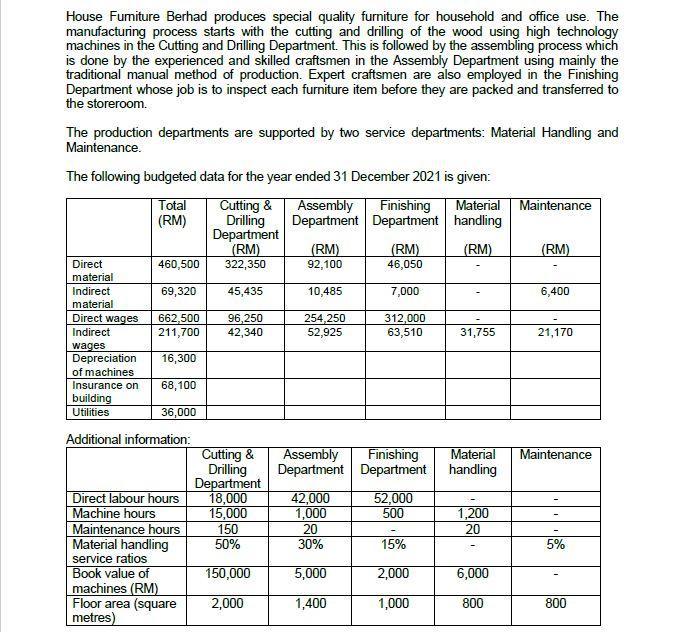

House Fumiture Berhad produces special quality furniture for household and office use. The manufacturing process starts...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

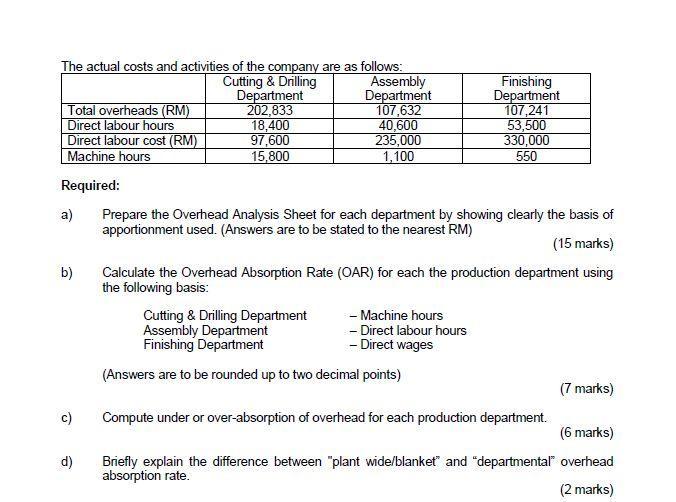

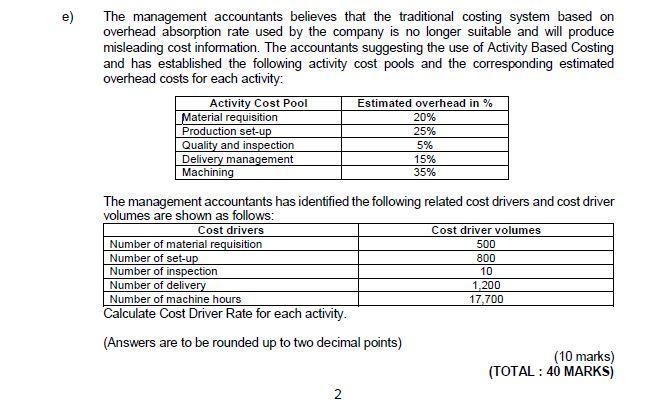

House Fumiture Berhad produces special quality furniture for household and office use. The manufacturing process starts with the cutting and drilling of the wood using high technology machines in the Cutting and Drilling Department. This is followed by the assembling process which is done by the experienced and skilled craftsmen in the Assembly Department using mainly the traditional manual method of production. Expert craftsmen are also employed in the Finishing Department whose job is to inspect each furniture item before they are packed and transferred to the storeroom. The production departments are supported by two service departments: Material Handling and Maintenance. The following budgeted data for the year ended 31 December 2021 is given: Total (RM) Cutting & Drilling Department (RM) Assembly Finishing Department Department handling Material Maintenance (RM) (RM) 92,100 (RM) 46,050 (RM) Direct 460,500 322,350 material Indirect 69,320 45,435 10,485 7,000 6,400 material Direct wages 662,500 211,700 96,250 42,340 254,250 52,925 312,000 63,510 Indirect 31,755 21,170 wages Depreciation of machines 16,300 Insurance on 68,100 building Utilities 36,000 Additional information: Cutting & Drilling Department 18,000 15,000 Finishing Department Department handling Assembly Material Maintenance Direct labour hours Machine hours Maintenance hours Material handling service ratios Book value of machines (RM) Floor area (square metres) 42,000 1,000 52,000 500 1,200 20 150 50% 20 30% 15% 5% 150,000 5,000 2,000 6,000 2,000 1,400 1,000 800 800 The actual costs and activities of the company are as follows: Cutting & Drilling Department 202,833 18,400 97,600 15,800 Total overheads (RM) Direct labour hours Direct labour cost (RM) Machine hours Assembly Department 107,632 40,600 235,000 1,100 Finishing Department 107,241 53,500 330,000 550 Required: a) Prepare the Overhead Analysis Sheet for each department by showing clearly the basis of apportionment used. (Answers are to be stated to the nearest RM) (15 marks) b) Calculate the Overhead Absorption Rate (OAR) for each the production department using the following basis: Cutting & Drilling Department Assembly Department Finishing Department - Machine hours - Direct labour hours - Direct wages (Answers are to be rounded up to two decimal points) (7 marks) c) Compute under or over-absorption of overhead for each production department. (6 marks) d) Briefly explain the difference between "plant wide/blanket" and "departmental" overhead absorption rate. (2 marks) e) The management accountants believes that the traditional costing system based on overhead absorption rate used by the company is no longer suitable and will produce misleading cost information. The accountants suggesting the use of Activity Based Costing and has established the following activity cost pools and the corresponding estimated overhead costs for each activity: Activity Cost Pool Material requisition Production set-up Quality and inspection Delivery management Machining Estimated overhead in % 20% 25% 5% 15% 35% The management accountants has identified the following related cost drivers and cost driver volumes are shown as follows: Cost drivers Cost driver volumes Number of material requisition Number of set-up Number of inspection Number of delivery Number of machine hours Calculate Cost Driver Rate for each activity. 500 800 10 1,200 17,700 (Answers are to be rounded up to two decimal points) (10 marks) (TOTAL : 40 MARKS) 2 House Fumiture Berhad produces special quality furniture for household and office use. The manufacturing process starts with the cutting and drilling of the wood using high technology machines in the Cutting and Drilling Department. This is followed by the assembling process which is done by the experienced and skilled craftsmen in the Assembly Department using mainly the traditional manual method of production. Expert craftsmen are also employed in the Finishing Department whose job is to inspect each furniture item before they are packed and transferred to the storeroom. The production departments are supported by two service departments: Material Handling and Maintenance. The following budgeted data for the year ended 31 December 2021 is given: Total (RM) Cutting & Drilling Department (RM) Assembly Finishing Department Department handling Material Maintenance (RM) (RM) 92,100 (RM) 46,050 (RM) Direct 460,500 322,350 material Indirect 69,320 45,435 10,485 7,000 6,400 material Direct wages 662,500 211,700 96,250 42,340 254,250 52,925 312,000 63,510 Indirect 31,755 21,170 wages Depreciation of machines 16,300 Insurance on 68,100 building Utilities 36,000 Additional information: Cutting & Drilling Department 18,000 15,000 Finishing Department Department handling Assembly Material Maintenance Direct labour hours Machine hours Maintenance hours Material handling service ratios Book value of machines (RM) Floor area (square metres) 42,000 1,000 52,000 500 1,200 20 150 50% 20 30% 15% 5% 150,000 5,000 2,000 6,000 2,000 1,400 1,000 800 800 The actual costs and activities of the company are as follows: Cutting & Drilling Department 202,833 18,400 97,600 15,800 Total overheads (RM) Direct labour hours Direct labour cost (RM) Machine hours Assembly Department 107,632 40,600 235,000 1,100 Finishing Department 107,241 53,500 330,000 550 Required: a) Prepare the Overhead Analysis Sheet for each department by showing clearly the basis of apportionment used. (Answers are to be stated to the nearest RM) (15 marks) b) Calculate the Overhead Absorption Rate (OAR) for each the production department using the following basis: Cutting & Drilling Department Assembly Department Finishing Department - Machine hours - Direct labour hours - Direct wages (Answers are to be rounded up to two decimal points) (7 marks) c) Compute under or over-absorption of overhead for each production department. (6 marks) d) Briefly explain the difference between "plant wide/blanket" and "departmental" overhead absorption rate. (2 marks) e) The management accountants believes that the traditional costing system based on overhead absorption rate used by the company is no longer suitable and will produce misleading cost information. The accountants suggesting the use of Activity Based Costing and has established the following activity cost pools and the corresponding estimated overhead costs for each activity: Activity Cost Pool Material requisition Production set-up Quality and inspection Delivery management Machining Estimated overhead in % 20% 25% 5% 15% 35% The management accountants has identified the following related cost drivers and cost driver volumes are shown as follows: Cost drivers Cost driver volumes Number of material requisition Number of set-up Number of inspection Number of delivery Number of machine hours Calculate Cost Driver Rate for each activity. 500 800 10 1,200 17,700 (Answers are to be rounded up to two decimal points) (10 marks) (TOTAL : 40 MARKS) 2 House Fumiture Berhad produces special quality furniture for household and office use. The manufacturing process starts with the cutting and drilling of the wood using high technology machines in the Cutting and Drilling Department. This is followed by the assembling process which is done by the experienced and skilled craftsmen in the Assembly Department using mainly the traditional manual method of production. Expert craftsmen are also employed in the Finishing Department whose job is to inspect each furniture item before they are packed and transferred to the storeroom. The production departments are supported by two service departments: Material Handling and Maintenance. The following budgeted data for the year ended 31 December 2021 is given: Total (RM) Cutting & Drilling Department (RM) Assembly Finishing Department Department handling Material Maintenance (RM) (RM) 92,100 (RM) 46,050 (RM) Direct 460,500 322,350 material Indirect 69,320 45,435 10,485 7,000 6,400 material Direct wages 662,500 211,700 96,250 42,340 254,250 52,925 312,000 63,510 Indirect 31,755 21,170 wages Depreciation of machines 16,300 Insurance on 68,100 building Utilities 36,000 Additional information: Cutting & Drilling Department 18,000 15,000 Finishing Department Department handling Assembly Material Maintenance Direct labour hours Machine hours Maintenance hours Material handling service ratios Book value of machines (RM) Floor area (square metres) 42,000 1,000 52,000 500 1,200 20 150 50% 20 30% 15% 5% 150,000 5,000 2,000 6,000 2,000 1,400 1,000 800 800 The actual costs and activities of the company are as follows: Cutting & Drilling Department 202,833 18,400 97,600 15,800 Total overheads (RM) Direct labour hours Direct labour cost (RM) Machine hours Assembly Department 107,632 40,600 235,000 1,100 Finishing Department 107,241 53,500 330,000 550 Required: a) Prepare the Overhead Analysis Sheet for each department by showing clearly the basis of apportionment used. (Answers are to be stated to the nearest RM) (15 marks) b) Calculate the Overhead Absorption Rate (OAR) for each the production department using the following basis: Cutting & Drilling Department Assembly Department Finishing Department - Machine hours - Direct labour hours - Direct wages (Answers are to be rounded up to two decimal points) (7 marks) c) Compute under or over-absorption of overhead for each production department. (6 marks) d) Briefly explain the difference between "plant wide/blanket" and "departmental" overhead absorption rate. (2 marks) e) The management accountants believes that the traditional costing system based on overhead absorption rate used by the company is no longer suitable and will produce misleading cost information. The accountants suggesting the use of Activity Based Costing and has established the following activity cost pools and the corresponding estimated overhead costs for each activity: Activity Cost Pool Material requisition Production set-up Quality and inspection Delivery management Machining Estimated overhead in % 20% 25% 5% 15% 35% The management accountants has identified the following related cost drivers and cost driver volumes are shown as follows: Cost drivers Cost driver volumes Number of material requisition Number of set-up Number of inspection Number of delivery Number of machine hours Calculate Cost Driver Rate for each activity. 500 800 10 1,200 17,700 (Answers are to be rounded up to two decimal points) (10 marks) (TOTAL : 40 MARKS) 2 House Fumiture Berhad produces special quality furniture for household and office use. The manufacturing process starts with the cutting and drilling of the wood using high technology machines in the Cutting and Drilling Department. This is followed by the assembling process which is done by the experienced and skilled craftsmen in the Assembly Department using mainly the traditional manual method of production. Expert craftsmen are also employed in the Finishing Department whose job is to inspect each furniture item before they are packed and transferred to the storeroom. The production departments are supported by two service departments: Material Handling and Maintenance. The following budgeted data for the year ended 31 December 2021 is given: Total (RM) Cutting & Drilling Department (RM) Assembly Finishing Department Department handling Material Maintenance (RM) (RM) 92,100 (RM) 46,050 (RM) Direct 460,500 322,350 material Indirect 69,320 45,435 10,485 7,000 6,400 material Direct wages 662,500 211,700 96,250 42,340 254,250 52,925 312,000 63,510 Indirect 31,755 21,170 wages Depreciation of machines 16,300 Insurance on 68,100 building Utilities 36,000 Additional information: Cutting & Drilling Department 18,000 15,000 Finishing Department Department handling Assembly Material Maintenance Direct labour hours Machine hours Maintenance hours Material handling service ratios Book value of machines (RM) Floor area (square metres) 42,000 1,000 52,000 500 1,200 20 150 50% 20 30% 15% 5% 150,000 5,000 2,000 6,000 2,000 1,400 1,000 800 800 The actual costs and activities of the company are as follows: Cutting & Drilling Department 202,833 18,400 97,600 15,800 Total overheads (RM) Direct labour hours Direct labour cost (RM) Machine hours Assembly Department 107,632 40,600 235,000 1,100 Finishing Department 107,241 53,500 330,000 550 Required: a) Prepare the Overhead Analysis Sheet for each department by showing clearly the basis of apportionment used. (Answers are to be stated to the nearest RM) (15 marks) b) Calculate the Overhead Absorption Rate (OAR) for each the production department using the following basis: Cutting & Drilling Department Assembly Department Finishing Department - Machine hours - Direct labour hours - Direct wages (Answers are to be rounded up to two decimal points) (7 marks) c) Compute under or over-absorption of overhead for each production department. (6 marks) d) Briefly explain the difference between "plant wide/blanket" and "departmental" overhead absorption rate. (2 marks) e) The management accountants believes that the traditional costing system based on overhead absorption rate used by the company is no longer suitable and will produce misleading cost information. The accountants suggesting the use of Activity Based Costing and has established the following activity cost pools and the corresponding estimated overhead costs for each activity: Activity Cost Pool Material requisition Production set-up Quality and inspection Delivery management Machining Estimated overhead in % 20% 25% 5% 15% 35% The management accountants has identified the following related cost drivers and cost driver volumes are shown as follows: Cost drivers Cost driver volumes Number of material requisition Number of set-up Number of inspection Number of delivery Number of machine hours Calculate Cost Driver Rate for each activity. 500 800 10 1,200 17,700 (Answers are to be rounded up to two decimal points) (10 marks) (TOTAL : 40 MARKS) 2 House Fumiture Berhad produces special quality furniture for household and office use. The manufacturing process starts with the cutting and drilling of the wood using high technology machines in the Cutting and Drilling Department. This is followed by the assembling process which is done by the experienced and skilled craftsmen in the Assembly Department using mainly the traditional manual method of production. Expert craftsmen are also employed in the Finishing Department whose job is to inspect each furniture item before they are packed and transferred to the storeroom. The production departments are supported by two service departments: Material Handling and Maintenance. The following budgeted data for the year ended 31 December 2021 is given: Total (RM) Cutting & Drilling Department (RM) Assembly Finishing Department Department handling Material Maintenance (RM) (RM) 92,100 (RM) 46,050 (RM) Direct 460,500 322,350 material Indirect 69,320 45,435 10,485 7,000 6,400 material Direct wages 662,500 211,700 96,250 42,340 254,250 52,925 312,000 63,510 Indirect 31,755 21,170 wages Depreciation of machines 16,300 Insurance on 68,100 building Utilities 36,000 Additional information: Cutting & Drilling Department 18,000 15,000 Finishing Department Department handling Assembly Material Maintenance Direct labour hours Machine hours Maintenance hours Material handling service ratios Book value of machines (RM) Floor area (square metres) 42,000 1,000 52,000 500 1,200 20 150 50% 20 30% 15% 5% 150,000 5,000 2,000 6,000 2,000 1,400 1,000 800 800 The actual costs and activities of the company are as follows: Cutting & Drilling Department 202,833 18,400 97,600 15,800 Total overheads (RM) Direct labour hours Direct labour cost (RM) Machine hours Assembly Department 107,632 40,600 235,000 1,100 Finishing Department 107,241 53,500 330,000 550 Required: a) Prepare the Overhead Analysis Sheet for each department by showing clearly the basis of apportionment used. (Answers are to be stated to the nearest RM) (15 marks) b) Calculate the Overhead Absorption Rate (OAR) for each the production department using the following basis: Cutting & Drilling Department Assembly Department Finishing Department - Machine hours - Direct labour hours - Direct wages (Answers are to be rounded up to two decimal points) (7 marks) c) Compute under or over-absorption of overhead for each production department. (6 marks) d) Briefly explain the difference between "plant wide/blanket" and "departmental" overhead absorption rate. (2 marks) e) The management accountants believes that the traditional costing system based on overhead absorption rate used by the company is no longer suitable and will produce misleading cost information. The accountants suggesting the use of Activity Based Costing and has established the following activity cost pools and the corresponding estimated overhead costs for each activity: Activity Cost Pool Material requisition Production set-up Quality and inspection Delivery management Machining Estimated overhead in % 20% 25% 5% 15% 35% The management accountants has identified the following related cost drivers and cost driver volumes are shown as follows: Cost drivers Cost driver volumes Number of material requisition Number of set-up Number of inspection Number of delivery Number of machine hours Calculate Cost Driver Rate for each activity. 500 800 10 1,200 17,700 (Answers are to be rounded up to two decimal points) (10 marks) (TOTAL : 40 MARKS) 2 House Fumiture Berhad produces special quality furniture for household and office use. The manufacturing process starts with the cutting and drilling of the wood using high technology machines in the Cutting and Drilling Department. This is followed by the assembling process which is done by the experienced and skilled craftsmen in the Assembly Department using mainly the traditional manual method of production. Expert craftsmen are also employed in the Finishing Department whose job is to inspect each furniture item before they are packed and transferred to the storeroom. The production departments are supported by two service departments: Material Handling and Maintenance. The following budgeted data for the year ended 31 December 2021 is given: Total (RM) Cutting & Drilling Department (RM) Assembly Finishing Department Department handling Material Maintenance (RM) (RM) 92,100 (RM) 46,050 (RM) Direct 460,500 322,350 material Indirect 69,320 45,435 10,485 7,000 6,400 material Direct wages 662,500 211,700 96,250 42,340 254,250 52,925 312,000 63,510 Indirect 31,755 21,170 wages Depreciation of machines 16,300 Insurance on 68,100 building Utilities 36,000 Additional information: Cutting & Drilling Department 18,000 15,000 Finishing Department Department handling Assembly Material Maintenance Direct labour hours Machine hours Maintenance hours Material handling service ratios Book value of machines (RM) Floor area (square metres) 42,000 1,000 52,000 500 1,200 20 150 50% 20 30% 15% 5% 150,000 5,000 2,000 6,000 2,000 1,400 1,000 800 800 The actual costs and activities of the company are as follows: Cutting & Drilling Department 202,833 18,400 97,600 15,800 Total overheads (RM) Direct labour hours Direct labour cost (RM) Machine hours Assembly Department 107,632 40,600 235,000 1,100 Finishing Department 107,241 53,500 330,000 550 Required: a) Prepare the Overhead Analysis Sheet for each department by showing clearly the basis of apportionment used. (Answers are to be stated to the nearest RM) (15 marks) b) Calculate the Overhead Absorption Rate (OAR) for each the production department using the following basis: Cutting & Drilling Department Assembly Department Finishing Department - Machine hours - Direct labour hours - Direct wages (Answers are to be rounded up to two decimal points) (7 marks) c) Compute under or over-absorption of overhead for each production department. (6 marks) d) Briefly explain the difference between "plant wide/blanket" and "departmental" overhead absorption rate. (2 marks) e) The management accountants believes that the traditional costing system based on overhead absorption rate used by the company is no longer suitable and will produce misleading cost information. The accountants suggesting the use of Activity Based Costing and has established the following activity cost pools and the corresponding estimated overhead costs for each activity: Activity Cost Pool Material requisition Production set-up Quality and inspection Delivery management Machining Estimated overhead in % 20% 25% 5% 15% 35% The management accountants has identified the following related cost drivers and cost driver volumes are shown as follows: Cost drivers Cost driver volumes Number of material requisition Number of set-up Number of inspection Number of delivery Number of machine hours Calculate Cost Driver Rate for each activity. 500 800 10 1,200 17,700 (Answers are to be rounded up to two decimal points) (10 marks) (TOTAL : 40 MARKS) 2 House Fumiture Berhad produces special quality furniture for household and office use. The manufacturing process starts with the cutting and drilling of the wood using high technology machines in the Cutting and Drilling Department. This is followed by the assembling process which is done by the experienced and skilled craftsmen in the Assembly Department using mainly the traditional manual method of production. Expert craftsmen are also employed in the Finishing Department whose job is to inspect each furniture item before they are packed and transferred to the storeroom. The production departments are supported by two service departments: Material Handling and Maintenance. The following budgeted data for the year ended 31 December 2021 is given: Total (RM) Cutting & Drilling Department (RM) Assembly Finishing Department Department handling Material Maintenance (RM) (RM) 92,100 (RM) 46,050 (RM) Direct 460,500 322,350 material Indirect 69,320 45,435 10,485 7,000 6,400 material Direct wages 662,500 211,700 96,250 42,340 254,250 52,925 312,000 63,510 Indirect 31,755 21,170 wages Depreciation of machines 16,300 Insurance on 68,100 building Utilities 36,000 Additional information: Cutting & Drilling Department 18,000 15,000 Finishing Department Department handling Assembly Material Maintenance Direct labour hours Machine hours Maintenance hours Material handling service ratios Book value of machines (RM) Floor area (square metres) 42,000 1,000 52,000 500 1,200 20 150 50% 20 30% 15% 5% 150,000 5,000 2,000 6,000 2,000 1,400 1,000 800 800 The actual costs and activities of the company are as follows: Cutting & Drilling Department 202,833 18,400 97,600 15,800 Total overheads (RM) Direct labour hours Direct labour cost (RM) Machine hours Assembly Department 107,632 40,600 235,000 1,100 Finishing Department 107,241 53,500 330,000 550 Required: a) Prepare the Overhead Analysis Sheet for each department by showing clearly the basis of apportionment used. (Answers are to be stated to the nearest RM) (15 marks) b) Calculate the Overhead Absorption Rate (OAR) for each the production department using the following basis: Cutting & Drilling Department Assembly Department Finishing Department - Machine hours - Direct labour hours - Direct wages (Answers are to be rounded up to two decimal