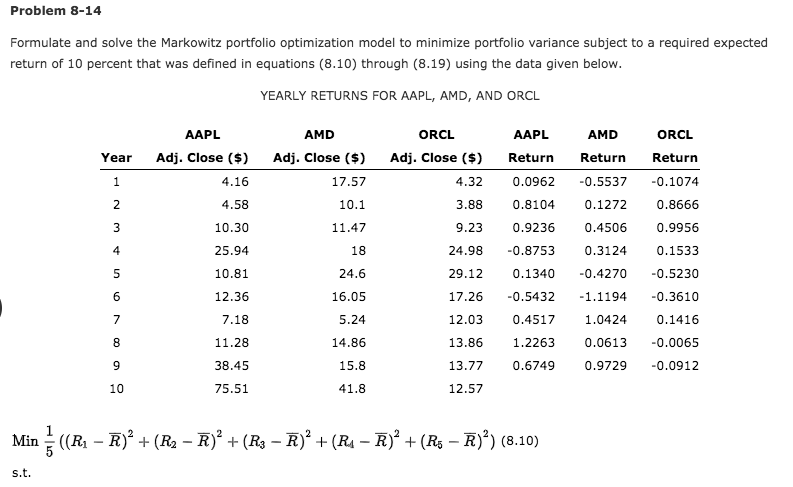

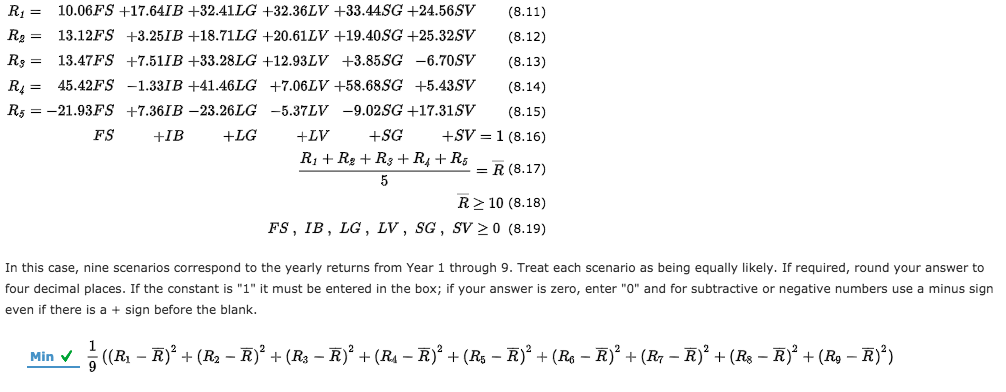

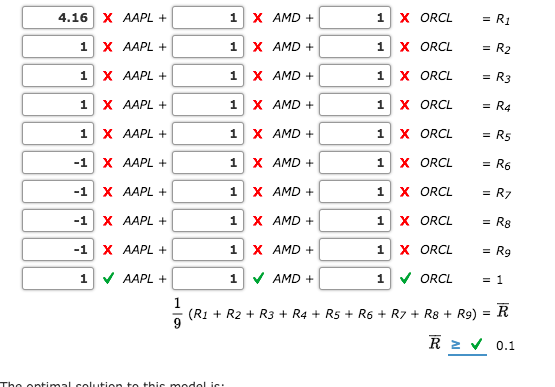

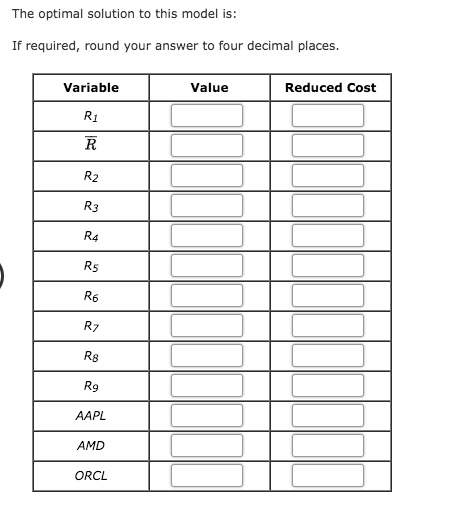

Problem 8-14 Formulate and solve the Markowitz portfolio optimization model to minimize portfolio variance subject to a required expected return of 10 percent that was defined in equations (8.10) through (8.19) using the data given below YEARLY RETURNS FOR AAPL, AMD, AND ORCL ORCL AAPL ORCL Year Adj. Close () Adj. Close ($) Adj. Close ($) Return Return Return 4.32 0.0962 0.5537 -0.1074 3.88 0.8104 0.12720.8666 9.23 0.9236 0.4506 0.9956 24.98 0.8753 0.3124 0.1533 29.12 0.1340 0.4270 0.5230 17.26 0.5432 1.1194 0.3610 12.03 0.4517 1.0424 0.1416 13.86 1.2263 0.0613 0.0065 13.77 0.6749 0.9729 0.0912 AAPL AMD AMD 4.16 4.58 10.30 25.94 10.81 12.36 7.18 11.28 38.45 75.51 17.57 10.1 11.47 18 24.6 16.05 5.24 14.86 15.8 41.8 2 4 8 10 12.57 R1-10.06FS +17.64IB +32.4LLG +32.36LV +33.44SG +24.56S (8.11) R13.12FS +3.25IB +18.71LG +20.61LV +19.40SG+25.32SV (8.12) R9-13.47FS +7.51IB +33.28LG +12.93LV +3.85SG -6.70SV (8.13) R'= 45.42FS -1.331B +41.461 G +7.06LV +58.68SG +5.43SV (8.14) R5--21.93FS +7.36IB -23.26LG -5.37LV-9.02SG +17.31SV (8.15) FS +IB +LG +LV +SG +SV = 1 (8.16) R 2 10 (8.18) FS, IB, LG, LV, SG, SV 2 0 (8.19) In this case, nine scenarios correspond to the yearly returns from Year 1 through 9. Treat each scenario as being equally likely. If required, round your answer to four decimal places. If the constant is "1" it must be entered in the box; if your answer is zero, enter "O" and for subtractive or negative numbers use a minus sign even if there is a sign before the blank. 4.16 X AAPL 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1 AMD 1 X ORCL = R2 1X AAPL+ 1X AAPL+ 1X AAPL+ 1X AAPL+ -1X AAPL+ -1X AAPL+ -1X AAPL+ -1X AAPL+ 1 X ORCL R6 (R1 + R2 + R3 + R4 R5 + R6 + R7 + R8 + R9) = Problem 8-14 Formulate and solve the Markowitz portfolio optimization model to minimize portfolio variance subject to a required expected return of 10 percent that was defined in equations (8.10) through (8.19) using the data given below YEARLY RETURNS FOR AAPL, AMD, AND ORCL ORCL AAPL ORCL Year Adj. Close () Adj. Close ($) Adj. Close ($) Return Return Return 4.32 0.0962 0.5537 -0.1074 3.88 0.8104 0.12720.8666 9.23 0.9236 0.4506 0.9956 24.98 0.8753 0.3124 0.1533 29.12 0.1340 0.4270 0.5230 17.26 0.5432 1.1194 0.3610 12.03 0.4517 1.0424 0.1416 13.86 1.2263 0.0613 0.0065 13.77 0.6749 0.9729 0.0912 AAPL AMD AMD 4.16 4.58 10.30 25.94 10.81 12.36 7.18 11.28 38.45 75.51 17.57 10.1 11.47 18 24.6 16.05 5.24 14.86 15.8 41.8 2 4 8 10 12.57 R1-10.06FS +17.64IB +32.4LLG +32.36LV +33.44SG +24.56S (8.11) R13.12FS +3.25IB +18.71LG +20.61LV +19.40SG+25.32SV (8.12) R9-13.47FS +7.51IB +33.28LG +12.93LV +3.85SG -6.70SV (8.13) R'= 45.42FS -1.331B +41.461 G +7.06LV +58.68SG +5.43SV (8.14) R5--21.93FS +7.36IB -23.26LG -5.37LV-9.02SG +17.31SV (8.15) FS +IB +LG +LV +SG +SV = 1 (8.16) R 2 10 (8.18) FS, IB, LG, LV, SG, SV 2 0 (8.19) In this case, nine scenarios correspond to the yearly returns from Year 1 through 9. Treat each scenario as being equally likely. If required, round your answer to four decimal places. If the constant is "1" it must be entered in the box; if your answer is zero, enter "O" and for subtractive or negative numbers use a minus sign even if there is a sign before the blank. 4.16 X AAPL 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1X AMD+ 1 AMD 1 X ORCL = R2 1X AAPL+ 1X AAPL+ 1X AAPL+ 1X AAPL+ -1X AAPL+ -1X AAPL+ -1X AAPL+ -1X AAPL+ 1 X ORCL R6 (R1 + R2 + R3 + R4 R5 + R6 + R7 + R8 + R9) =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts