Question: help with qestion Homework Help - Q&A from x | eCampus Home * | Z Content * connect * @ Home - Canva * |

help with qestion

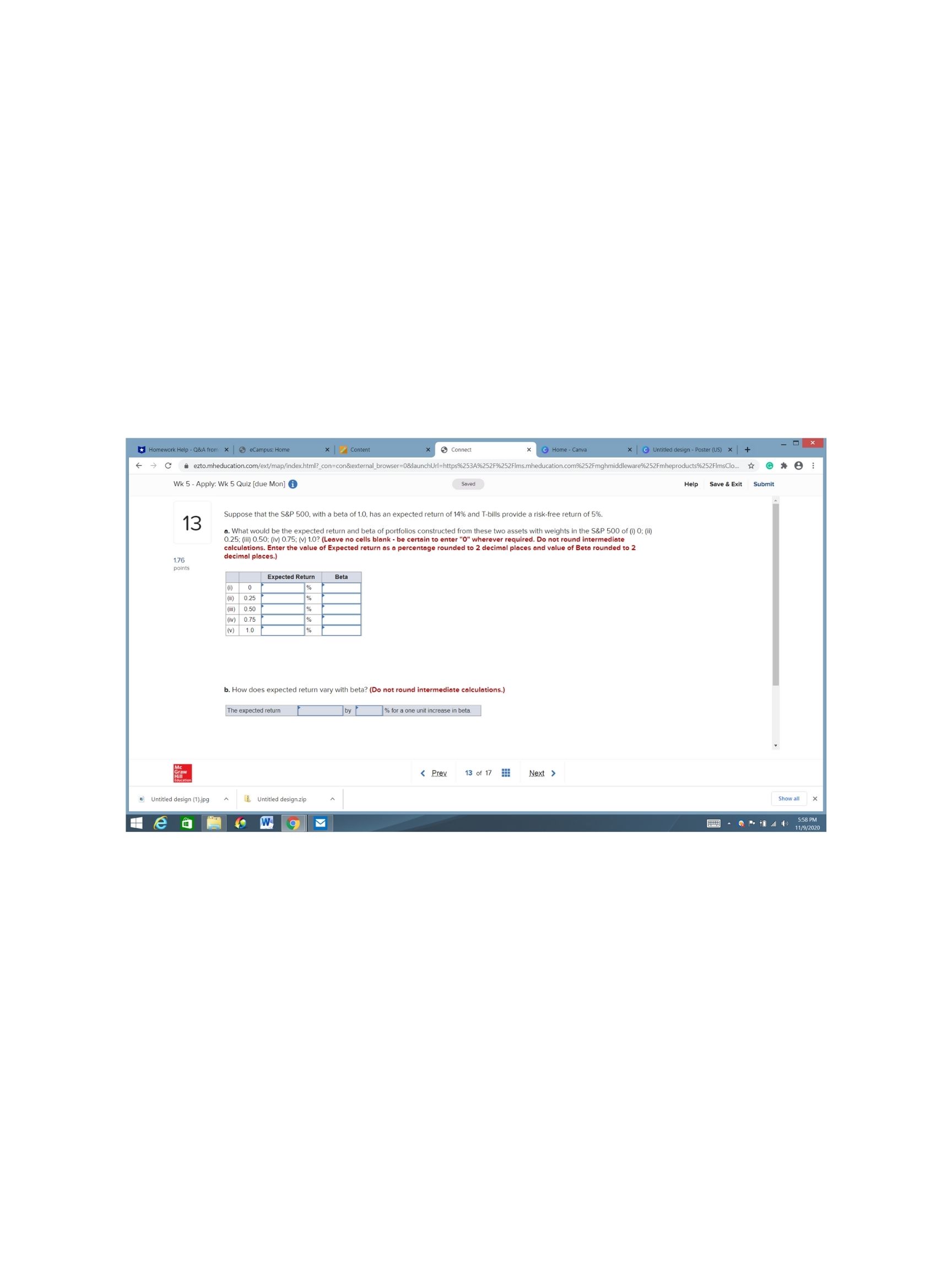

Homework Help - Q&A from x | eCampus Home * | Z Content * connect * @ Home - Canva * | @ Untitled design - Poster (US) * | + 1 X * ezto.mheducation.com/ext/map/index.html?_con=con&external_browser=0&launchUrl=https%253A%252F6252Fims.mheducation.com%252Fmghmiddleware%252Fmheproducts6252FimsClo.. # @ # : Wk 5 - Apply: Wk 5 Quiz [due Mon] Saved Help Save & Exit Submit 13 Suppose that the S&P 500, with a beta of 1.0, has an expected return of 14% and T-bills provide a risk-free return of 5%. a. What would be the expected return and beta of portfolios constructed from these two assets with weights in the S&P 500 of (1) 0: (i1) 0.25; (11) 0.50; (iv) 0.75; (v) 1.0? (Leave no cells blank - b enter "0" wherever required. Do not round intermed decimal places.) calculations. Enter the value of Expected return as a percentage rounded to 2 decimal places and value of Beta rounded to 2 1.76 points Expected Return Beta (IV ) 0.75 (V ) 10 b. How does expected return vary with beta? (Do not round intermediate calculations.) The expected return by % for a one unit increase in beta.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts