Question: Hello i know this is a long question but i would appreciate any help i can get on this 1. (4 points each) Consider the

Hello i know this is a long question but i would appreciate any help i can get on this

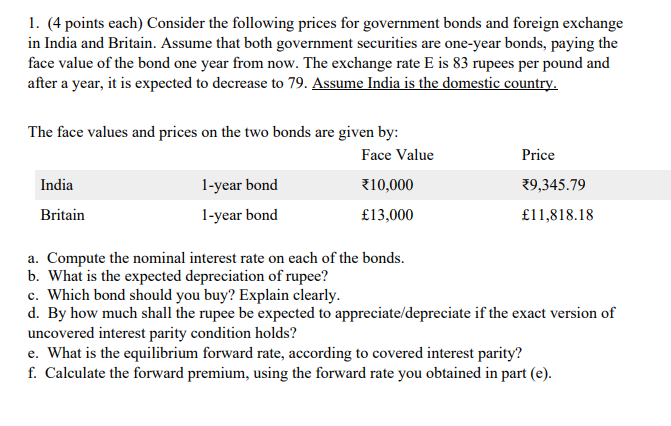

1. (4 points each) Consider the following prices for government bonds and foreign exchange in India and Britain. Assume that both government securities are one-year bonds, paying the face value of the bond one year from now. The exchange rate E is 83 rupees per pound and after a year, it is expected to decrease to 79. Assume India is the domestic country. The face values and prices on the two bonds are given by: Face Value Price India 1-year bond 10,000 39,345.79 Britain 1-year bond $13,000 f11,818.18 a. Compute the nominal interest rate on each of the bonds. b. What is the expected depreciation of rupee? c. Which bond should you buy? Explain clearly. d. By how much shall the rupee be expected to appreciate/depreciate if the exact version of uncovered interest parity condition holds? e. What is the equilibrium forward rate, according to covered interest parity? f. Calculate the forward premium, using the forward rate you obtained in part (e)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts