Question: Hello, please help me with this question, thank you!! QUESTION 3 (CONTEMPORARY ISSUES IN FMS AND FUND MANAGEMET) b) The following information on the performance

Hello, please help me with this question, thank you!!

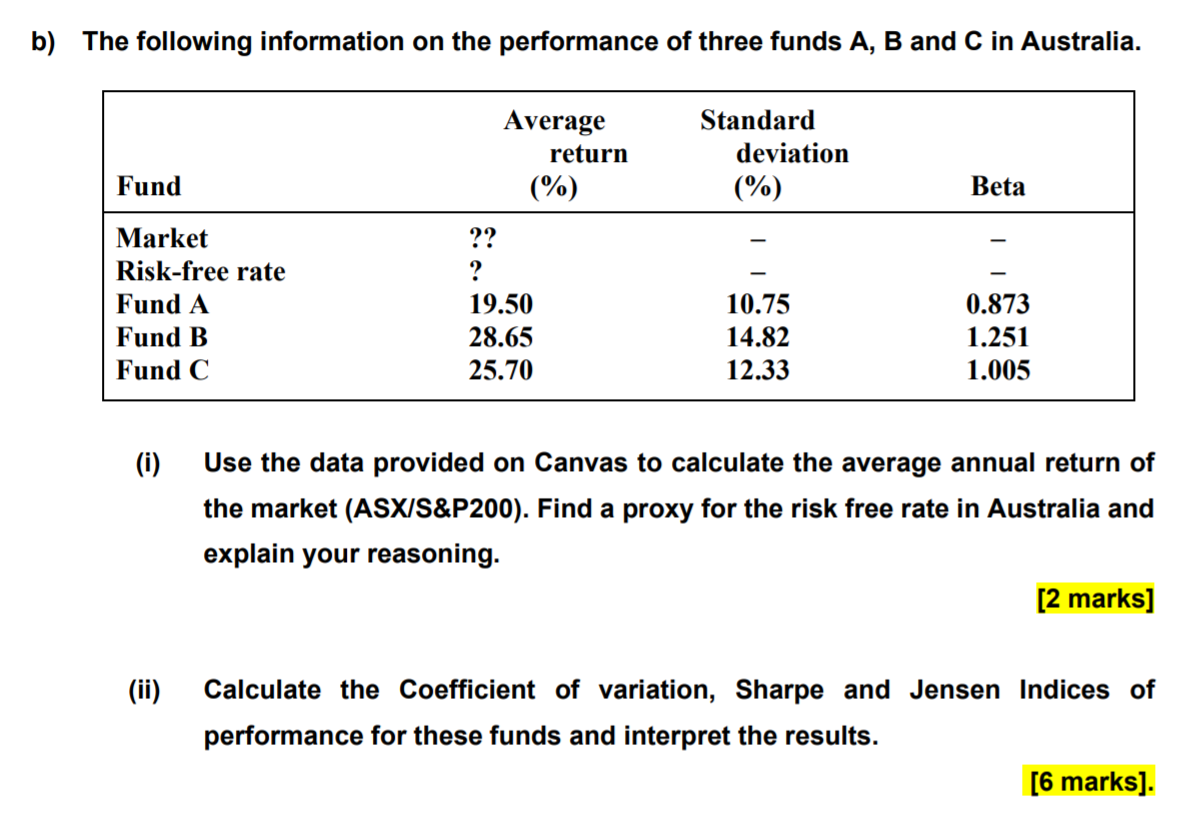

QUESTION 3 (CONTEMPORARY ISSUES IN FMS AND FUND MANAGEMET) b) The following information on the performance of three funds A, B and C in Australia. Average return (%) Standard deviation (%) Fund Beta Market Risk-free rate Fund A Fund B Fund C ?? ? 19.50 28.65 25.70 10.75 14.82 12.33 0.873 1.251 1.005 (i) Use the data provided on Canvas calculate the average annual return of the market (ASXIS&P200). Find a proxy for the risk free rate in Australia and explain your reasoning. [2 marks] (ii) Calculate the coefficient of variation, Sharpe and Jensen Indices of performance for these funds and interpret the results. [6 marks]. QUESTION 3 (CONTEMPORARY ISSUES IN FMS AND FUND MANAGEMET) b) The following information on the performance of three funds A, B and C in Australia. Average return (%) Standard deviation (%) Fund Beta Market Risk-free rate Fund A Fund B Fund C ?? ? 19.50 28.65 25.70 10.75 14.82 12.33 0.873 1.251 1.005 (i) Use the data provided on Canvas calculate the average annual return of the market (ASXIS&P200). Find a proxy for the risk free rate in Australia and explain your reasoning. [2 marks] (ii) Calculate the coefficient of variation, Sharpe and Jensen Indices of performance for these funds and interpret the results. [6 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts