Hiram Life (Hiram), a large multinational insurer located in Canada, has received permission to increase its...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

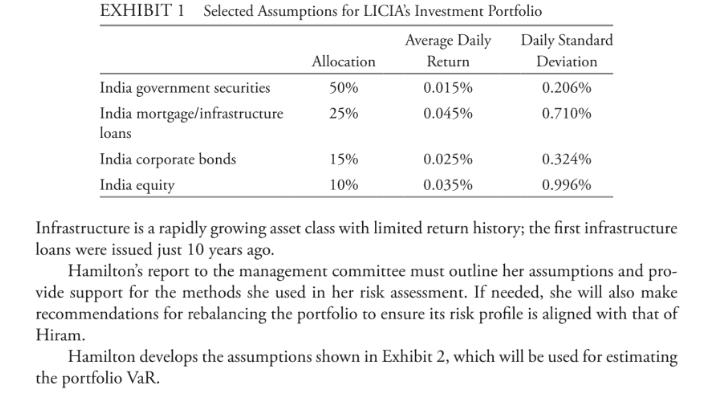

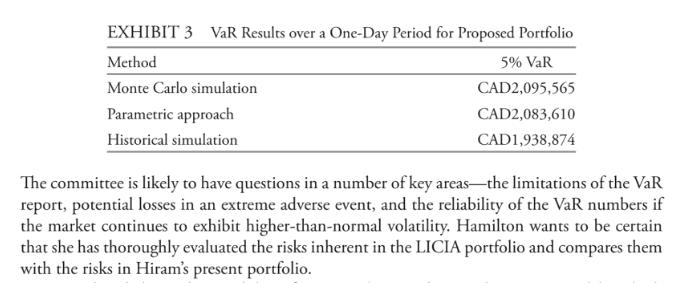

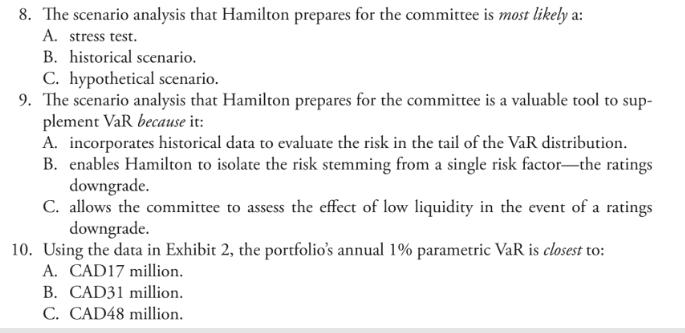

Hiram Life (Hiram), a large multinational insurer located in Canada, has received permission to increase its ownership in an India-based life insurance company, LICIA, from 26% to 49%. Before completing this transaction, Hiram wants to complete a risk assessment of LICIA's investment portfolio. Judith Hamilton, Hiram's chief financial officer, has been asked to brief the management committee on investment risk in its India-based insurance operations. LICIA's portfolio, which has a market value of CAD260 million, is currently structured as shown in Exhibit 1. Despite its more than 1,000 individual holdings, the portfolio is invested predominantly in India. The Indian government bond market is highly liquid, but the country's mortgage and infrastructure loan markets, as well as the corporate bond market, are relatively illiquid. Individual mortgage and corporate bond positions are large relative to the normal trading volumes in these securities. Given the elevated current and fiscal account deficits, Indian investments are also subject to above-average economic risk. Hamilton begins with a summary of the India-based portfolio. Exhibit 1 presents the current portfolio composition and the risk and return assumptions used to estimate value at risk (VaR). EXHIBIT 1 Selected Assumptions for LICIA's Investment Portfolio Average Daily Return India government securities India mortgage/infrastructure loans Hiram. India corporate bonds India equity Allocation 50% 25% 15% 10% 0.015% 0.045% 0.025% 0.035% Daily Standard Deviation 0.206% 0.710% 0.324% 0.996% Infrastructure is a rapidly growing asset class with limited return history; the first infrastructure loans were issued just 10 years ago. Hamilton's report to the management committee must outline her assumptions and pro- vide support for the methods she used in her risk assessment. If needed, she will also make recommendations for rebalancing the portfolio to ensure its risk profile is aligned with that of Hamilton develops the assumptions shown in Exhibit 2, which will be used for estimating the portfolio VaR. EXHIBIT 2 VaR Input Assumptions for Proposed CAD260 Million Portfolio Average Return Standard Deviation Method Monte Carlo simulation Parametric approach Historical simulation Assumption 0.026% 0.026% 0.023% Assumption 0.501% 0.501% 0.490% Hamilton elects to apply a one-day, 5% VaR limit of CAD2 million in her risk assessment of LICIA's portfolio. This limit is consistent with the risk tolerance the committee has specified for the Hiram portfolio. The markets' volatility during the last 12 months has been significantly higher than the historical norm, with increased frequency of large daily losses, and Hamilton expects the next 12 months to be equally volatile. She estimates the one-day 5% portfolio VaR for LICIA's portfolio using three different approaches: EXHIBIT 3 VaR Results over a One-Day Period for Proposed Portfolio 5% VaR Method Monte Carlo simulation Parametric approach Historical simulation CAD2,095,565 CAD2,083,610 CAD1,938,874 The committee is likely to have questions in a number of key areas the limitations of the VaR report, potential losses in an extreme adverse event, and the reliability of the VaR numbers if the market continues to exhibit higher-than-normal volatility. Hamilton wants to be certain that she has thoroughly evaluated the risks inherent in the LICIA portfolio and compares them with the risks in Hiram's present portfolio. Hamilton believes the possibility of a ratings downgrade on Indian sovereign debt is high and not yet fully reflected in securities prices. If the rating is lowered, many of the portfolio's holdings will no longer meet Hiram's minimum ratings requirement. A downgrade's effect is unlikely to be limited to the government bond portfolio. All asset classes can be expected to be affected to some degree. Hamilton plans to include a scenario analysis that reflects this possibility to ensure that management has the broadest possible view of the risk exposures in the India portfolio. 6. Given Hamilton's expectations, which of the following models is most appropriate to use in estimating portfolio Var? A. Parametric method B. Historical simulation method C. Monte Carlo simulation method 7. Which risk measure is Hamilton most likely to present when addressing the committee's concerns regarding potential losses in extreme stress events? A. Relative VaR B. Incremental VaR C. Conditional VaR 8. The scenario analysis that Hamilton prepares for the committee is most likely a: A. stress test. B. historical scenario. C. hypothetical scenario. 9. The scenario analysis that Hamilton prepares for the committee is a valuable tool to sup- plement VaR because it: A. incorporates historical data to evaluate the risk in the tail of the VaR distribution. B. enables Hamilton to isolate the risk stemming from a single risk factor-the ratings downgrade. C. allows the committee to assess the effect of low liquidity in the event of a ratings downgrade. 10. Using the data in Exhibit 2, the portfolio's annual 1% parametric VaR is closest to: A. CAD17 million. B. CAD31 million. C. CAD48 million. Hiram Life (Hiram), a large multinational insurer located in Canada, has received permission to increase its ownership in an India-based life insurance company, LICIA, from 26% to 49%. Before completing this transaction, Hiram wants to complete a risk assessment of LICIA's investment portfolio. Judith Hamilton, Hiram's chief financial officer, has been asked to brief the management committee on investment risk in its India-based insurance operations. LICIA's portfolio, which has a market value of CAD260 million, is currently structured as shown in Exhibit 1. Despite its more than 1,000 individual holdings, the portfolio is invested predominantly in India. The Indian government bond market is highly liquid, but the country's mortgage and infrastructure loan markets, as well as the corporate bond market, are relatively illiquid. Individual mortgage and corporate bond positions are large relative to the normal trading volumes in these securities. Given the elevated current and fiscal account deficits, Indian investments are also subject to above-average economic risk. Hamilton begins with a summary of the India-based portfolio. Exhibit 1 presents the current portfolio composition and the risk and return assumptions used to estimate value at risk (VaR). EXHIBIT 1 Selected Assumptions for LICIA's Investment Portfolio Average Daily Return India government securities India mortgage/infrastructure loans Hiram. India corporate bonds India equity Allocation 50% 25% 15% 10% 0.015% 0.045% 0.025% 0.035% Daily Standard Deviation 0.206% 0.710% 0.324% 0.996% Infrastructure is a rapidly growing asset class with limited return history; the first infrastructure loans were issued just 10 years ago. Hamilton's report to the management committee must outline her assumptions and pro- vide support for the methods she used in her risk assessment. If needed, she will also make recommendations for rebalancing the portfolio to ensure its risk profile is aligned with that of Hamilton develops the assumptions shown in Exhibit 2, which will be used for estimating the portfolio VaR. EXHIBIT 2 VaR Input Assumptions for Proposed CAD260 Million Portfolio Average Return Standard Deviation Method Monte Carlo simulation Parametric approach Historical simulation Assumption 0.026% 0.026% 0.023% Assumption 0.501% 0.501% 0.490% Hamilton elects to apply a one-day, 5% VaR limit of CAD2 million in her risk assessment of LICIA's portfolio. This limit is consistent with the risk tolerance the committee has specified for the Hiram portfolio. The markets' volatility during the last 12 months has been significantly higher than the historical norm, with increased frequency of large daily losses, and Hamilton expects the next 12 months to be equally volatile. She estimates the one-day 5% portfolio VaR for LICIA's portfolio using three different approaches: EXHIBIT 3 VaR Results over a One-Day Period for Proposed Portfolio 5% VaR Method Monte Carlo simulation Parametric approach Historical simulation CAD2,095,565 CAD2,083,610 CAD1,938,874 The committee is likely to have questions in a number of key areas the limitations of the VaR report, potential losses in an extreme adverse event, and the reliability of the VaR numbers if the market continues to exhibit higher-than-normal volatility. Hamilton wants to be certain that she has thoroughly evaluated the risks inherent in the LICIA portfolio and compares them with the risks in Hiram's present portfolio. Hamilton believes the possibility of a ratings downgrade on Indian sovereign debt is high and not yet fully reflected in securities prices. If the rating is lowered, many of the portfolio's holdings will no longer meet Hiram's minimum ratings requirement. A downgrade's effect is unlikely to be limited to the government bond portfolio. All asset classes can be expected to be affected to some degree. Hamilton plans to include a scenario analysis that reflects this possibility to ensure that management has the broadest possible view of the risk exposures in the India portfolio. 6. Given Hamilton's expectations, which of the following models is most appropriate to use in estimating portfolio Var? A. Parametric method B. Historical simulation method C. Monte Carlo simulation method 7. Which risk measure is Hamilton most likely to present when addressing the committee's concerns regarding potential losses in extreme stress events? A. Relative VaR B. Incremental VaR C. Conditional VaR 8. The scenario analysis that Hamilton prepares for the committee is most likely a: A. stress test. B. historical scenario. C. hypothetical scenario. 9. The scenario analysis that Hamilton prepares for the committee is a valuable tool to sup- plement VaR because it: A. incorporates historical data to evaluate the risk in the tail of the VaR distribution. B. enables Hamilton to isolate the risk stemming from a single risk factor-the ratings downgrade. C. allows the committee to assess the effect of low liquidity in the event of a ratings downgrade. 10. Using the data in Exhibit 2, the portfolio's annual 1% parametric VaR is closest to: A. CAD17 million. B. CAD31 million. C. CAD48 million.

Expert Answer:

Answer rating: 100% (QA)

Hamilton s report to the management committee will provid... View the full answer

Related Book For

Marketing The Core

ISBN: 978-0078028922

5th edition

Authors: Roger A. Kerin, Steven W. Hartley, William Rudelius

Posted Date:

Students also viewed these banking questions

-

Imagine Victoria Industrial Equipment Corporation (VIEC) located in Canada has an asset costs $675,000 at the beginning of the year. The Capital Cost Allowance rate for this asset is 25%. The asset's...

-

A bond speculator currently has positions in two separate corporate bond portfolios: a long holding in Portfolio 1 and a short holding in Portfolio 2. All the bonds have the same credit quality....

-

Current market yields on U.S. government securities are distributed by maturity as follows: Draw a yield curve for these securities. What shape does the curve have? What significance might this yield...

-

How does unemployment behave over the business cycle?

-

A user queries the Part table in the Premiere Products database over the company intranet. Assume the Part table contains 5,000 rows, each row is 1,000 bits long, the access delay is 2.5 seconds, the...

-

Suppose the following bond quotes for IOU Corporation appear in the financial page of today's newspaper. Assume the bond has a face value of $1,000 and the current date is April 15, 2009. What is the...

-

A long wire used as a heating element carries a current of \(0.80 \mathrm{~A}\). It dissipates \(6.0 \mathrm{~W}\) for every meter of length. What is the electric field strength inside this wire?

-

Custom Metal Works produces castings and other metal parts to customer specifications. The company uses a job-order costing system and applies overhead costs to jobs on the basis of machine-hours. At...

-

A bond is available for purchase. If current interest rates are 4.00%, is this bond over or under priced? Issued 2014 Par Value (Face Value) 1,000 Coupon rate 4.25% Payment 42.5 Term (years) 30 Years...

-

On January 1, 2024, Marigold Company purchased 8,568 shares of Swifty Company's common stock for $123,000. Immediately after the stock acquisition, the statements of financial position of Marigold...

-

DP, a U.S. corporation, has two wholly owned subsidiaries, DS, a U.S. corporation, and FS, a foreign subsidiary incorporated in country X. DS manufactures hammers at a cost of $10 per unit and sells...

-

This four step assessment process is based on the premise that by understanding its risks, a community can make smart decisions about how to manage risk, including developing needed capabilities....

-

is the allocation of the cost of a long-lived, tangible asset over its useful life creating an expense on the income statement that is matched against the revenue generated by using the asset.

-

The opportunity to establish a risk value on a routine operation may or may not be of use to the operations department. As the safety manager for an offshore drilling rig, you believe that a standard...

-

Reflect on the technical skills developed through all Accounting and Finance workshops.

-

The Adidas Communication Strategy Marketing Communication strategy of Adidas is based on on-line and offline advertising and promotion. Development of informative web site is the top priority for...

-

2) What is the output of the following Python statement? print (8/3, 4* 7,9 + 13, 2 ** 5, 6 * (3 + 2))

-

A circular concrete shaft liner with Youngs modulus of 3.4 million psi, Poissons ratio of 0.25, unconfined compressive strength 3,500 psi and tensile strength 350 psi is loaded to the verge of...

-

Breadth and depth are two important components in distinguishing among types of retailers. Discuss the breadth and depth implications of the following retailers discussed in this chapter: (a)...

-

What would be your response to the statement, Profit maximization is the only legitimate pricing objective for the firm?

-

Idle production capacity may be related to inventory or capacity management. How would the pricing component of the marketing mix reduce idle production capacity for (a) A car wash, (b) A stage...

-

Perhaps the most famous case illustrating the enormous cost of winning back lost customers is that of the Tylenol Murders. Seven people in the Chicago area died suddenly after taking Tylenol...

-

Give a brief rationale for empowerment.

-

Describe the concept of MBWA.

Study smarter with the SolutionInn App