GoMo Ltd is a UK registered company which commenced trading in the UK on 1 March...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

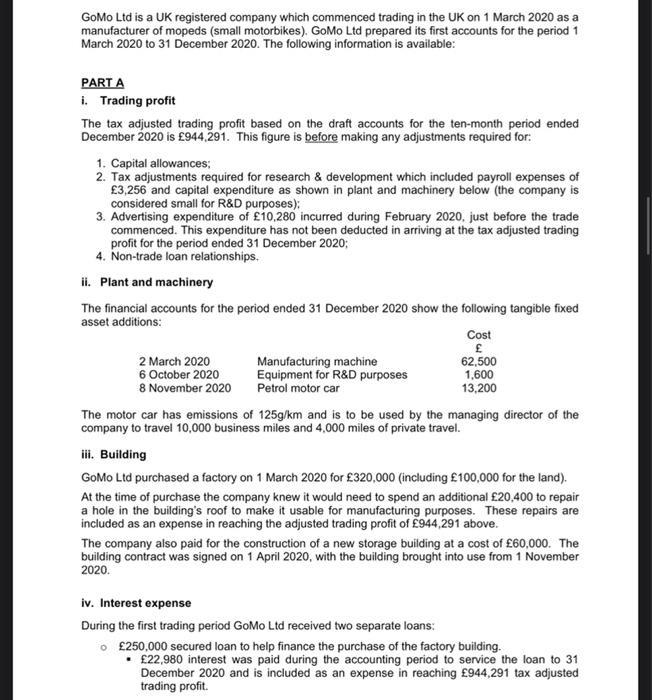

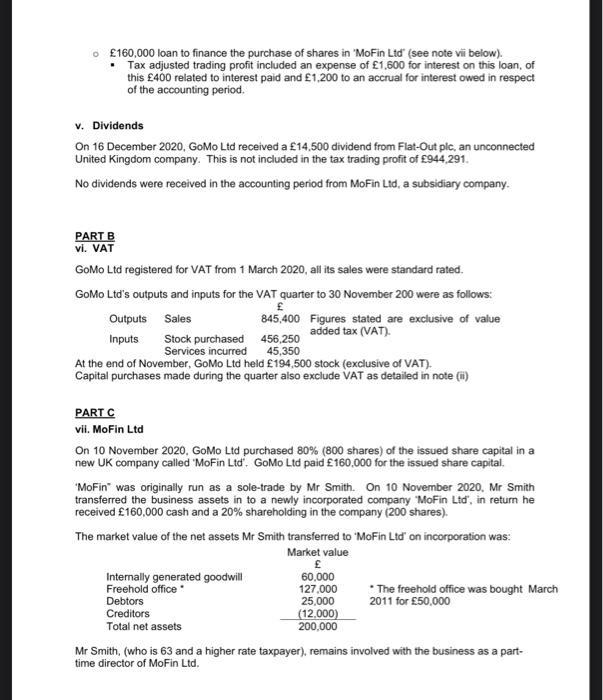

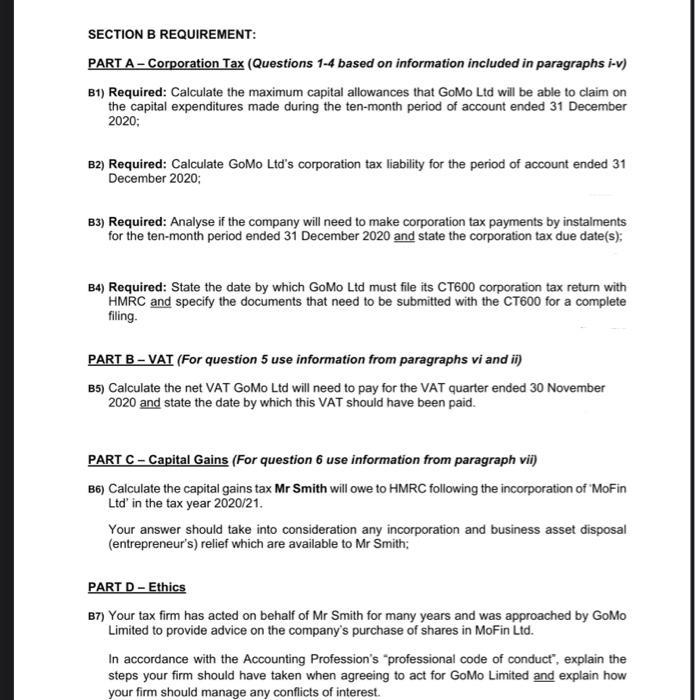

GoMo Ltd is a UK registered company which commenced trading in the UK on 1 March 2020 as a manufacturer of mopeds (small motorbikes). GoMo Ltd prepared its first accounts for the period 1 March 2020 to 31 December 2020. The following information is available: PART A i. Trading profit The tax adjusted trading profit based on the draft accounts for the ten-month period ended December 2020 is £944,291. This figure is before making any adjustments required for: 1. Capital allowances; 2. Tax adjustments required for research & development which included payroll expenses of £3,256 and capital expenditure as shown in plant and machinery below (the company is considered small for R&D purposes); 3. Advertising expenditure of £10,280 incurred during February 2020, just before the trade commenced. This expenditure has not been deducted in arriving at the tax adjusted trading profit for the period ended 31 December 2020; 4. Non-trade loan relationships. ii. Plant and machinery The financial accounts for the period ended 31 December 2020 show the following tangible fixed asset additions: 2 March 2020 6 October 2020 8 November 2020 Manufacturing machine Equipment for R&D purposes Petrol motor car Cost £ 62,500 1,600 13,200 The motor car has emissions of 125g/km and is to be used by the managing director of the company to travel 10,000 business miles and 4,000 miles of private travel. iii. Building GoMo Ltd purchased a factory on 1 March 2020 for £320,000 (including £100,000 for the land). At the time of purchase the company knew it would need to spend an additional £20,400 to repair a hole in the building's roof to make it usable for manufacturing purposes. These repairs are included as an expense in reaching the adjusted trading profit of £944,291 above. The company also paid for the construction of a new storage building at a cost of £60,000. The building contract was signed on 1 April 2020, with the building brought into use from 1 November 2020. iv. Interest expense During the first trading period GoMo Ltd received two separate loans: o £250,000 secured loan to help finance the purchase of the factory building. • £22,980 interest was paid during the accounting period to service the loan to 31 December 2020 and is included as an expense in reaching £944,291 tax adjusted trading profit. o £160,000 loan to finance the purchase of shares in 'MoFin Ltd' (see note vili below). • Tax adjusted trading profit included an expense of £1,600 for interest on this loan, of this £400 related to interest paid and £1,200 to an accrual for interest owed in respect of the accounting period. v. Dividends On 16 December 2020, GoMo Ltd received a £14,500 dividend from Flat-Out plc, an unconnected United Kingdom company. This is not included in the tax trading profit of £944,291. No dividends were received in the accounting period from MoFin Ltd, a subsidiary company. PART B vi. VAT GoMo Ltd registered for VAT from 1 March 2020, all its sales were standard rated. GoMo Ltd's outputs and inputs for the VAT quarter to 30 November 200 were as follows: £ 845,400 Figures stated are exclusive of value added tax (VAT). Stock purchased 456,250 Services incurred Outputs Sales Inputs 45,350 At the end of November, GoMo Ltd held £194,500 stock (exclusive of VAT). Capital purchases made during the quarter also exclude VAT as detailed in note (ii) PART C vii. MoFin Ltd On 10 November 2020, GoMo Ltd purchased 80% (800 shares) of the issued share capital in a new UK company called 'MoFin Ltd". GoMo Ltd paid £160,000 for the issued share capital. MoFin" was originally run as a sole-trade by Mr Smith. On 10 November 2020, Mr Smith transferred the business assets in to a newly incorporated company "MoFin Ltd, in return he received £160,000 cash and a 20% shareholding in the company (200 shares). The market value of the net assets Mr Smith transferred to "MoFin Ltd" on incorporation was: Market value £ 60,000 127,000 25,000 (12,000) 200,000 Internally generated goodwill Freehold office Debtors Creditors Total net assets *The freehold office was bought March 2011 for £50,000 Mr Smith, (who is 63 and a higher rate taxpayer), remains involved with the business as a part- time director of MoFin Ltd. SECTION B REQUIREMENT: PART A - Corporation Tax (Questions 1-4 based on information included in paragraphs i-v) B1) Required: Calculate the maximum capital allowances that GoMo Ltd will be able to claim on the capital expenditures made during the ten-month period of account ended 31 December 2020; B2) Required: Calculate GoMo Ltd's corporation tax liability for the period of account ended 31 December 2020; B3) Required: Analyse if the company will need to make corporation tax payments by instalments for the ten-month period ended 31 December 2020 and state the corporation tax due date(s); B4) Required: State the date by which GoMo Ltd must file its CT600 corporation tax return with HMRC and specify the documents that need to be submitted with the CT600 for a complete filing. PART B-VAT (For question 5 use information from paragraphs vi and ii) B5) Calculate the net VAT GoMo Ltd will need to pay for the VAT quarter ended 30 November 2020 and state the date by which this VAT should have been paid. PART C - Capital Gains (For question 6 use information from paragraph vii) B6) Calculate the capital gains tax Mr Smith will owe to HMRC following the incorporation of 'MoFin Ltd' in the tax year 2020/21. Your answer should take into consideration any incorporation and business asset disposal (entrepreneur's) relief which are available to Mr Smith; PART D- Ethics B7) Your tax firm has acted on behalf of Mr Smith for many years and was approached by GoMo Limited to provide advice on the company's purchase of shares in MoFin Ltd. In accordance with the Accounting Profession's "professional code of conduct", explain the steps your firm should have taken when agreeing to act for GoMo Limited and explain how your firm should manage any conflicts of interest. GoMo Ltd is a UK registered company which commenced trading in the UK on 1 March 2020 as a manufacturer of mopeds (small motorbikes). GoMo Ltd prepared its first accounts for the period 1 March 2020 to 31 December 2020. The following information is available: PART A i. Trading profit The tax adjusted trading profit based on the draft accounts for the ten-month period ended December 2020 is £944,291. This figure is before making any adjustments required for: 1. Capital allowances; 2. Tax adjustments required for research & development which included payroll expenses of £3,256 and capital expenditure as shown in plant and machinery below (the company is considered small for R&D purposes); 3. Advertising expenditure of £10,280 incurred during February 2020, just before the trade commenced. This expenditure has not been deducted in arriving at the tax adjusted trading profit for the period ended 31 December 2020; 4. Non-trade loan relationships. ii. Plant and machinery The financial accounts for the period ended 31 December 2020 show the following tangible fixed asset additions: 2 March 2020 6 October 2020 8 November 2020 Manufacturing machine Equipment for R&D purposes Petrol motor car Cost £ 62,500 1,600 13,200 The motor car has emissions of 125g/km and is to be used by the managing director of the company to travel 10,000 business miles and 4,000 miles of private travel. iii. Building GoMo Ltd purchased a factory on 1 March 2020 for £320,000 (including £100,000 for the land). At the time of purchase the company knew it would need to spend an additional £20,400 to repair a hole in the building's roof to make it usable for manufacturing purposes. These repairs are included as an expense in reaching the adjusted trading profit of £944,291 above. The company also paid for the construction of a new storage building at a cost of £60,000. The building contract was signed on 1 April 2020, with the building brought into use from 1 November 2020. iv. Interest expense During the first trading period GoMo Ltd received two separate loans: o £250,000 secured loan to help finance the purchase of the factory building. • £22,980 interest was paid during the accounting period to service the loan to 31 December 2020 and is included as an expense in reaching £944,291 tax adjusted trading profit. o £160,000 loan to finance the purchase of shares in 'MoFin Ltd' (see note vili below). • Tax adjusted trading profit included an expense of £1,600 for interest on this loan, of this £400 related to interest paid and £1,200 to an accrual for interest owed in respect of the accounting period. v. Dividends On 16 December 2020, GoMo Ltd received a £14,500 dividend from Flat-Out plc, an unconnected United Kingdom company. This is not included in the tax trading profit of £944,291. No dividends were received in the accounting period from MoFin Ltd, a subsidiary company. PART B vi. VAT GoMo Ltd registered for VAT from 1 March 2020, all its sales were standard rated. GoMo Ltd's outputs and inputs for the VAT quarter to 30 November 200 were as follows: £ 845,400 Figures stated are exclusive of value added tax (VAT). Stock purchased 456,250 Services incurred Outputs Sales Inputs 45,350 At the end of November, GoMo Ltd held £194,500 stock (exclusive of VAT). Capital purchases made during the quarter also exclude VAT as detailed in note (ii) PART C vii. MoFin Ltd On 10 November 2020, GoMo Ltd purchased 80% (800 shares) of the issued share capital in a new UK company called 'MoFin Ltd". GoMo Ltd paid £160,000 for the issued share capital. MoFin" was originally run as a sole-trade by Mr Smith. On 10 November 2020, Mr Smith transferred the business assets in to a newly incorporated company "MoFin Ltd, in return he received £160,000 cash and a 20% shareholding in the company (200 shares). The market value of the net assets Mr Smith transferred to "MoFin Ltd" on incorporation was: Market value £ 60,000 127,000 25,000 (12,000) 200,000 Internally generated goodwill Freehold office Debtors Creditors Total net assets *The freehold office was bought March 2011 for £50,000 Mr Smith, (who is 63 and a higher rate taxpayer), remains involved with the business as a part- time director of MoFin Ltd. SECTION B REQUIREMENT: PART A - Corporation Tax (Questions 1-4 based on information included in paragraphs i-v) B1) Required: Calculate the maximum capital allowances that GoMo Ltd will be able to claim on the capital expenditures made during the ten-month period of account ended 31 December 2020; B2) Required: Calculate GoMo Ltd's corporation tax liability for the period of account ended 31 December 2020; B3) Required: Analyse if the company will need to make corporation tax payments by instalments for the ten-month period ended 31 December 2020 and state the corporation tax due date(s); B4) Required: State the date by which GoMo Ltd must file its CT600 corporation tax return with HMRC and specify the documents that need to be submitted with the CT600 for a complete filing. PART B-VAT (For question 5 use information from paragraphs vi and ii) B5) Calculate the net VAT GoMo Ltd will need to pay for the VAT quarter ended 30 November 2020 and state the date by which this VAT should have been paid. PART C - Capital Gains (For question 6 use information from paragraph vii) B6) Calculate the capital gains tax Mr Smith will owe to HMRC following the incorporation of 'MoFin Ltd' in the tax year 2020/21. Your answer should take into consideration any incorporation and business asset disposal (entrepreneur's) relief which are available to Mr Smith; PART D- Ethics B7) Your tax firm has acted on behalf of Mr Smith for many years and was approached by GoMo Limited to provide advice on the company's purchase of shares in MoFin Ltd. In accordance with the Accounting Profession's "professional code of conduct", explain the steps your firm should have taken when agreeing to act for GoMo Limited and explain how your firm should manage any conflicts of interest.

Expert Answer:

Answer rating: 100% (QA)

PART A i The maximum capital allowances that GoMo Lid will be able to claim on the capital expenditures made during the tenmonth period of account end... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-0273744443

14th Edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these accounting questions

-

Blackhawks plc is a UK registered company that provides services to the financial services industry. The company has been trading for many years and prepares financial statements to 31 March....

-

Answer ALL questions. FunkyClothing Ltd are a UK registered company who design and produce sustainable clothing for the fashion market. Their clothing sells both online and in high-street retail...

-

On 1 March 2020 Holmes Ltd enters into a binding agreement with a New Zealand company, which requires the New Zealand Company to construct an item of machinery for Holmes Ltd. The cost of the...

-

The unadjusted trial balance of Mesa Inc., at the company's year end of December 31 follows: Additional information and adjustment data: 1. The 12-month insurance policy was purchased and was...

-

Explain how a manager might make a trade-off between the direct materials price and the direct materials quantity variances.

-

Yvonne Sanchez borrowed money from MBank to purchase an automobile. She gave MBank a security interest in the vehicle as collateral to secure the loan. When Sanchez defaulted on the loan, MBank hired...

-

Using the software development life cycle approach, do we apply project management principles to software development? Elaborate on your answer.

-

At the end of July, Tony took a complete inventory of his supplies and found the following: 5 dozen 14 screws at a cost of $8 a dozen 2 dozen 12 screws at a cost of $5 a dozen 2 cartons of computer...

-

The Application Appointment ( A simple calculator and notepad is helpful for this activity. ) You are a loan originator, and you have a new couple, Pat and Kris as customers who would like to apply...

-

Whats the difference between a real resource and a virtual resource?

-

Calculate the pH of a 0.40M ammonia solution? Show how the concentrations of the pertinent species change. (Kb=1.85x10^-5)

-

Working individually, in pairs, or in small groups, as your instructor directs, a. Look at five of the example student rsums on VisualCV. com. What features do you like? Why? What features would you...

-

Joe has worked for Blanque Cheque Construction (BCC) for five years, mainly in administrative positions. Three months ago, he was informed that he was being transferred to the firms project...

-

TMP Human Resource Consulting had the following contribution margin income statement for the year ended 2019. Required Answer each of the following independent situations. (a) Explain how an...

-

Wagons and Wheels Ltd is a farm machinery dealership. In recent years, the company has experienced unsatisfactory profit results because of declining sales in the area. At the suggestion of the...

-

Draw Franciss supply curve as shown in the chapter and indicate the following: a. The producer surplus when the price is $40 per haircut, shaded with horizontal stripes. b. The increase in producer...

-

A private healthcare center in Saudi Arabia has current assets of SAR 150,000 and total assets of SAR 390,000. This center has current liabilities of SAR 100,000 and total liabilities of SAR 240,000....

-

What are the main distinctions between the different schools of legal interpretation?

-

Gamma plc had an issued share capital at 1 April 20X0 of: 200,000 made up of 20p shares. 50,000 1 convertible preference shares receiving a dividend of 2.50 per share: These shares were...

-

The move from the preparation of accounts under UK GAAP to the users of IFRS by United Kingdom quoted companies for years beginning 1 January 2005 had an effect on the level of profits reported. How...

-

Rouge plc acquired 100% of the common shares of Noir plc on 1 January 20X0 and gained control. At that date the statements of financial position of the two companies were as follows: Required:...

-

Following up on question number 3, assume the school conducts a manifestation determination meeting. Tim attends the meeting with his parents. At the meeting, Tim tells the team that smoking helps...

-

Which is an advantage to an employee who participates in a profit-sharing plan? A. Employee does not have to make investment decisions. B. Graded vesting schedule. C. Older employees receive the...

-

Which of the following is not a characteristic of a defined benefit plan? A. A guaranteed retirement benefit. B. Risk of preretirement inflation assumed by employer. C. Benefits based upon the...

Study smarter with the SolutionInn App