Question: Here is an example problem with solutions and explanations, please solve the problem that does not have answers: Example problem and answers: Example problem explanations:

Here is an example problem with solutions and explanations, please solve the problem that does not have answers:

Example problem and answers:

Example problem explanations:

Example problem explanations:

Please solve this problem:

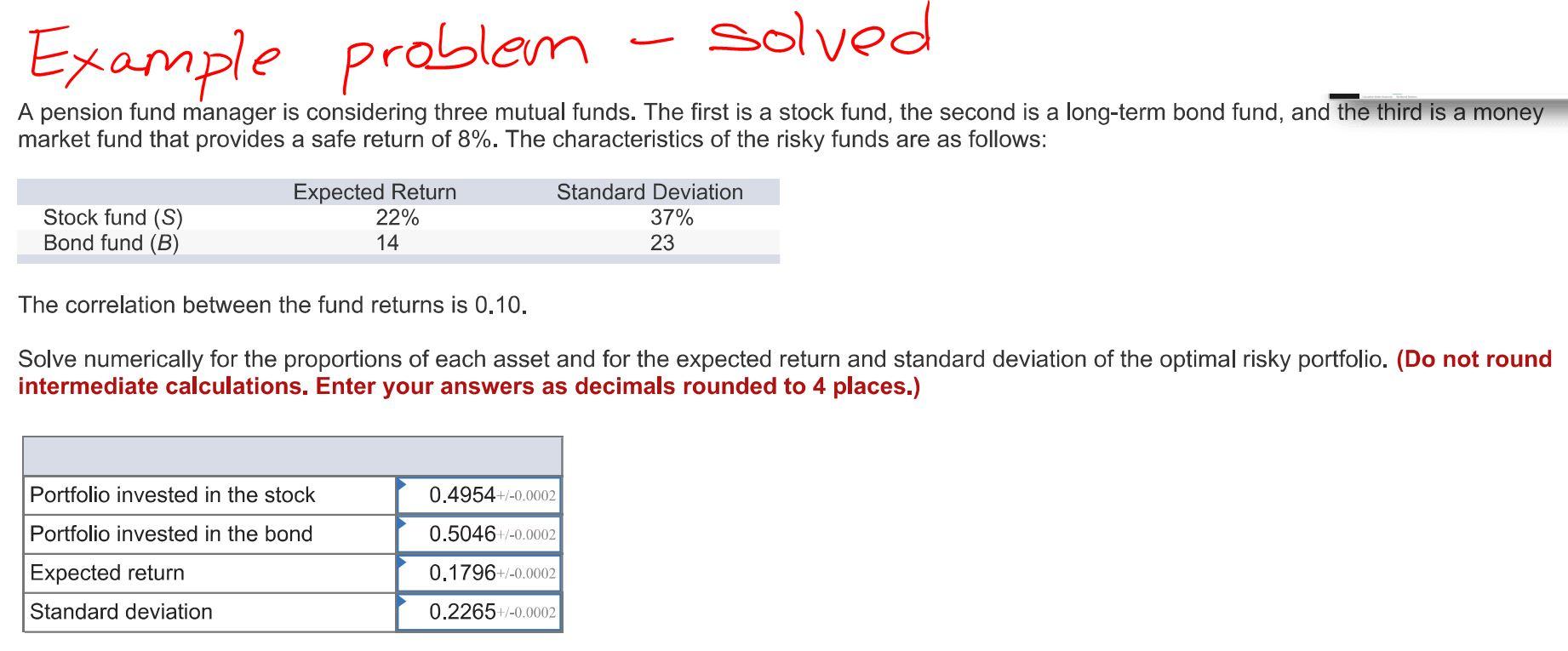

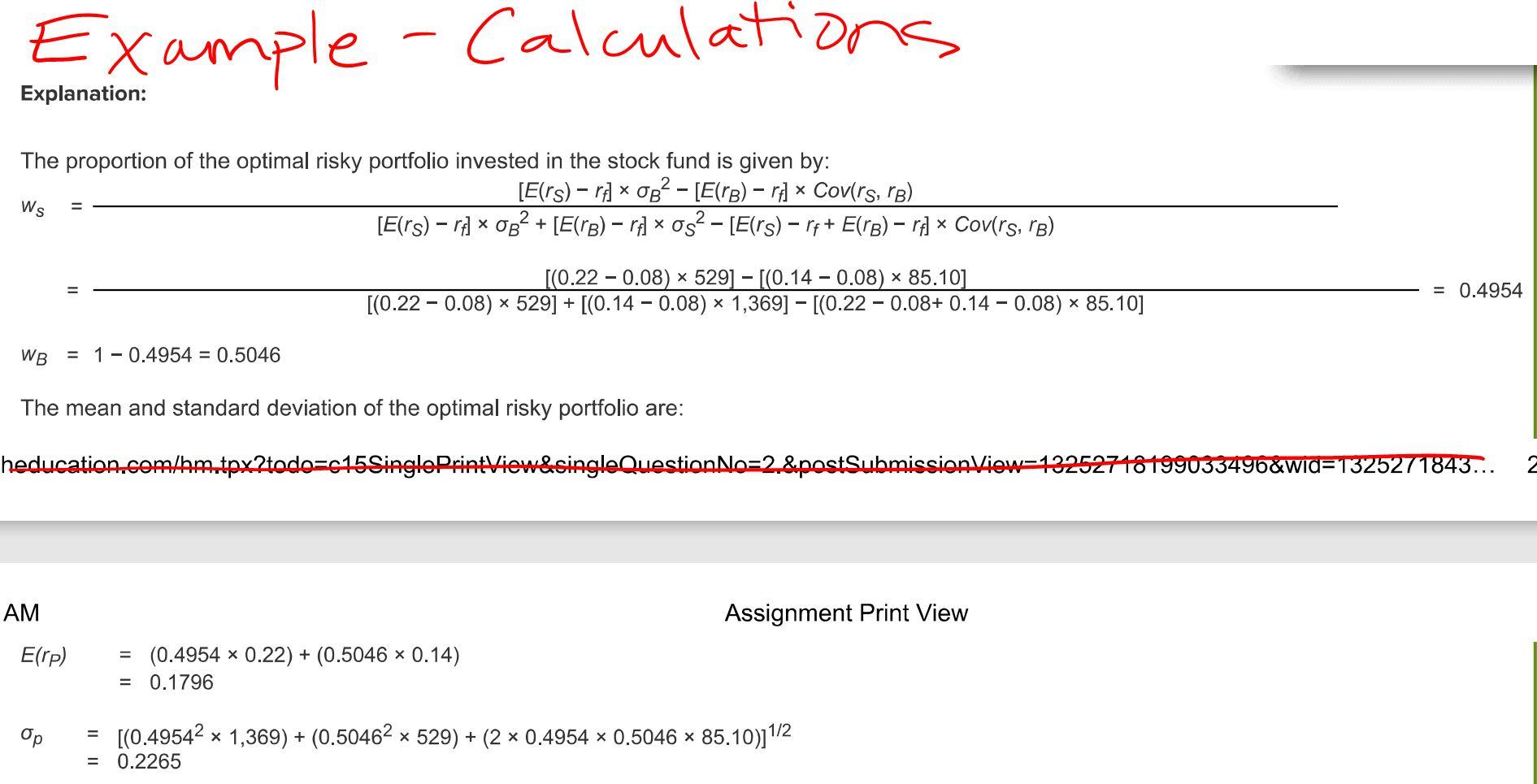

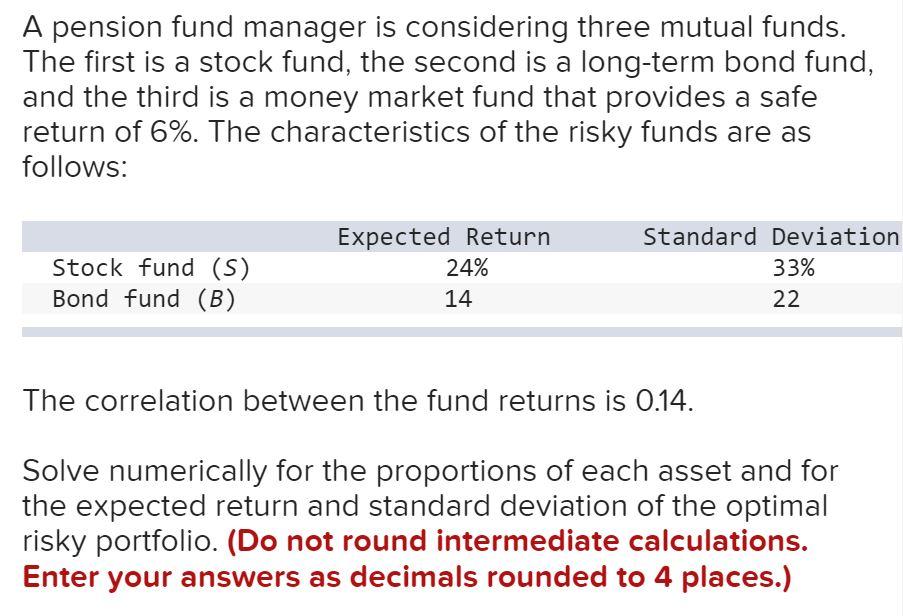

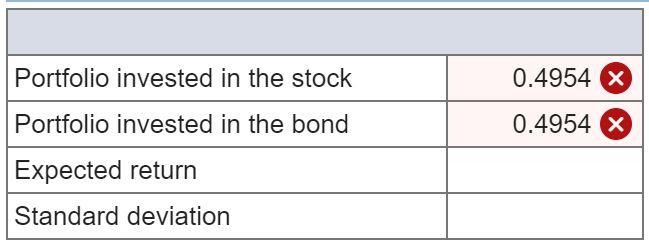

Example problem solved A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term bond fund, and the third is a money market fund that provides a safe return of 8%. The characteristics of the risky funds are as follows: Stock fund (S) Bond fund (B) Expected Return 22% 14 Standard Deviation 37% 23 The correlation between the fund returns is 0.10. Solve