points) (7 marks) c) Compute under or over-absorption of overhead for each production department. (6 marks) d) Briefly explain the difference between "plant wide/blanket" and "departmental" overhead absorption rate. (2 marks) e) The management accountants believes that the traditional costing system based on overhead absorption rate used by the company is no longer suitable and will produce misleading cost information. The accountants suggesting the use of Activity Based Costing and has established the following activity cost pools and the corresponding estimated overhead costs for each activity: Activity Cost Pool Material requisition Production set-up Quality and inspection Delivery management Machining Estimated overhead in % 20% 25% 5% 15% 35% The management accountants has identified the following related cost drivers and cost driver volumes are shown as follows: Cost drivers Cost driver volumes Number of material requisition Number of set-up Number of inspection Number of delivery Number of machine hours Calculate Cost Driver Rate for each activity. 500 800 10 1,200 17,700 (Answers are to be rounded up to two decimal points) (10 marks) (TOTAL : 40 MARKS) 2 House Fumiture Berhad produces special quality furniture for household and office use. The manufacturing process starts with the cutting and drilling of the wood using high technology machines in the Cutting and Drilling Department. This is followed by the assembling process which is done by the experienced and skilled craftsmen in the Assembly Department using mainly the traditional manual method of production. Expert craftsmen are also employed in the Finishing Department whose job is to inspect each furniture item before they are packed and transferred to the storeroom. The production departments are supported by two service departments: Material Handling and Maintenance. The following budgeted data for the year ended 31 December 2021 is given: Total (RM) Cutting & Drilling Department (RM) Assembly Finishing Department Department handling Material Maintenance (RM) (RM) 92,100 (RM) 46,050 (RM) Direct 460,500 322,350 material Indirect 69,320 45,435 10,485 7,000 6,400 material Direct wages 662,500 211,700 96,250 42,340 254,250 52,925 312,000 63,510 Indirect 31,755 21,170 wages Depreciation of machines 16,300 Insurance on 68,100 building Utilities 36,000 Additional information: Cutting & Drilling Department 18,000 15,000 Finishing Department Department handling Assembly Material Maintenance Direct labour hours Machine hours Maintenance hours Material handling service ratios Book value of machines (RM) Floor area (square metres) 42,000 1,000 52,000 500 1,200 20 150 50% 20 30% 15% 5% 150,000 5,000 2,000 6,000 2,000 1,400 1,000 800 800 The actual costs and activities of the company are as follows: Cutting & Drilling Department 202,833 18,400 97,600 15,800 Total overheads (RM) Direct labour hours Direct labour cost (RM) Machine hours Assembly Department 107,632 40,600 235,000 1,100 Finishing Department 107,241 53,500 330,000 550 Required: a) Prepare the Overhead Analysis Sheet for each department by showing clearly the basis of apportionment used. (Answers are to be stated to the nearest RM) (15 marks) b) Calculate the Overhead Absorption Rate (OAR) for each the production department using the following basis: Cutting & Drilling Department Assembly Department Finishing Department - Machine hours - Direct labour hours - Direct wages (Answers are to be rounded up to two decimal points) (7 marks) c) Compute under or over-absorption of overhead for each production department. (6 marks) d) Briefly explain the difference between "plant wide/blanket" and "departmental" overhead absorption rate. (2 marks) e) The management accountants believes that the traditional costing system based on overhead absorption rate used by the company is no longer suitable and will produce misleading cost information. The accountants suggesting the use of Activity Based Costing and has established the following activity cost pools and the corresponding estimated overhead costs for each activity: Activity Cost Pool Material requisition Production set-up Quality and inspection Delivery management Machining Estimated overhead in % 20% 25% 5% 15% 35% The management accountants has identified the following related cost drivers and cost driver volumes are shown as follows: Cost drivers Cost driver volumes Number of material requisition Number of set-up Number of inspection Number of delivery Number of machine hours Calculate Cost Driver Rate for each activity. 500 800 10 1,200 17,700 (Answers are to be rounded up to two decimal points) (10 marks) (TOTAL : 40 MARKS) 2

Expert Answer:

Answer rating: 100% (QA)

a Overhead analysis sheet for each department Total Basis Cutting Drilling Assembly Finishing Material handling Maintenance Direct material note Indir... View the full answer

Related Book For

Managerial Economics

ISBN: 978-0133020267

7th edition

Authors: Paul Keat, Philip K Young, Steve Erfle

Posted Date:

Students also viewed these accounting questions

-

The summarized statements for the year ended 31 December 2007 for Mat, Rug and P entities are as follows: Statements of comprehensive income for the year ended 31 December 2007 The following...

-

The financial statements for Lucky Ltd for the year ended 31 December 2014 were as follows. Additional information: Dividends paid during the year $60, 000 Retained earnings al 1 January 2014:...

-

The income statements for the year ended 31 December 2020 and the statements of financial position as at 31 December 2020 for Garden Plc, Leaf Ltd and Flower Ltd are given as follows: Statements of...

-

A production line will be used to manufacture an item. The line will be operated with using the same personnel during single shift operations. During the initial line certification, the first item...

-

The following frequency distribution shows the various levels of demand for a particular laptop computer sold by Costco during the last 50 business days. Determine the average number of laptops sold...

-

Water bury, Inc., manufactures and sells RF17, a specialty raft used for whitewater rafting. In 2013, it reported the following: 2013 Units produced and sold ......................... 20,000...

-

How does a data management system differ from a communication system?

-

Barbara Flynn sells papers at a newspaper stand for $.35. The papers cost her $.25, giving her a $.10 profit on each one she sells. From past experience Barbara knows that: (a) 20% of the time she...

-

Hazelnut Corporation manufactures lawn ornaments. It currently has two product lines, the basic and the luxury. Hazelnut has a total of $169,122 in overhead. The company has identified the following...

-

corporation is resisting the personal holding company tax, but the Tax Court sides with the IRS. Within 90 days after the adverse decision, one shareholder transfers his stock and $10,000 in cash to...

-

3 years ago on January 1, 2011, Daisy Company acquired 80 percent of Rose Company for $594,000 in cash. Roses net book value on that date was $610,000 and the fair value of the non-controlling...

-

In 2012, the state of California implemented a system of quantity regulation of greenhouse gases, which included tradable permits. This cap-and-trade program for greenhouse gas emissions distributes...

-

Find an example of how your workplace or school practices written communication with you personally (e.g., course syllabus, job orientation newsletter). Is the overall message easy to read and...

-

In 2015, the Congressional Budget Office (CBO) estimated the impact of repealing the Affordable Care Act (ACA) using both traditional and dynamic scoring practices. Under traditional scoring, they...

-

What type of documented letter would you need as part of a university admission or employment application?

-

The 2018 tax overhaul cut taxes for both individuals and corporations. But it includes a provision to sunset the individual tax cuts in the year 2025. Why does the bill include this provision? What...

-

Suppose the market risk premium is 4% and the risk-free interest rate is 4%. Using the data in the table, calculate the expected return of investing in a. Starbucks' stock. b. Hershey's stock. c....

-

During 2012, Cheng Book Store paid $483,000 for land and built a store in Georgetown. Prior to construction, the city of Georgetown charged Cheng $1,300 for a building permit, which Cheng paid. Cheng...

-

Define coefficient of variation.

-

The Grand Design Corporation uses the certainty equivalent approach in making capital budgeting decisions. You are given the following data for a particular project The risk-free discount rate is I...

-

The Distinctive Fashions Company increased its advertising budget for its leading brand of women's yoga apparel from $10,000 in 2011 to $15,000 in 2012. Its sales increased from 900 units to 1,050...

-

Find the probability of an IQ less than 85.

-

If 25 women are randomly selected, find the probability that the mean of their red blood cell counts is less than 4.444. Assume that red blood cell counts of women are normally distributed with a...

-

Mensa International calls itself the international high IQ society, and it has more than 100,000 members. Mensa states that candidates for membership of Mensa must achieve a score at or above the...

Study smarter with the SolutionInn App