On 1 August 2016 Pataya purchased 18 million of a total of 24 million equity shares in

Question:

On 1 August 2016 Pataya purchased 18 million of a total of 24 million equity shares in Santa. The acquisition was through a share exchange of two shares in Pataya for every three shares in Santa. Both companies have shares with a par value of Rs1 each. The market price of Pataya’s shares at 1 August 2016 was Rs 5·75 per share. Pataya will also pay in cash on 31 July 2018 (two years after acquisition) Rs 2·42 per acquired share of Santa. Ignore cost of capital. The reserves of Santa on 1 April 2016 were Rs 69 million.

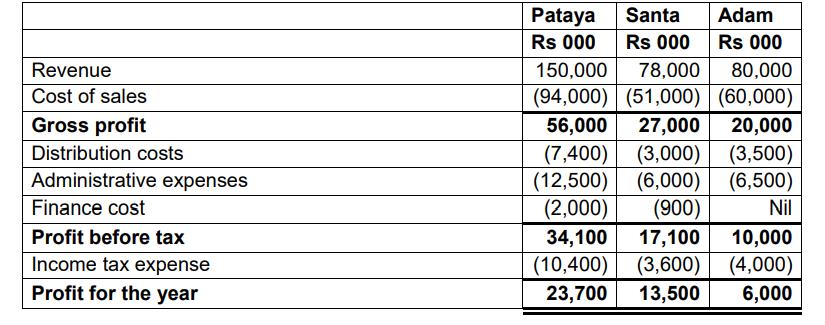

Pataya has held an investment of 30% of the equity shares in Adam for many years. The summarised income statements for the three companies for the year ended 31 March 2017 are:

The following information is relevant:

(i) The fair values of the net assets of Santa at the date of acquisition were equal to their carrying amounts with the exception of property and plant. Property and plant had fair values of Rs 4·1 million and Rs 2·4 million respectively in excess of their carrying amounts. The increase in the fair value of the property would create additional depreciation of Rs 200,000 in the consolidated financial statements in the post acquisition period to 31 March 2017 and the plant had a remaining life of four years (straight-line depreciation) at the date of acquisition of Santa. All depreciation is treated as part of cost of sales.

The fair values have not been reflected in Santa’s financial statements. No fair value adjustments were required on the acquisition of Adam.

ii) The fair value of non controlling interest is estimated to be Rs 2.5 million.

(iii) Prior to its acquisition, Santa had been a good customer of Pataya. In the year to 31 March 2017, Pataya sold goods at a selling price of Rs 1·25 million per month to Santa both before and after its acquisition. Pataya made a profit of 20% on the cost of these sales. At 31 March 2017 Santa still held inventory of Rs 3 million (at cost to Santa) of goods purchased in the post acquisition period from Pataya.

(iv) An impairment test on the goodwill of Santa conducted on 31 March 2017 concluded that it should be written down by Rs 2 million. The value of the investment in Adam was not impaired.

(v) All items in the above income statements are deemed to accrue evenly over the year.

(vi) Ignore deferred tax.

Required:

(a) Calculate the goodwill arising on the acquisition of Santa at 1 August 2016 and its value as at 31 March 2017. [12 marks]

(b) Prepare the consolidated income statement for the Papaya Group for the year ended 31 March 2017.

Expert Answer:

a The goodwill arising on the acquisition of Santa at 1 August 2016 would be calculated as follows P... View the full answer

Statistics for Business and Economics

ISBN: 978-0132930192

8th edition

Authors: Paul Newbold, William Carlson, Betty Thorne