numerically for the proportions of each asset and for the expected return and standard deviation of the optimal risky portfolio. (Do not round intermediate calculations. Enter your answers as decimals rounded to 4 places.) Portfolio invested in the stock 0.4954+/-0.0002 Portfolio invested in the bond 0.5046 -0.0002 Expected return 0.1796+/-0.0002 Standard deviation 0.2265+/-0.0002 Example -Calculations Explanation: The proportion of the optimal risky portfolio invested in the stock fund is given by: [E(rs) rp] * 082 [E(nb) rf] Covirs, rB) Ws [E(rs) rf] * 082 + [E(Tb) ri] * og2 - [E(rs) Pf+ E(lb) rA] * Covers, rb) X - [(0.22 - 0.08) * 529] [(0.14 - 0.08) ~ 85.10] [(0.22 - 0.08) * 529] + [(0.14 - 0.08) * 1,369] [(0.22 - 0.08+ 0.14 - 0.08) * 85.10] = 0.4954 WB = 1 -0.4954 = 0.5046 The mean and standard deviation of the optimal risky portfolio are: heducation.com/am.tpx?todo=c15SinglePrintView&single QuestionNo=2.&.postSubmission View=13252718199033496&wid=1325271843... a AM Assignment Print View E(rp) = (0.4954 * 0.22) + (0.5046 * 0.14) = 0.1796 Op = + [(0.49542 x 1,369) + (0.50462 x 529) + (2 * 0.4954 * 0.5046 85.10)]1/2 = 0.2265 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term bond fund, and the third is a money market fund that provides a safe return of 6%. The characteristics of the risky funds are as follows: Stock fund (S) Bond fund (B) Expected Return 24% 14 Standard Deviation 33% 22 The correlation between the fund returns is 0.14. Solve numerically for the proportions of each asset and for the expected return and standard deviation of the optimal risky portfolio. (Do not round intermediate calculations. Enter your answers as decimals rounded to 4 places.) Portfolio invested in the stock 0.4954 x 0.4954 x Portfolio invested in the bond Expected return Standard deviation

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts